People

- Liza Guzman

- Priya Punatar

Topics

- Consumer Protection

- Credit

- Customer Centricity

- Digital Financial Services

- Digital Transformation

- Financial Capability

- Financial Health

- Fintech

- Human Centered Design

- Microfinance

- MSME/SME Finance

- Partnerships

- Personal Financial Management

- Resilience

- Responsible Product Design and Delivery

- Small Business Owners

- Supply Chain Finance

- Underserved Groups

Foreword

Karen is a single mom who lives in Santiago, Chile, with her young daughter. She went to school to study business administration but had to drop out to care for her daughter. Today, she works at a retail shop where she makes just enough to get by. Karen worries all the time — about paying the bills each month, about providing for her daughter, and about her growing credit card debt. She knows she needs to make a change, but she doesn’t know where to start. She has tried to put together a plan to pay off her debt, but it is difficult to figure out the total amount she owes or identify the right person to call. Thinking about money makes her feel stressed, overwhelmed, and alone.

To achieve their goals and build financial health, people like Karen need products and services that can help them to better track their finances, manage shocks (like global pandemics) and pursue financial goals.

Unfortunately, most low-income individuals and small businesses currently lack access to formal financial services; nearly half of adults in Latin America do not have a formal bank account, and those with accounts use them infrequently. This suggests that most of the financial products available to users in Latin America may be expensive, inconvenient, inappropriate, or all three.

This is because developing relevant financial services for low-income households and small businesses — that can have a meaningful impact on their financial health — is not straightforward. Low-income customers often lack formal financial records, operate informally, and have little experience with formal financial services, making it difficult for providers to pinpoint their needs. Moreover, many of these customers distrust formal financial services and hold negative beliefs around account ownership and credit. To craft relevant financial products, providers must acquire a deep understanding of their customer’s financial behaviors, pain points, ambitions, attitudes, and capabilities.

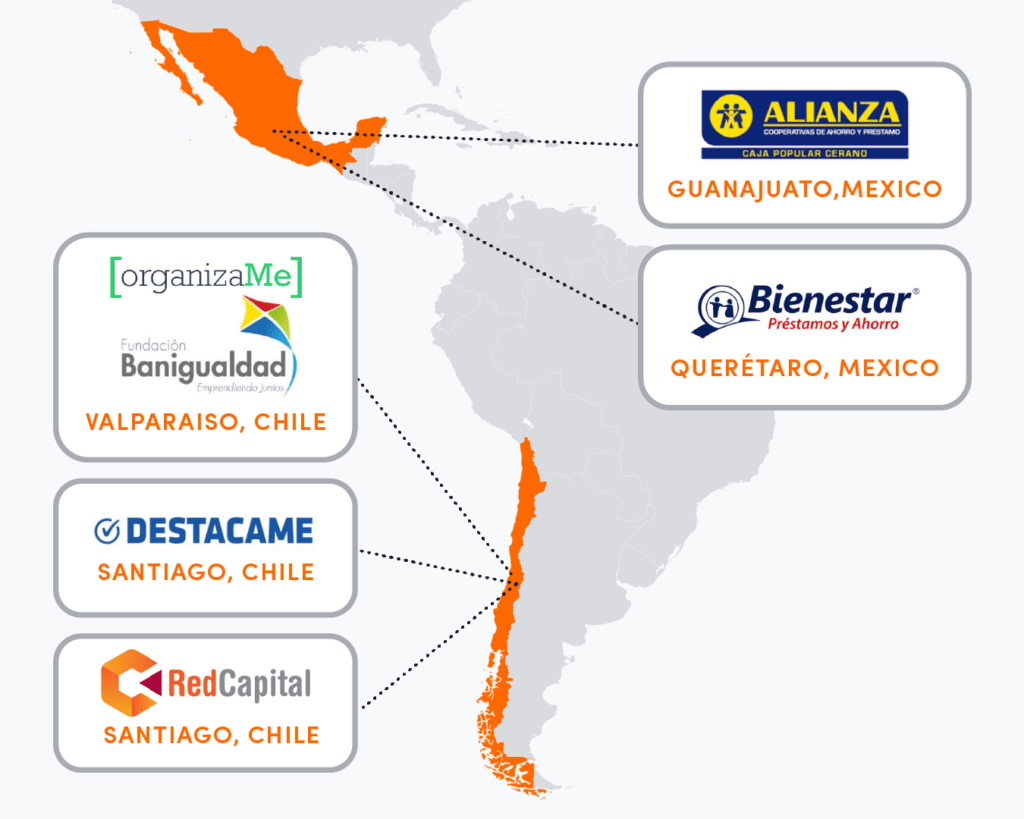

To help them develop financial services that can deliver financial health, Accion Global Advisory Solutions along with MetLife Foundation partnered with fintechs, cooperatives, and traditional financial service providers (FSPs) in Chile and Mexico to develop products to better serve their low-income customers. Accion worked with these FSP partners to design and launch viable digital products and services to reach underserved clients and improve their financial health, to help them maintain resilience against adversity and take advantage of opportunities.

This paper shares five case studies about Accion’s work with Chilean and Mexican partners over the past three and a half years. In Chile, we used human-centered design and behavioral economics to launch a business management application for microbusinesses with Organizame and Banigualdad, revamped a financial health portal with Destácame, and deployed a crowd-funding platform for microentrepreneurs with RedCapital. In Mexico, we developed a savings product for youth with Caja Popular Cerano and launched a supply chain finance product with Caja Bienestar. In this paper, we share our key challenges, learnings, and overall results from this project — uncovering best practices on how to design for and influence financial health along the way.

To date, most financial health efforts have focused on measurement and monitoring, but little guidance has been provided to financial service providers that are at the frontlines of engaging and serving customers on a daily basis. This paper is a first effort in that direction, giving providers actionable lessons for how to support positive financial health outcomes among their users. Moreover, the case studies within demonstrate the positive impact that a financial health-focused approach has on loyalty, customer lifetime value, and in creating new customer acquisition opportunities.

In the midst of enormous financial uncertainty sparked by COVID-19, our efforts to help underserved families and businesses improve their financial capabilities and develop healthy financial behaviors are critical. Our hope is that this paper will help financial service providers develop and optimize financial health-centric products that will lead to meaningful changes in the financial lives of their customers. This will require a more holistic approach to designing products for underserved individuals that includes consideration of their financial capabilities and historic behaviors. We believe that such an approach will result in better products with greater uptake and engagement.

Liza Guzman

Vice President and Program Manager, Customer Strategy

Executive summary

People around the world are continually working to improve their financial lives. They do so with whatever knowledge they have gathered and with the tools available to them, some informal and some formal. Much of this effort happens outside of financial services; people work hard to grow their businesses, send their children to school, and troubleshoot during tough moments. Ultimately, all people aspire for greater financial health and for better lives for themselves and their families.

Ultimately, all people aspire for greater financial health and for better lives for themselves and their families.

In 2018, Accion and MetLife Foundation launched a partnership to explore how financial service providers (FSPs) can craft financial products to support these efforts. More specifically, they sought to design products that benefit users’ financial health using customer-centric, behaviorally informed design. The project aimed to build better digital financial products and delivery methods grounded in customer needs to benefit underserved customers.

This paper features five in-depth case studies that detail Accion’s experience working with five financial service provider (FSP) partners in Chile and Mexico over the past three years.

The teams worked together to design and launch innovative financial products,

and to monitor their impact via financial health measurements. The case studies dive into the contextual problems we worked to solve, the product features that we designed, and share preliminary measures of product uptake and impact on users seen to date. At the end of each case study, we share key takeaways for FSPs and industry players that are seeking to build the financial health of low-income and underserved populations.

For each of these products, Accion Global Advisory Solutions helped FSPs develop the skills to truly listen to what their customers need, design best-in-class digital products utilizing behavioral science principles to nudge healthy financial behaviors and implement a financial health measurement methodology. We also worked closely with our partner institutions to ensure that product concepts were desirable, feasible, and viable; to manage organizational change; and to market the products effectively. In Mexico, we launched a supply chain finance product with Caja Bienestar and a savings product for youth with Caja Popular Cerano. In Chile, we revamped a financial health portal with Destácame, tailored a business management application for (micro, small, and medium enterprises) MSMEs with Organizame and Banigualdad, and deployed a crowd-funding platform for microentrepreneurs with RedCapital.

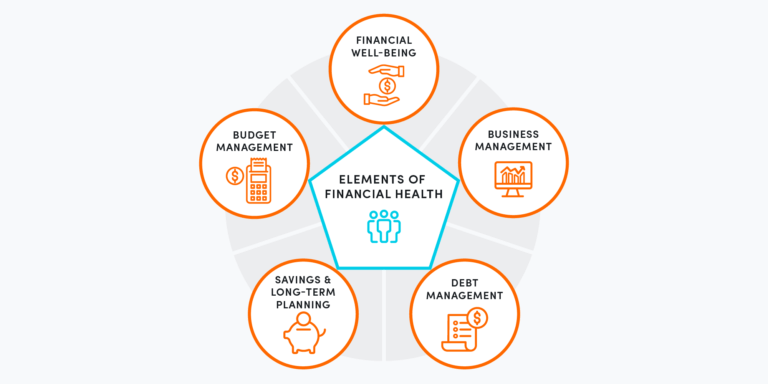

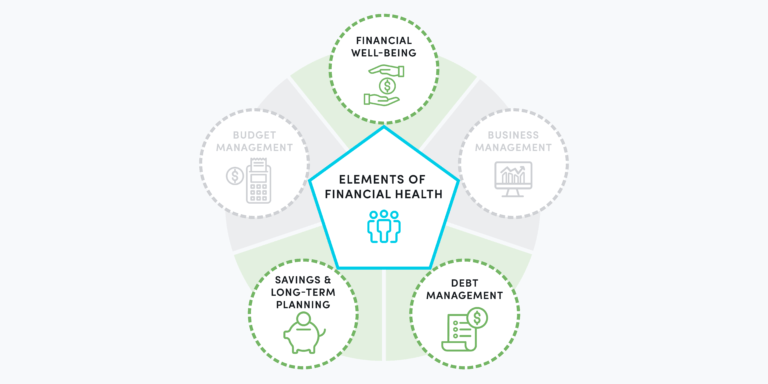

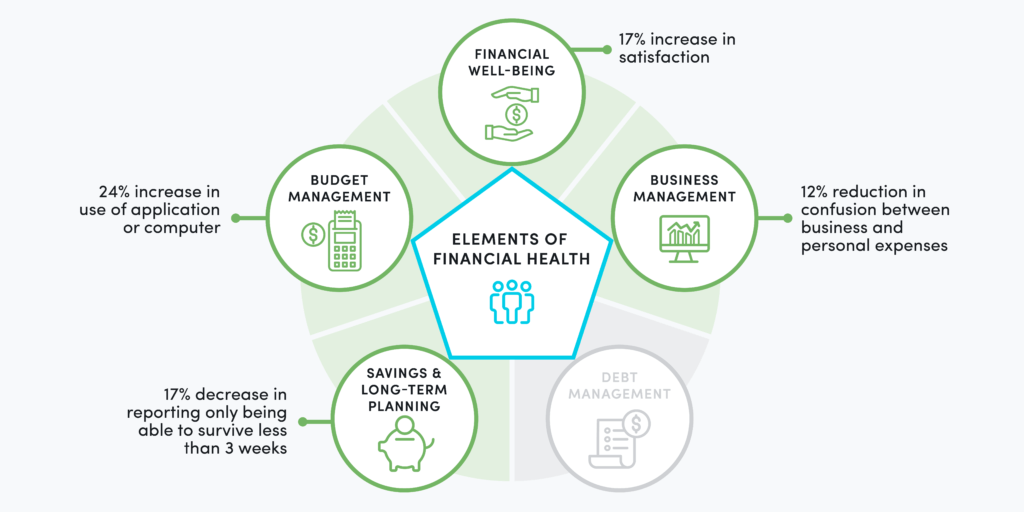

To assess and document the impact of these products on users’ financial health — the state in which an individual can meet current needs, absorb financial shocks (like global pandemics), and pursue financial goals — we tracked outcomes in five areas that map to our conceptual framework for financial health for individuals and MSMEs: overall feelings of financial well-being, budget management, debt management, savings and long-term planning, and business management.

While these products are still early days in terms of customer uptake and traction, preliminary results reveal significant and positive improvements across these dimensions of financial health. We found that:

- Nearly all products resulted in less financial stress and greater satisfaction with their current financial situation. Among users that own their own business, many demonstrated an ability to bounce back to levels prior to the COVID-19 pandemic level of sales (or higher!) when compared with control groups that did not use the financial products developed through this project.

- Easy-to-use budget management tools led to more users tracking their income and expenses on a more regular basis, therefore making users feel more in control of their finances.

- Across all products, individuals and businesses felt that they had a manageable level of debt, were better able to pay their credit on time, and were more comfortable taking out credit with a formal financial provider.

- Individuals using each of the products were able to save more and contribute to emergency funds.

- Business owners that took out working capital credit or used the business management tools noted that the additional liquidity enabled their business to take advantage of more opportunities.

Through our work with our partners and their clients across this project, we uncovered five cross-cutting takeaways for building relevant, impactful, and financial health-centric products:

Five cross-cutting takeaways for building relevant, impactful, and financial health-centric products

To encourage sustained behavior change, institutions need to embed healthy financial habits within existing practice and actions and minimize the need for additional effort. Products like automated savings accounts and direct debit payments have demonstrated the success of seamless approaches, which reduce decision-making effort (and associated fatigue) and make saving and expense management feel effortless.

To meaningfully build financial well-being, institutions need to ingrain healthy financial habits into everyday life and encourage frequent interaction with the user. An occasional touchpoint is unlikely to lead to durable change.

Human touch is critical for delivering digital financial tools to customers unfamiliar with digital technology or that lack digital literacy. Most successful financial service providers rely on human touch at various stages in a customer journey to build trust, establish relationships, and engage their customers.

Well-designed financial-health-building tools and content are attractive to users, and FSPs increasingly recognize it as a customer acquisition tool. The ability to show impact on end-customers’ financial health, a key pain point globally in the aftermath of the COVID-19 pandemic, can bring new business opportunities and partnerships with other institutions that enable rapid user growth.

Customers that used and engaged with products with an explicit aim to improve financial health reported greater resiliency during the pandemic and a deep sense of gratitude to their financial institutions. They felt the institution was their partner as they sought to navigate their businesses during the pandemic and were significantly more likely to recommend their provider to others.

Introduction

Financial inclusion is more than just connecting people to a bank account. People need financial tools that they trust, use, and benefit from, so that entrepreneurs can hire more employees, parents can save for the future, families can weather economic shocks, and communities everywhere can accelerate social and economic progress. The COVID-19 pandemic has highlighted the importance of well-designed financial tools, especially digital ones, to help low-income populations build resilience to weather prolonged income shocks.

While access to financial services has advanced during the last decade in Latin America, many consumers who have gained access have not taken full advantage of their newly acquired services. As of 2017, 17 percent of accounts in Latin America and the Caribbean sat dormant.

While access to financial services has advanced during the last decade in Latin America, many consumers who have gained access have not taken full advantage of their newly acquired services. As of 2017, 17 percent of accounts in Latin America and the Caribbean sat dormant.

This is because widely available financial products are not designed to fit most users’ needs, wants, and behaviors. Moreover, we have found that consumers need better support in navigating how different products can help them to grow their businesses, make choices that fit their lives, and reach their ambitions.

To address dormant accounts and low engagement, financial service providers should focus on products that build financial health among users — the ability to meet their current financial needs, absorb financial shocks, and pursue financial goals. Such products are not just good for users, they are good for business. The 2019 US Financial Health Pulse reports that, in the United States, people whose primary institution helped them to improve their financial health were 1.5 times more likely to be satisfied customers and 1.3 times more likely to purchase more products and services in the future. Additional research from Albania has shown that financially-healthy customers exhibit better financial behaviors; they use a more diverse range of financial products and services and use them more actively. And finally, Gallup found that when customers feel that their bank is looking out for their financial well-being, they are much more likely to be fully engaged with that bank.

By helping consumers build their financial health, FSPs can help customers become more informed and engaged; in other words, they become better customers. Moreover, as competition among FSPs continues to grow, providers that can serve those with unmet needs will win loyalty and growth.

Our approach

For decades, Accion has helped FSPs around the world deliver products that unserved and underserved client needs from the formal financial sector. The Accion Global Advisory Solutions team is committed to delivering high-quality, affordable solutions for the billions of individuals who are still unserved or underserved by the financial sector. We combine human-centered design with insights into emerging technologies and effective business models to create financial services that accelerate social and economic progress.

In our view, to build financial health, FSPs need to put customers at the center of the design process and ask, “How can we better understand the challenges that our customers face, and how can we help them tackle these issues through our services?” Accion helps FSPs on this journey to understand the customers’ key pain points and develop tools, exercises, and advice that will build customer’s financial knowledge, skills, and attitudes.

In 2018, Accion launched a partnership with MetLife Foundation to support five institutions in Chile and Mexico to develop products and services clients can trust, use, and benefit from. Over the last three and a half years, we worked closely with our FSP partners to create innovative solutions and services that help underserved families and businesses improve their financial health outcomes, become more resilient to shocks, and take advantage of opportunities that come their way.

In Mexico, we partnered with two cooperatives: Caja Bienestar to launch a supply chain finance product and Caja Popular Cerano to develop a savings product for youth. In Chile, we worked with three fintech organizations: we supported the revamp of a financial health portal with Destácame, a business management application with Organizame for Fundacion Banigualdad’s clients, and a crowd-funding platform for microentrepreneurs with RedCapital.

Across all projects, we tracked impact in five specific areas of financial health that together suggest levels of resiliency and ability to take advantage of opportunities:

- Overall feeling of financial well-being: Assess feelings of satisfaction with regard to users’ financial lives, and the extent to which thinking about finances causes stress.

- Business management: Consider whether business owners feel confident about the financial sustainability of their businesses in the long run.

- Debt management: Evaluate how well people are managing their existing debt and the extent of access to external resources, if needed.

- Savings and long-term planning: Observe whether users are building and maintaining short- and long-term savings based on their financial goals.

- Budget management: Understand what tools are being used to manage personal, family, and business budgets to prioritize expenses and assess profitability.

These aspects of financial health were assessed via short, digital surveys among potential customers before product launch, and again several months after product launch. Due to small sample sizes, we were not always able to achieve statistical validity with our results, but we believe the directionality is still promising. Moreover, these products are still relatively new to the market and early days in terms of customer uptake and traction, so impact is likely underestimated.

A note on timing

We experienced many challenges throughout the product development process: political insecurity, strikes, violence that made travel impossible, and, of course, the pandemic. Building an innovation mindset to financial institutions is never easy since FSPs are generally conservative, risk-averse institutions, and political, social, and natural uncertainty has made change even more challenging. Though our teams were able to conduct in-depth research through direct engagement with users at the onset of the project, our interactions with end-customers were entirely virtual from March 2020 onwards. These shocks delayed several product launches as our partner institutions shifted their attention to more immediate and pressing priorities.

Furthermore, many of our end-clients also experienced health challenges and losses during this period. Most experienced disruptions in their business or were forced to shutter their doors and reinvent their livelihoods amid uncertainty.

Nine months into the pandemic, we surveyed our partners’ clients to validate whether the product concepts we conceived before the pandemic would continue to be relevant, useful, and helpful as they sought to navigate and recover from the pandemic. We overwhelmingly heard from users that products that could give them the working capital they needed to keep the lights on, tools to manage their budget and their debt, and digital records for their business were exactly what they needed to keep their financial lives on track.

In all, we hope that the lessons shared here will help other institutions develop and launch innovative products that empower their customers to make choices that fit their lives and build habits that improve their financial health, so they can improve their resilience to shocks and reach their ambitions.

Case Study: Caja Bienestar

In Mexico, 99 percent of all businesses are micro, small, and medium enterprises (MSMEs). They contribute 52 percent of GDP and generate 72 percent of jobs in the country. Although MSMEs play a crucial role in Mexico, fewer than 10 percent of them have received a bank loan.

Located in the heart of central Mexico, Caja Bienestar is meeting the needs of MSMEs. It is the largest socially focused financial institution in the country. Now entering its 25th year, the institution has more than 80,000 active microentrepreneur clients. Since its inception, Caja Bienestar has offered a variety of low-cost, high-quality financial services to its clients — both for personal and business purposes — and continues to be one of the most affordable credit options for small businesses and families in Central Mexico.

However, there remained two distinct segments that Bienestar had not able to reach with their current offering. The first included microentrepreneurs, who, due to their business size, lack of documentation, and low or non-existent credit scores continued to lack access to credit, even from socially focused lenders like Caja Bienestar. The second segment included microentrepreneurs that have the necessary documentation and credit histories to obtain credit but may lack the financial capabilities that would enable them to take out a loan confidently. For example, these entrepreneurs may not know what type of credit to apply for, may find it difficult to understand interest rates, or may be afraid of finding themselves deep in debt.

As a result of these challenges, these segments of MSMEs in Mexico often obtain the financing they need to purchase inventory from their suppliers, who they know and trust. MSMEs often find it more convenient to access informal credit from suppliers, where there is no need for collateral or paperwork. This short-term credit, with clear fees and schedules, is easier to understand than formal credit. However, such credit is not reliably available and can be expensive. Moreover, not all distributors offer such credit, as it requires them to carry the risk of late repayments, and the risk of theft upon collections. This reluctance means that many MSMEs are left without sufficient access to credit to fuel their business operations.

The solution

To extend credit to informal MSMEs — that lack credit scores or distrust formal financial services but require liquidity to manage inventory — Caja Bienestar developed a revolving credit line product. The team knew that the credit product would have to be deeply customer-centric and tailored to the specific needs of the MSMEs that Bienestar had not previously been able to serve. The working capital loan, with attractive and competitive fees, was designed to not require a credit score, and instead uses information and recommendations from third-party wholesale distributors to assess risk. These distributors have sold to these businesses for many years, often extending them in-kind credit, and can therefore provide reliable assessments of their creditworthiness. In all, several innovative features that make it particularly well-suited to growing the financial capabilities of microenterprises:

- Fee-based credit rather than interest rates. While most loans include interest rates, Accion’s research with customers found that such calculations are difficult for many microentrepreneurs to understand. Instead, the researchers found that defined fees are easier to grasp and can help shopkeepers better calculate the profitability of various aspects of their businesses. However, it is worth noting that, since various providers describe their pricing in different terms, it can be difficult for users to compare prices, so Bienestar’s loan officers make themselves available to help potential clients understand what option is best for them.

- Pre-approved credit based on information from distributors. Using information and recommendations from distributors, Bienestar pre-approves groups of microentrepreneurs to access credit to replenish their product inventory. The sales and payment information from distributors has served as a valuable substitute for credit history, allowing Caja Bienestar to sufficiently assess creditworthiness for those without formal credit histories.

Distributors also benefit from this arrangement, as they can optimize their sales and transfer the risk of giving credit to Caja Bienestar. For Caja Bienestar itself, the information received from suppliers helps them get to know their customers better and make more informed decisions regarding the MSME borrowers’ debt, reserves, business inventory, and operations.

- A digital simulator to help MSMEs make informed decisions and prevent over-indebtedness. As MSMEs often lack an understanding of their own margins or costs of capital, the team built a digital simulator that MSMEs can use to determine what loan terms they need to finance their inventory. The tool calculates whether the expected profits from the sale of their inventory will be enough to cover the cost of credit. It then guides them to consider different terms or amounts based on their profitability levels.

- A go-to-market strategy closely tied to key customer pain points. Marketing materials for the product provided customers with tips and advice about how to better understand the cost of credit and how to manage their debt. Loan offers were also trained to help clients calculate what their monthly sales would need to be to pay back credit, and ultimately determine whether they should take out a loan.

By offering entrepreneurs access to credit as well as free use of the digital simulator and complementing the approach with a communications strategy oriented around building financial health, Bienestar provides underserved entrepreneurs a low-risk way to grow their businesses while building their confidence to adopt and use credit to grow their businesses and manage their debt. The product, Bienestar para tu Negocio, was launched in January 2020 in partnership with six trusted, local textile and construction distributors that provide goods to MSMEs. With Bienestar para tu Negocio, entrepreneurs finally have access to the credit they need and the opportunity to grow their businesses. Over time, this financing will help MSMEs smooth their income and remain resilient in difficult periods.

Customer Spotlight: Maria Olga

Maria Olga is a microentrepreneur, she lives with her husband and children in Querétaro, Mexico. She opened her own business four years ago, where she sells a little of everything: spray paint, tools, bicycle parts and even cement and plaster. Lately, she was facing difficulties; customers came to her business to buy certain products, but she did not have capital available to purchase it because her resources were already invested in inventory. She did not dare to acquire a loan, because she thought that it would not be given to her, and she was afraid that the interest rates were very high. One day a supplier told her about the Caja Bienestar product loan, and she applied. Now, Maria Olga can stock her business with everything she needs and learned that she can pay off a loan in the time it takes her clients to pay her. She no longer loses customers due to lack of inventory. She feels very grateful because someone trusted in her.

Results

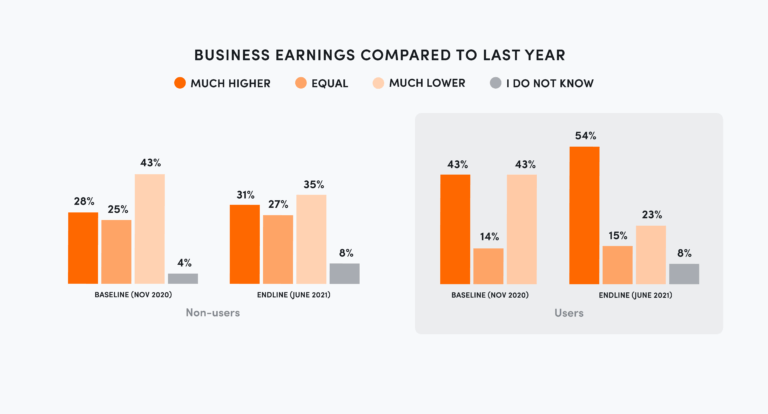

During the pilot, the credit product had 14 active users, each of whom has received an average of 18 rounds of credit since January 2020, demonstrating significant recurring use. Ten of these individuals are first-time credit users. Of those that have used the credit product, nearly 70 percent are between the ages of 26 and 45, 65 percent have had their business for over five years, and the majority describe their business as being in the commerce or transportation sectors. To date, 327 people have used the simulator to determine whether they should take out credit.

To understand the impact of the credit, the team asked both those who received credit as well as some who did not, a series of questions about financial health at the beginning and end of the pilot in November 2020 and June 2021, respectively.

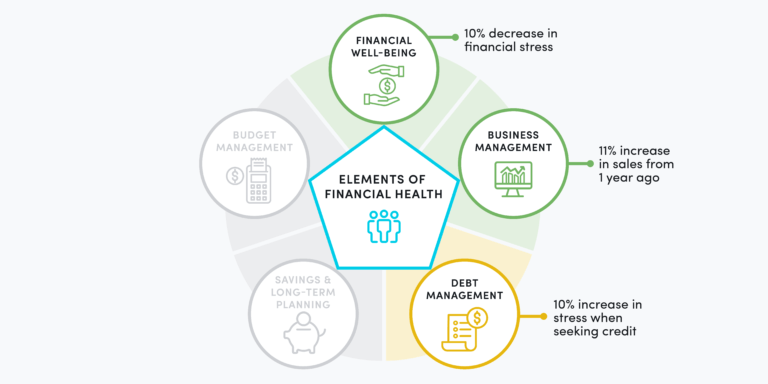

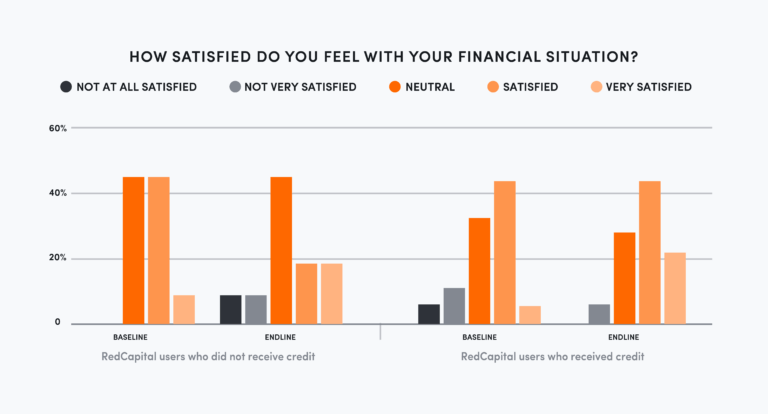

Overall, we found that use of the Bienestar para tu Negocio credit product is correlated with improved feelings of financial well-being, greater resilience to the shock of the pandemic, but we also saw an increase in stress among users when thinking about taking out credit—likely due to increased business uncertainty as the pandemic continues.

Overall financial well-being

Feelings of overall financial well-being among Caja Bienestar’s clients who took out a line of credit improved significantly when compared to those in the control group (those who did not take out any credit). In the group that received credit, the percentage of respondents that said their financial situation caused them stress decreased by nearly 10 percentage points in the time since the product launched. For those that did not receive credit, feelings of financial stress increased by nearly 5 percent over the same time period.

Business management

The group of clients that received credit also reported being more able to manage their businesses than those in the control group. They reported a faster recovery after the pandemic and higher profits than this time last year. They also reported fewer instances of lost opportunities due to lack of liquidity or inventory.

Debt Management

Understanding what interest rate is best when seeking credit is an important skill when choosing a credit product. To test their understanding of debt, respondents were asked what interest rate they preferred when seeking credit. In both the group that received credit and those that did not, a large percentage could not identify the best interest rate. In addition, users of the Bienestar para tu Negocio product reported an increase in stress when seeking credit from a cooperative of a bank (an increase of 10 percent). These key findings demonstrate a need to further strengthen knowledge around how to choose between credit products and build greater confidence in managing debt.

However, those that used the simulator tool expressed greater willingness to take out credit from a bank or credit union to take advantage of bulk purchase discounts from distributors in the future, demonstrating an improved understanding of when it is appropriate to seek credit.

Key takeaways

As noted earlier, interest rates can be difficult to understand and require complex calculations to assess the impact on profitability if using credit to purchase inventory. Conducting a scan of your target customer’s financial knowledge, to understand their current state, is critical for any financial services institution seeking to improve their clients’ financial health and product uptake. With this insight in mind, Caja Bienestar designed a fee-based working capital credit product rather than relying on traditional interest rates to communicate the product’s terms in vernacular that their customers understand.

Globally, the digital divide presents a challenge for even the most customer-centric digital products. During the customer research phase, Bienestar’s small merchant customers expressed anxiety about using a digital device to complete a credit application as many continue to use feature phones and do not have access to smartphones. Others that do have access to smartphones noted a feeling of insecurity in providing their personal details online or simply did not know how to navigate the application on their phones.

In response, Bienestar has trained its salesforce to teach clients how to use the digital tool and developed a chatbot to provide answers to quick questions for those that are more digitally savvy.

Over the seven-month evaluation period, those who utilized the working capital product saw improved outcomes across various aspects of their financial health. Those who utilized formal credit to finance their inventory reported being more resilient during the pandemic, less likely to lose sales due to a stock out and reported higher sales than a year before when compared with those who did not take out credit. While the financial health outcomes of those that benefited from receiving credit should continue to be monitored, these findings show that thoughtfully-designed financial capability building products can build resiliency among low-income customers – ultimately creating greater retention, engagement, and loyalty for the financial service provider over time.

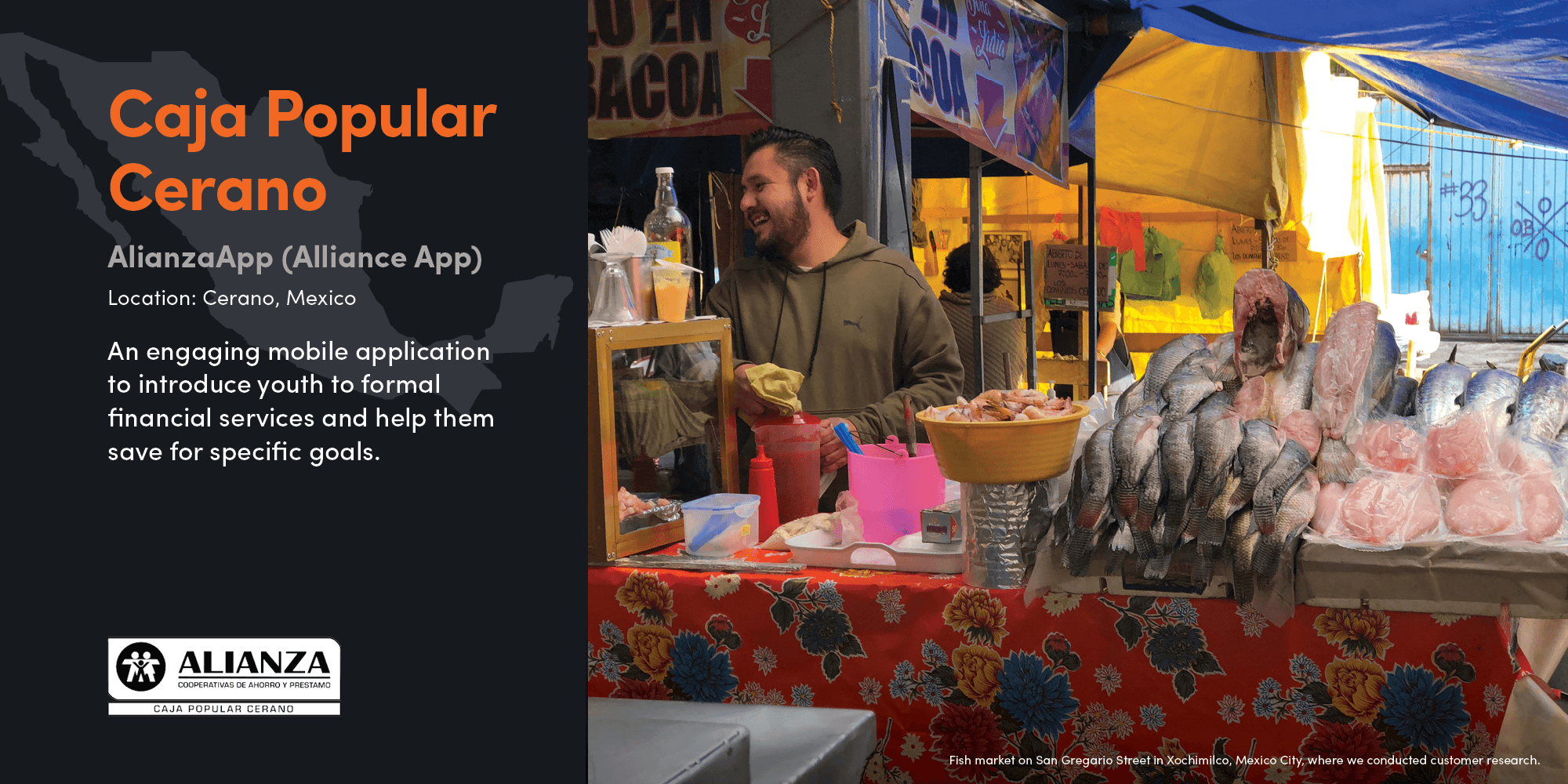

Case Study: Caja Popular Cerano

Only 33 percent of the youth population (ages 15-24) in Mexico are clients of a banking institution, compared to nearly 40 percent across Latin America and the Caribbean. These low rates of engagement in Mexico reflect the fact that young people do not connect with traditional brick-and-mortar financial institutions, which have limited hours and require in-person transactions. Young people are looking for financial institutions that allow them to conduct transactions around the clock, and that use the channels that they use – social media and smartphone apps.

Caja Popular Cerano is one of the many financial institutions that has struggled to connect with young people. It was founded in 1965 as a savings and credit cooperative and is headquartered in Cerano in the state of Guanajuato in Mexico. Today, it has 22 branches and serves more than 100,000 people. Its mission is to extend access to financial services to low-income segments of the population and to improve their users’ quality of life. To do so, Caja Popular Cerano provides specialized savings and loans to the middle-, low- and very-low-income segments, as well as micro, small and medium enterprises. Caja Popular Cerano is part of Federacion Alianza, a federation of 19 cooperatives in Mexico that serves as an umbrella organization to offer its members services such as a core banking system, as well as marketing and product development support.

Although youth people make up a small percentage of current users, Caja Popular Cerano saw an enormous opportunity to serve the urban youth market in Mexico. However, market research showed that many of their current customers’ children were uninterested in opening accounts with Caja Cerano, a break from the past when families banked with Caja Cerano for generation after generation. The institution was finding their customer base was aging and that they were acquiring very few younger ones. To attract and serve young customers, Caja Popular Cerano needed to better understand the needs and preferences of youth, as they think about their own financial lives, and create a new offering relevant to their lives.

The Accion and Caja Popular Cerano teams partnered to conduct in-depth interviews and co-creation sessions with several young students, part-time workers, and self-employed individuals to compile a detailed picture of youth in the state of Guanajuato. These research efforts revealed several key findings that became the basis for the product design. We found that many young people had already or aspired to start their own business—and had ambitious plans to grow. We also found that young people are busy managing many responsibilities at once, including school, work, caring for their families, and starting new businesses, in some cases. Despite having ambitious plans to grow their businesses and careers, young people told us that they usually think about their financial lives in short time horizons, planning how to get through the week, rather than thinking about planning for the future. But in the same vein, young people said they were excited to save for specific projects. Even if they do not make much money, they value saving informally. They like to use mobile apps to keep in touch with friends and for online shopping, however, most lack a credit card or mobile money account. Most people told us that they do not currently use formal financial services, are fearful of taking out loans as the risk of not being able to repay and being blacklisted could be detrimental to their lives.

The research also uncovered the extent to which young people use their phones to access the internet. Nearly 40 percent noted that they spend more than four hours a day on the internet, and 23 percent reported spending 2-3 hours on the internet a day. Nearly 90 percent of these respondents noted that they typically connect to the internet through their mobile phone.

The Solution

In light of the research findings, Accion worked with Caja Popular Cerano to develop a platform that would motivate young people to develop a saving discipline that would enable them to reach their future ambitions and help them develop positive credit scores over time. The team helped Caja Popular Cerano build their internal capacity to develop their first digital product: AlianzApp, an application that allows youth to put money aside weekly for a particular goal, either by putting money into savings or by taking out a very small loan. AlianzApp encourages young clients to save regularly and for specific purposes, borrow when they need, learn the value of a positive credit score, and build trust in formal financial institutions. By cultivating these capabilities in younger clients, Caja Popular Cerano will help customers thrive throughout their financial lives, starting with the app, which will likely be the individual’s first interaction with a financial institution.

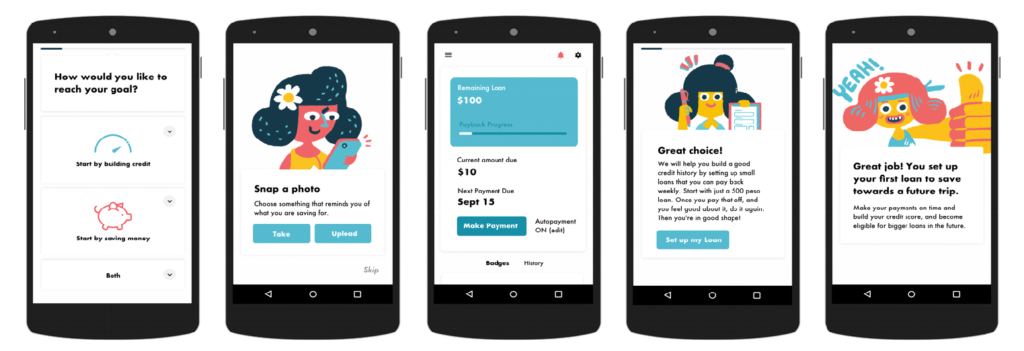

To craft a financial services app offer that meets the preferences and expectations of young people, key features of the AlianzApp include:

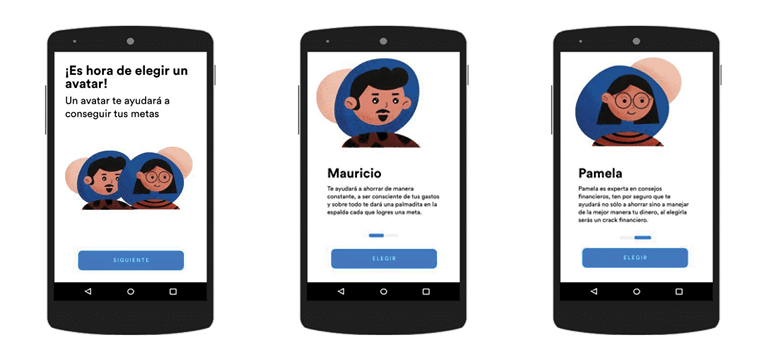

- Use of avatars to personalize and send timely advice. The app allows youth to choose an avatar, Mauricio or Pamela, who becomes a source of financial information throughout the youth’s journey. As the user saves or takes out credit, Mauricio or Pamela gives them advice, sends messages or nudges as needed. For example, if a user has not made a loan repayment for more than two weeks, they receive a reminder that not repaying can impact their credit score.

- Built-in calculators to simulate time horizons for reaching their savings and loan goals. In our research, we found that it was very hard for youth to calculate the duration of a loan, or how long they would need to save to purchase something. By including a simulation tool in the app, users can see how long they need to save or to pay off a loan. In the app, users are presented with a dashboard that indicates how much they would need to save a week, and over what time horizon, to meet their goals. The dashboards are designed with flexibility in mind; the user can easily see how their savings requirements change as they change one variable.

- Motivating in-app messaging. The user also receives helpful tips about saving and paying back loans via notifications when they use the app. Additionally, the app has built-in motivational markers that show users whether they’re on a ‘streak’ (saving or paying consistently), how close they are to finishing a goal, and reminder messages if they have skipped a payment—and users receive badges when they have accomplished a goal. One of the overwhelming lessons we learned during interviews and prototyping is that youth value validation and celebration. The app includes six badges to incentivize use and continued savings and loan payments.

- Automated save and pay options. The application allows users to save or pay their credit automatically, with self-save and self-pay, features that were new to the institution. They allow for payments to be “out of sight, out of mind” for those who opt in.

Outside of the app, the team understood that the application could only be helpful if youth can easily find a place to deposit money. For this reason, the bank built a banking partnership so their young customers can make deposits at any BBVA branch, ATM, or banking agent (which includes OXXO, the largest network of kiosk and convenience stores in the country). This partnership provides a huge network of cash-in points for youth.

Results

Due to regulatory delays, AlianzApp has not yet launched, but the team expects its launch by the end of 2021. Given how promising the product is, the Federacion Alianza has expressed interest in expanding AlianzaApp to the other 18 cooperatives in the network. To support this growth, Accion has amplified the development of the product to ensure that once it is ready to launch, any cooperative in the network can offer it to their clients. The team is working with a local digital marketing firm to develop an ad and social media campaign to engage with youth and ensure that they learn about the application. The marketing tagline for the product is, #Financialloveexists or #ElAmorFinancieroExiste.

Customer Spotlight: Alejandra Rico

Alejandra Rico is 22 years old and currently is studying business management engineering at Guanajuato University. Saving is important to her because it can help her with unexpected expenses. She thinks that going to bank branches for transactions or to check your account movements is a waste of time, especially for young people who are looking to optimize their time. After testing the Cerano app, Alejandra noted that it can be helpful in helping her to control her expenses, and to create a saving habit since the app allows her to define a goal and track progress toward reaching it. Alejandra says the app will create a positive impact in her life via the advice and guidance it provides in setting up goals step-by-step, which is really easy and clear for young people.

In our business case projections, we assumed that at least 10,000 users would adopt the product in the first three years. Today, there are less than 10 cooperatives out of 150 in all of Mexico that have digital financial services offerings for their users, and this will be the first digital offering specifically tailored to youth. As such, we expect that many cooperatives will be motivated to adopt this offer, in which case, its reach will scale dramatically.

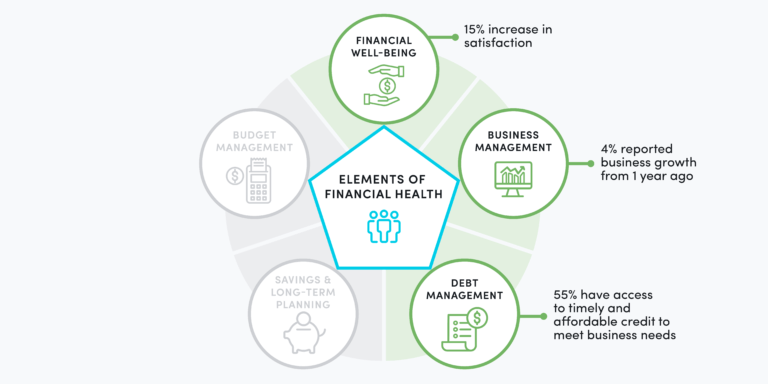

Overtime, we expect that the use of this app will result in improved measures of overall financial well-being of its users, improved ability to manage debt, and finally, greater capacity to save and plan for the long-term.

Expected financial health outcomes from the use of the AlianzApp:

Key takeaways

As we look forward to this product’s launch later this year, key takeaways from the process of developing of a product targeted for youth include:

In a survey disseminated to the target market for this product, youth respondents noted that they felt that investments and education were good reasons to take out credit, and that making nonessential purchases was not. However, when asked why they have taken out credit in the past, nearly 50 percent of the respondents said that they took it out to make a large purchase. Behavioral science studies have shown that people only sometimes do what they say they will do, often in predictable ways. These insights are helpful for determining what key messages to send through the application. It might be smart to appeal to what people say they want, but to plan for what they do in practice.

To encourage sustained behavior change, institutions need to embed healthy financial habits within everyday practice and action and encourage frequent interaction with the user. The target market for Caja Popular Cerano reported being online several hours of every day. Designing this product as a mobile app, where the youth population is likely to be already, was critical.

Behavioral research has found that products like automated savings accounts and direct debit payments have success when they reduce decision-making fatigue and make saving and expense management feel effortless. Our customer research showed that youth think about their finances and set money aside through informal savings mechanisms, every week. The team set up the app so that users can automate their existing behavior within a formal structure and use a digital tool to keep better track of their finances and improve their financial health over time.

As more customers demand products that uniquely cater to their needs and values, taking an innovative approach to product design is crucial. It is therefore critical that the entire business — from the Board all the way down to officers — is aligned with the firm’s priorities and objectives. To ensure alignment across all teams involved in the product development and rollout, Caja Popular Cerano created an extended team in the organization with representation from different divisions to ensure ideas resonated across the organization and to promote buy-in from all stakeholders. Ultimately, leadership paved the way for the team. Today, the CEO remains committed to building a culture of financial health, enabling the team to ensure it becomes embedded in every area of the business.

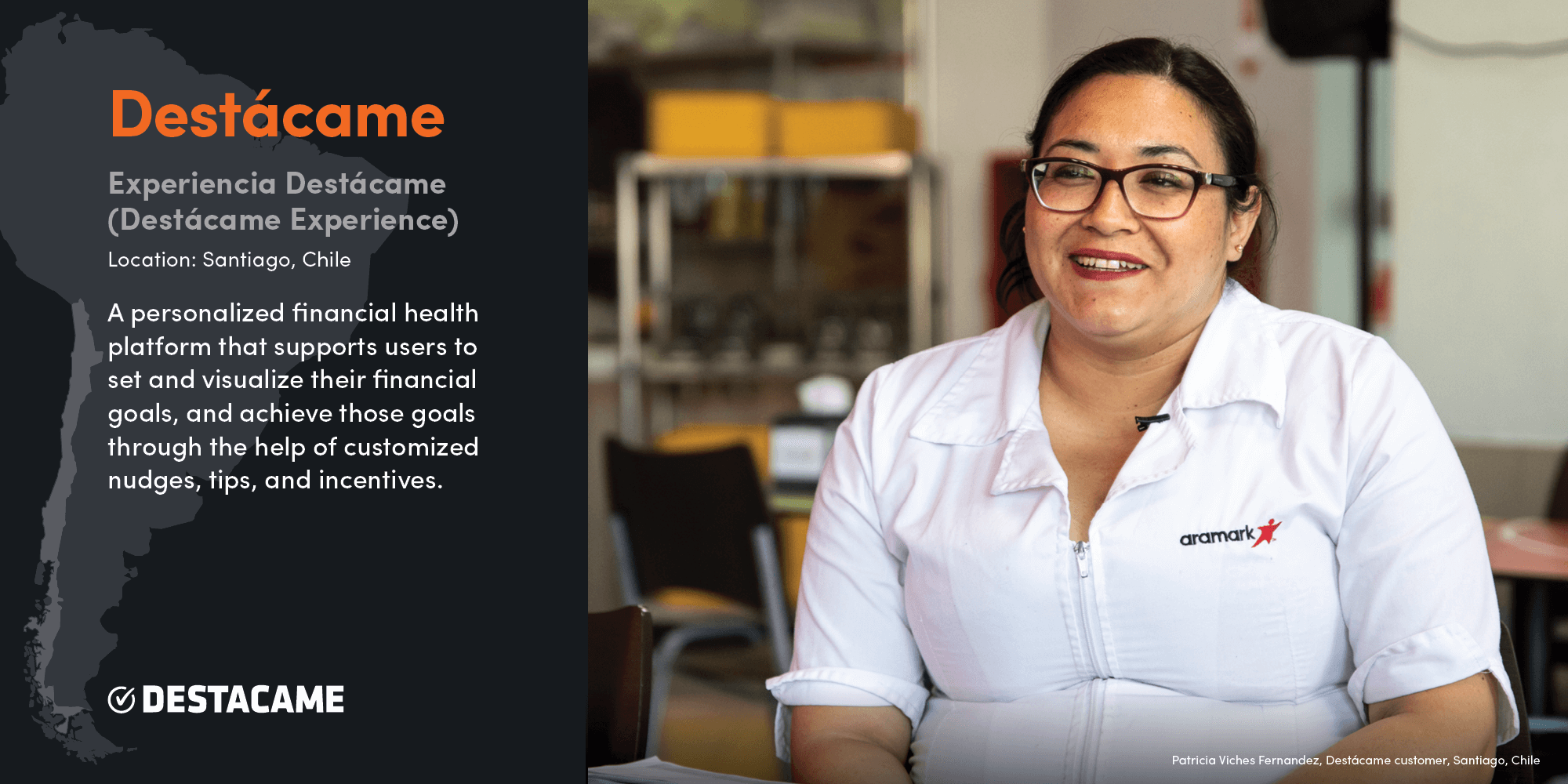

Case Study: Destácame

In Chile, 53 percent of the population is financially insecure, or at-risk of falling into poverty if they had to forgo three months of income. Accion’s research in Chile shows that many Chileans feel significant stress over their financial well-being, lack confidence in interacting with the formal financial sector, and have difficulty identifying how products and services can help them achieve their financial goals. The pandemic has only exacerbated feelings of financial insecurity in Chile.

Destácame is a personal financial management platform that seeks to empower individuals by raising their awareness of their own financial situation and facilitating access to financial products and services. On the Destácame website, users can review their credit report free of charge, access discounted options to pay off debt, review product offers from different entities, and learn tips to improve their financial situation. Destácame operates in Mexico and Chile, has over three million registered users, and partners with over 30 financial service providers.

Destácame’s site began as a marketplace to provide users with immediate access to many products and services as soon as they logged onto the site. While the offering was extensive (including credit reports, credit offers, credit cards, and debt reduction), it was not personalized. The original structure worked well to quickly grow the user base, but it did not promote Destácame as a long-term partner or financial health resource; only 11 percent of users were returning to the site month-over-month.

Accion partnered with Destácame to conduct market research, where we found that users feel stressed and alone in the face of managing their finances and financial challenges. We found that this emotional burden adds to daily challenges and manifests in different ways – some actively avoid dealing with their financial obligations, while others think about nothing else. Some people choose to believe that ‘nothing bad will happen,’ while others focus on just getting through the day rather than longer-term financial planning. We learned that people tend to prioritize current consumption without considering the healthy balance between income and expenses. Most users told us that they have no system in place to budget their expenses and were often unable to pay their expenses at the end of each month.

The Solution

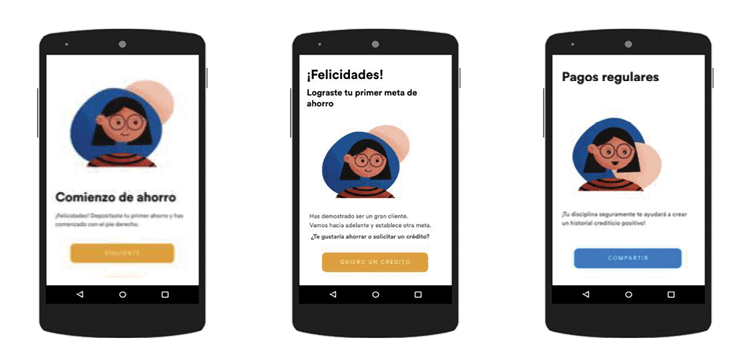

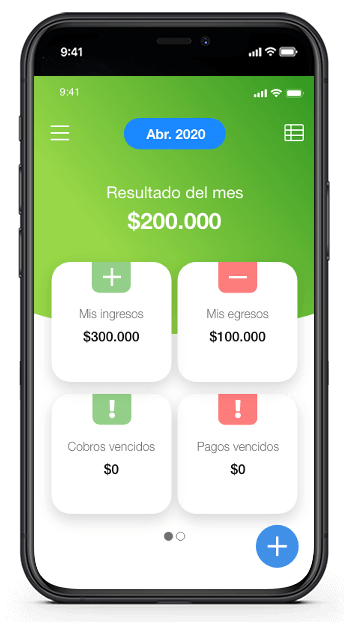

Destácame knew that their users needed more than just access to financial products – they need an advisor to help them navigate their financial lives, manage a budget and debt, save for the future, and become more resilient to shocks. The fintech, in partnership with Accion, set out to revamp and expand its platform to create a fully customized user experience, Experiencia Destácame, to allow customers to set, visualize, and work toward their financial goals through simple diagnostics, personalized user journeys, and digestible tips, tools, and product recommendations. Rather than adding products or features to its platform, the Experiencia Destácame project involved changing the core of Destácame’s business and re-envisioning its value proposition around financial health. This revamping of the platform provides a more comprehensive experience for its users, improve retention and engagement so as to improve customer lifetime value.

The Accion and Destácame teams developed several personalized tools for Experiencia Destácame to better support the financial health of the platform’s users:

- Diagnostics that assess the user’s financial health and personalize their experience. When a user arrives at the Destácame site, they can take a diagnostic that assesses their financial health in three main categories: budget management, shock resilience, and long-term planning. Based on their responses to the diagnostic, they are qualified as good, neutral, or bad in each category, and provided with suggestions and tips for how to improve their standing. They also receive recommendations for relevant products based on their financial needs.

- A budgeting tool to ensure users can save for the future and become more resilient to shocks. Based on users’ responses to the diagnostic, they may be directed to Destácame’s budgeting tool. This tool provides users a step-by-step, user-friendly approach to building a budget. Users are walked through a series of screens to add income and expenses and calculate their savings. It also provides users with guidance on how much money they can set aside each month to pay off any existing debt, so that they can improve their creditworthiness over time. Design elements were incorporated throughout to provide guidance and encouragement, including easily accessible definitions, quick tips, and an informal, user friendly, positive prose.

- An expense reduction tool that helps users better manage their monthly cash flow. Users may also be guided to an expense reduction tool, which helps them manage their monthly cashflow by setting goals to reduce expenses in key categories and entering spending once a week to assess progress. The tool is designed to be flexible enough to meet user needs (for example, selecting the day to receive reminders) but structured enough to encourage action using positive language and support.

These tools are easily accessible on mobile devices, require little time to complete, and quickly demonstrate and reward progress towards better financial habits. All the tools are also closely linked to each other. For example, after a user completes the budget, she may see that she is spending more than she’s bringing in each month and be prompted to work on reducing expenses via the expense reduction tool. After reducing expenses, she may be encouraged to start saving, and provided with recommendations for relevant savings products.

Results

Since launching in early 2020, over 1.25 million users in Chile and Mexico have visited the redesigned site. Almost 65,000 have completed the diagnostic, 128,000 have accessed the budgeting tool, and 30,000 have accessed the expense reduction tool, as of July 2021. These conversion rates are consistent with broader usage of Destácame products – and are impressive for self-driven tools. Survey data and usage metrics were collected before using the platform and again 12 and 18 months later in order to assess the impact of the Destácame platform on financial well-being.

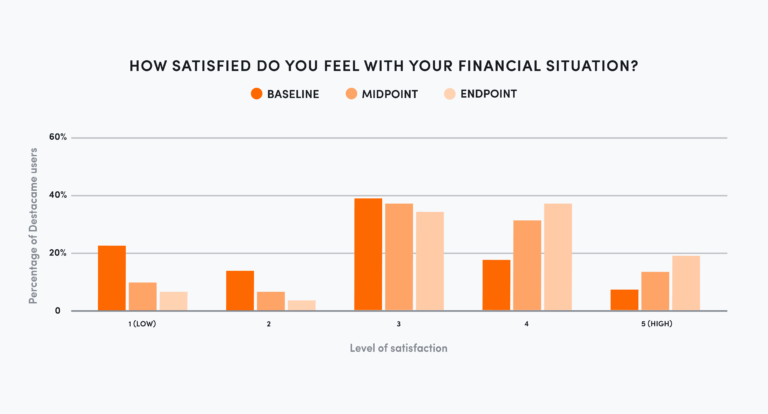

Overall feeling of financial well-being

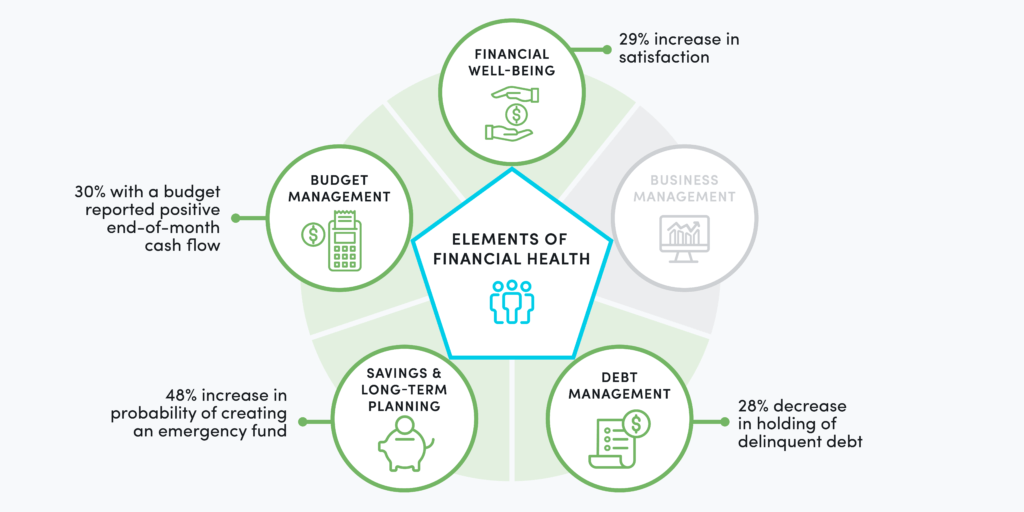

Experiencia Destácame users were asked about their level of satisfaction with their financial situation. Survey results show a large increase between baseline and final measurement (a 23 percentage point increase of those stating that they agree or strongly agree that they are satisfied with their financial situation). Since this study did not include a control group, it is hard to know how much of the changes to attribute to the platform although our statistical analysis did include controls for various contextual variables.

Savings and planning

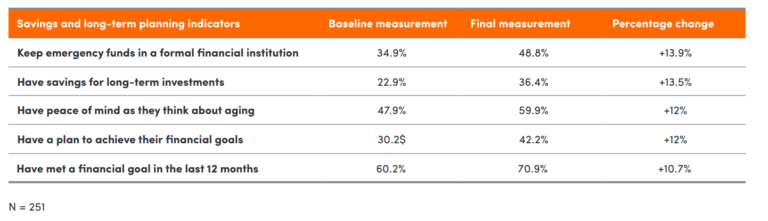

Over the evaluation period, the number of Destácame platform users that place importance on savings increased. There was also a notable increase in the number of users who have emergency funds, keep their emergency funds in a formal institution, have long-term savings, have a sense of financial security as they age, have plans to achieve financial goals, and have fulfilled a financial goal in the last twelve months.

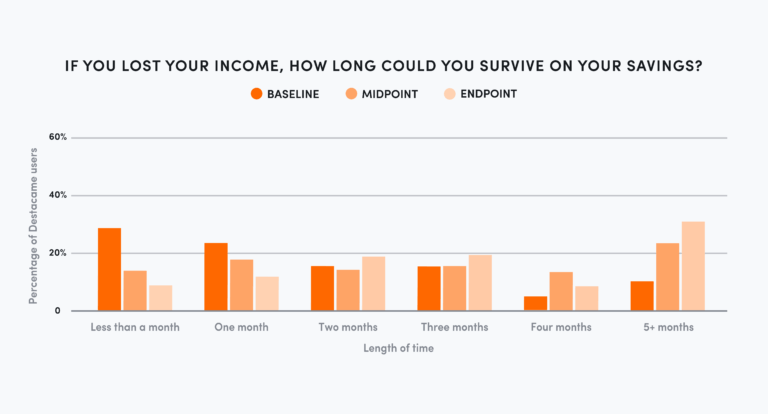

Users of the Experiencia Destácame platform articulated greater resilience than they did before they began using the platform. The proportion of users that stated that they would be able to survive for more than a month if they were to lose income, increased by 32 percentage points compared to the baseline.

Budget management

Usage data of the Destácame budget tool shows that 34 percent of users accessing the budget tool were creating a budget for the first time, 30 percent achieved a positive end-of-month cash flow, and 8 percent said they were able to decrease expenses through usage of the tool.

Since only some of the platform users used the budgeting tool, we were able to compare their responses to those who used the platform but not the budgeting tool. Among those who completed the budgeting tool, the percentage of users that reported spending more than they earn each month increased from 20 percent in the baseline to 27 percent in the endline. Among those that did not complete the budgeting tool, the percentage that reported spending more than they receive monthly decreased from 30 percent to 20 percent.

In addition, those who completed the expense reduction tool reported a higher willingness to recommend the Experiencia Destácame platform to family and friends. The Net Promoter Score (NPS) among those using the tool was equal to 55.56, higher than the NPS of 51.12 for the overall use of the platform.

Debt management

The number of Destácame users with delinquent debt decreased significantly over the course of the project (52 percent in the baseline to 24 percent in the final measurement). Results also showed an increase in the number of users that feel that their level of debt is manageable.

In addition, users that were able to pay off debts using the discount provided by Destácame reported a higher willingness to recommend the Destácame platform to family and friends than did clients who have not used the Experiencia Destácame platform to pay off debt. The average willingness to recommend the platform measured on a scale of 0-10, was 9.44 for among those who leveraged the platform to pay debt, versus 8.45 for those who did not.

Key takeaways

Destácame knows that their users like the idea of being financially healthy but that they are often too overwhelmed and tired to invest energy into improving their financial health. The vast majority of Destácame users come to the site to access their credit report free of charge or to explore potential discounts on outstanding debt.

To help their users become more financially healthy, Destácame took a ‘trojan horse’ approach to financial health recommendations, linking the topic closely to popular products by integrating short tips alongside the product journey, embedding links to the dashboard, and suggesting diagnostics as a natural part of the user experience, rather than leaving financial health as a standalone section. Nearly 40 percent of users that completed the diagnostics had first accessed their credit report.

To encourage sustained behavior change, institutions need to embed healthy financial habits within everyday practice and action. Destácame’s dashboard and tools are designed to be user-friendly; they feature a clean design and warm, informal prose, provide options for support throughout, and minimize the information request from the user. Where possible, efforts were made to cross-reference or replace requested information with user data from other parts of the site.

However, by their nature, both the budget and expense reduction tools depend heavily on inputs from the user, who must complete all income and expense fields to generate their monthly budget and record weekly expenses against their expense goals. This limits their impact to users who are highly motivated and will take the time to update the tools. As a result, usage of these tools is consistent with the conversion rates of other aspects of the Destácame site, however, driving further usage has been challenging — only 15 percent of those who have started the budgeting tool have completed it, and only 7 percent have returned to update their budget within 6 months. Of those that have accessed the expense reduction tool, only 17 percent have set an expense reduction goal for themselves.

Understanding these limitations, Destácame is in the process of launching a mobile application and debit card that offer significant opportunities to streamline and automate assessment of and support for financial health, and reduce effort for users. Budget and expense management will be synced with card transaction data, removing the need to input this data manually. Users will have the option to create savings ‘pockets’ with specific goals assigned; this may include a ‘rainy day’ pocket to build resilience. In the long term, they will also be able to classify expenses, as well as project and simulate cash flow to better plan and prepare for future events. Push notifications and emails will also be incorporated to provide targeted advice and promote healthy financial habits.

Beyond the platform changes the team made to create Experiencia Destácame, the team also developed a new monthly-paid subscription product, DestácamePro, which offers users ongoing access to discounted products and personalized advisory to support users in improving their financial health.

During the pandemic, institutions in Chile were eager to provide their employees with additional support for their financial health in order to decrease financial stress, improve overall health and therefore work performance. In response, Destácame developed a corporate version of their Pro product, which provides employees of an institution with Pro benefits and offers the institution high-level reporting on the state of financial health within their institution. To date, DestácamePro has 16,000 users and 6 corporate partners, with the intent to grow the number of users to 28,000 by December 2021.

These new business opportunities depended on the strong reporting framework that allowed the team to demonstrate impact. Early on, the Destácame and Accion teams established usage and impact indicators that could be measured monthly to understand progress and inform changes. A ‘SWAT’ team that included designers, developers, and business analysts met monthly to analyze results, discuss responses, and implement updates. The team now has 14 months of data on over 1.2 million users, which has provided a strong business case for potential partners.

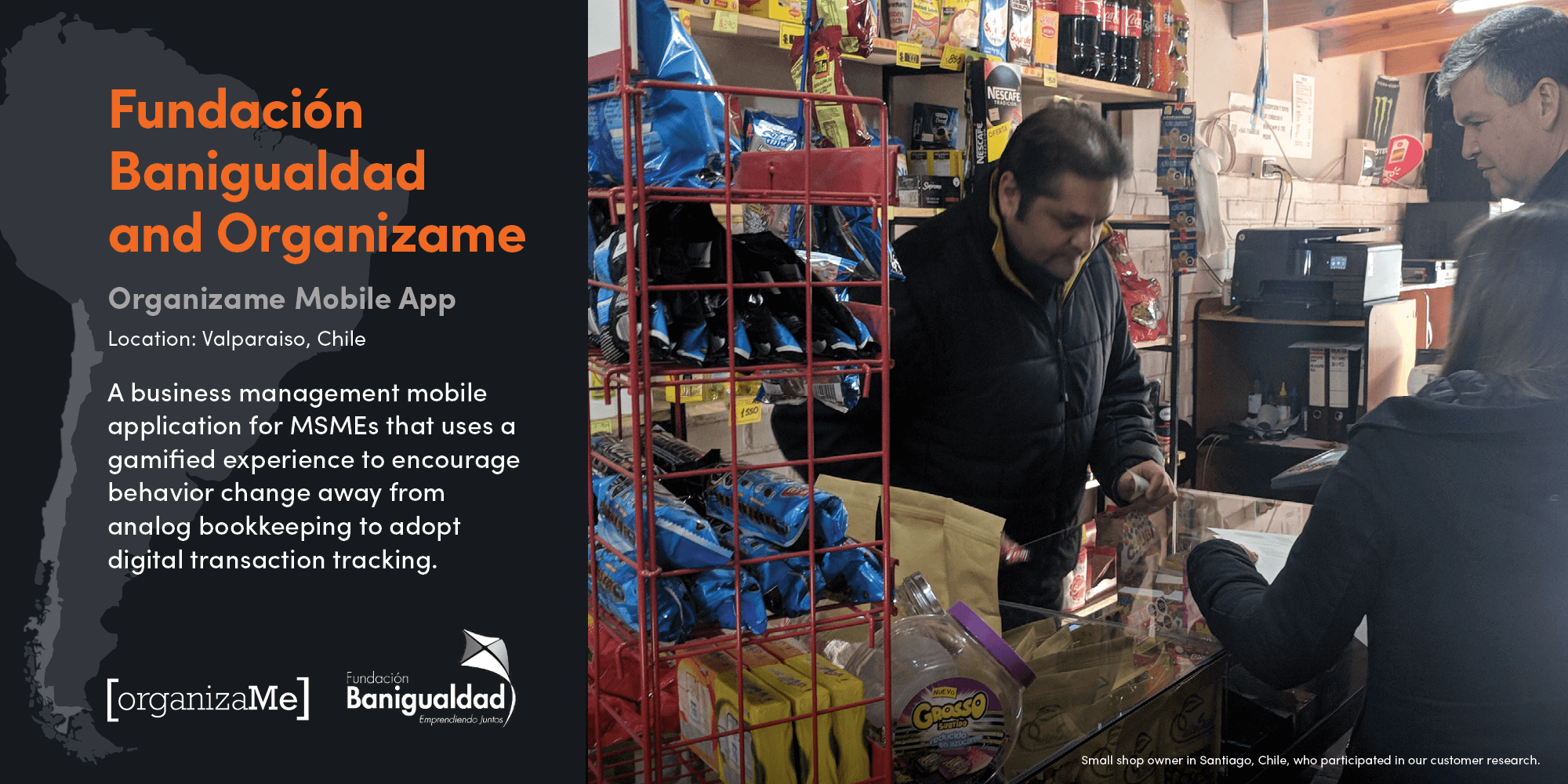

Case Study: Fundación Banigualdad and Organizame

Eighty-two percent of Chilean nationals report being internet users, a figure significantly above the region’s 72 percent average. According to the same report, 99 percent of Chileans that use social media, access social media via a cell phone. Despite the prevalence of digital tools and usage in Chile, many microentrepreneurs continue to use notebooks to track their income and expenses, rather than digital tools that can help them to manage their business , maintain business records, calculate profitability, and plan for the future. These manual behaviors persist and are difficult to change.

In this context, Fundación Banigualdad is a nonprofit organization that helps low-income microentrepreneurs access traditional financial services, giving them greater economic opportunity and equipping them to endure instability. In addition to issuing microloans, Banigualdad provides users with basic training in finance, marketing, sustainability, and business strategy. Today, the Fundación has just over 35,000 clients.

One of Fundación Banigualdad’s clients is Ms. Cecilia, who owns a small shop where she sells everyday items like food, cleaning supplies, and small gifts. While Cecilia knows when her shop is making money, she does not know what her actual profits are on a monthly or annual basis. This is because Cecilia and her husband track sales in several notebooks. When making a sale, they simply reach for the closest notebook and record the item and price sold. However, this process makes it very difficult to balance their accounts.

This process is typical of many informal microentrepreneurs around the world. While this casual approach to tracking income gets small business owners through the day-to-day, it can hold them back from building longer-term financial health. Without knowledge of their profits, it is hard to make effective, strategic long-term decisions and better prepare for unstable times. Moreover, without an accurate picture of profitability it is difficult for informal microentrepreneurs to begin the process of formalizing their business—which provides greater opportunities for access to credit and government subsidies.

Organizame is a Chilean fintech company that was founded to help formalized small businesses track their sales and expenses digitally and issue electronic invoices. The Organizame website helps digitize business functions like cash flow management, bill payment, and credit applications to help entrepreneurs consolidate business transactions and send electronic documents. In tracking sales and expenses, the application captures significant data on merchant revenue streams that entrepreneurs can use to formalize their businesses and financial service providers can also use to assess credit capacity and offer credit at better prices.

While the Organizame solution is helping many small businesses, informal MSMEs like Cecilia’s were not among their typical users. The team found that informal merchants don’t actively search for a digital solution and even when presented with one, are reluctant to adopt them given lack of access to computers, high costs, barriers in trust, digital literacy, and knowhow. In sum, the team realized that the original Organizame solution was not suited to the needs of shopkeepers who are accustomed to using a notebook.

Organizame’s interest to meet the needs of informal microentrepreneurs and Banigualdad’s commitment to helping their clients run their businesses more effectively, brought these two organizations together for this partnership.

During the customer research phase, the organizations found the target segment not only needed a tool to help them reconcile their finances at the end of the month, but also needed support in analyzing and developing new business opportunities, setting and sticking to goals, and keeping their family and business expenses separate.

The Solution

The Banigualdad and Organizame teams saw an opportunity to influence the record-keeping behavior of informal microentrepreneurs by helping them to separate family and business expenses, understand the importance of tracking income and expenses, calculate their business results, and monitor their accounts receivable.

Accion worked with Organizame to tailor their online business management tool to better serve Banigualdad’s informal, low-income clients. The app influences the user’s financial capabilities through several means:

- An app-based tool that enables MSMEs to digitize their business operations. While most microentrepreneurs in Chile do not have a computer, they have smartphones that they actively use for personal purposes, and to reach their customers and suppliers. Organizame, Banigualdad, and Accion decided to leverage that existing usage to develop a mobile application that would enable MSMEs to track their sales and expenses, and even issue electronic invoices — a first step to business formalization. The app consolidates their business transactions and automatically calculates monthly profits.

- In-app notifications that provide reminders and advice to ensure the tool is being used effectively. The app sends notifications and reminders to users at least once a week to remind them to keep track of their business transaction data in the app. In addition, the app monitors any inputted accounts receivable, and sends the user notifications when they come due. The app also sends reminders with key pieces of advice, such as keeping your family and business accounts separate.

- Gamified tutorials that make learning how to record transactions digitally engaging and fun. Research has shown that simply educating entrepreneurs about the benefits of digital tracking is not effective in changing their behavior, but gamification of experiences can be more effective. The project team developed a gamified tutorial for microentrepreneurs to play within the application to encourage and incentivize them to register their daily sales and expenses in the platform. Immediately after downloading the application, users are introduced to a game that simulates a small fictional business. The user earns points as they complete tasks that help them learn how to use the app, like tracking the fictional business’ income and expenses. As users gain points, they can improve the virtual business. The game walks users through how to log sales by customer and how to keep track of what they owe their suppliers or what is owed to them.

Results

The Organizame app was launched in April 2021 and five months after launch, it has been downloaded 1,660 times and 543 users have completed the gamified tutorials. To measure the impact of the tool on overall well-being of the users, we surveyed a sub-segment of clients prior to the launch of the tool, and again three months later to assess their overall feelings of well-being, ability to manage their business, and ability to manage debt.

Among the 554 merchants that responded to the survey, 44 percent downloaded the application and among those who have the application, 33 percent have begun registering their sales into the platform. The following findings compare the financial well-being of those that have downloaded and are using the application with those who have not downloaded the application. The second group does not serve as a perfect control group because the team targeted more mature businesses to pilot app, suggesting that impact may be overestimated.

Customer Spotlight: Rosita Corrotea

Rosita Corrotea is an entrepreneur from Coquimbo city in northern Chile who sells homemade cakes for birthdays and events. Her business is informal and she has been a Banigualdad client for almost four years. She knows how her business is going by the number of orders she receives but, before using the Organizame app, she didn’t really know how much money she earned per month. With the app, she can keep track of what she sells and what she spends on her business, and can calculate profits at the end of the month. Rosita has always been a person who likes to learn new things and found that using Organizame was very easy. She followed the tutorials and says that, “the application itself teaches her how to use it, it is easy to follow the instructions.”

Overall well-being

Results of the survey show that overall feelings of well-being improved for both those that used the Organizame app, as well as those who did not, which may reflect that microentrepreneurs across Chile are slowly beginning to recover from the ravages of the pandemic. However, users of the platform reported a 17 percentage point increase in their satisfaction with their financial situation, while those that did not use the platform only reported a 5 percentage point increase.

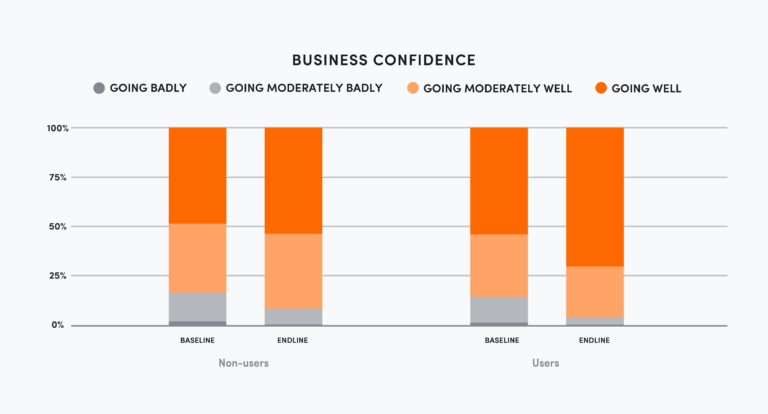

Business management

Across all measures, users of the app noted an improved ability to manage their business when compared with those that did not use the application. Prior to use of the app, approximately 50 percent of merchants reported feeling their businesses were progressing well. Among those who used the app, that group grew by 16 percent whereas it stayed around 50 percent among those who didn’t access the app, suggested that those who used the app were more likely to report positive feelings about their businesses.

All businesses reported being better able to pay themselves a salary at the end of every month, but the change was greatest among those who registered for the app as compared with those who never registered for the app. Similarly, the number of merchants who reported that their businesses grew in the last year increased in all groups. But while that proportion only grew by 5 percent in the non-app group, it grew by 13 percent among merchants who used the Organizame app.

Finally, users of the app were also less likely to confuse their personal and business funds. While the group without the app reported a 3 percent decline in ‘mixing their business and personal expenses’ (perhaps an effect of the assessment process), the group using the application reported a 12 percent decline, suggesting the effectiveness of the application in helping people track their business and personal funds separately but also a slight overall trend in better organization of funds across both the control and user group.

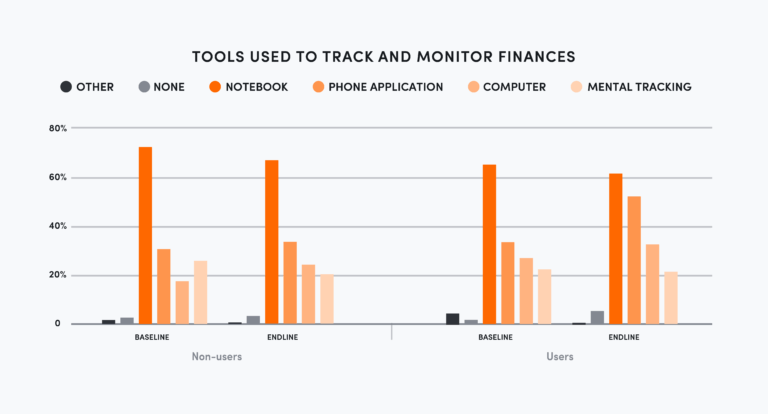

Budget management

The primary objective of the Organizame application was to change microentrepreneur’s business record-keeping behaviors to help them better manage and grow their businesses. Results from the survey found that even for those using the application actively, a notebook continues to be the primary tool for monitoring and tracking daily income and expenses. However, both groups did report an increase in their use of digital tools when managing their businesses — likely a result of changing digital behaviors during the pandemic. Not surprisingly, those that started using the app to monitor their finances reported a 24 percentage-point increase in their use of applications and computers when monitoring their expenses. The group without the app saw a 15 percent increase in the use of applications and computers. It will be critical for the Organizame team to continue

to find ways to motivate and incentivize users to continue recording their transactions digitally, as lasting behavior change takes time.

Savings and long-term planning

Usage of the Organizame application is also correlated with greater resilience. The proportion of users of the app who reported that they could survive less than three weeks with their current savings decreased by 17 percent over the treatment period. In contrast, that proportion stayed more stable among those who didn’t use the app.

Overall, Organizame’s app seems to help microentrepreneurs gain greater control over their expenses and even helps them to prepare for months of low sales — a critically important task for them to stay resilient in uncertain times. The Organizame solution provides low-income entrepreneurs with better insights into their finances, organizes their operations, and helps them make more informed decisions to grow their businesses and re-invest in their households.

While the app has had some preliminary benefits, there is still room for improvement. Usage data shows that only 28 percent of users are inputting their sales into the app regularly (seven times a month or more). Others are consolidating their daily sales and inputting their expenses into the app at various points within the month. The notebook continues to be the most prevalent method of record keeping. Through user research, we found that it is onerous for microentrepreneurs to record every single transaction separately in a digital app, as they may sell a high volume of low-price items each day, which are easier to note down in a notebook and transfer to the digital app in batches a few times each month.

Key takeaways

The market for financial health advice and support is vast. There are billions of people who are financially coping or vulnerable globally, and many need help. Organizations that support microentrepreneurs know this and realize that if they can help people overcome their financial challenges, they will win their loyalty. Visa recently approached Organizame to form a partnership and will be offering this platform to the low-income small business segment across a number of financial service providers, as a free value-add service. In the next year, the partnership is expected to reach 300,000 clients.

Human touch is critical for delivering digital financial tools to low-income consumers and businesses. This is especially true among low-income people who are accustomed to working with trusted intermediaries like bank officers and require more support navigating digital tools.

Organizame found that adoption and use of the application were dependent on having their representatives walk users through how to download the Organizame application and explain the benefits of the application in simple terms. The team found that downloads of the app spiked only on the days that the loan officers sent a link to the application directly to their group members through WhatsApp.

Managing finances can be stressful and intimidating, but gamification — or the use of game design elements in a non-game context — can make certain tasks more fun and motivating. Research has shown that gamification can influence psychological and physical outcomes.

Organizame applied this principle to its app. In this case, users earn points after completing tutorials instructing users how to record their sales into the application. The team found that the use of these tutorials motivated registered users to create product categories in the app.

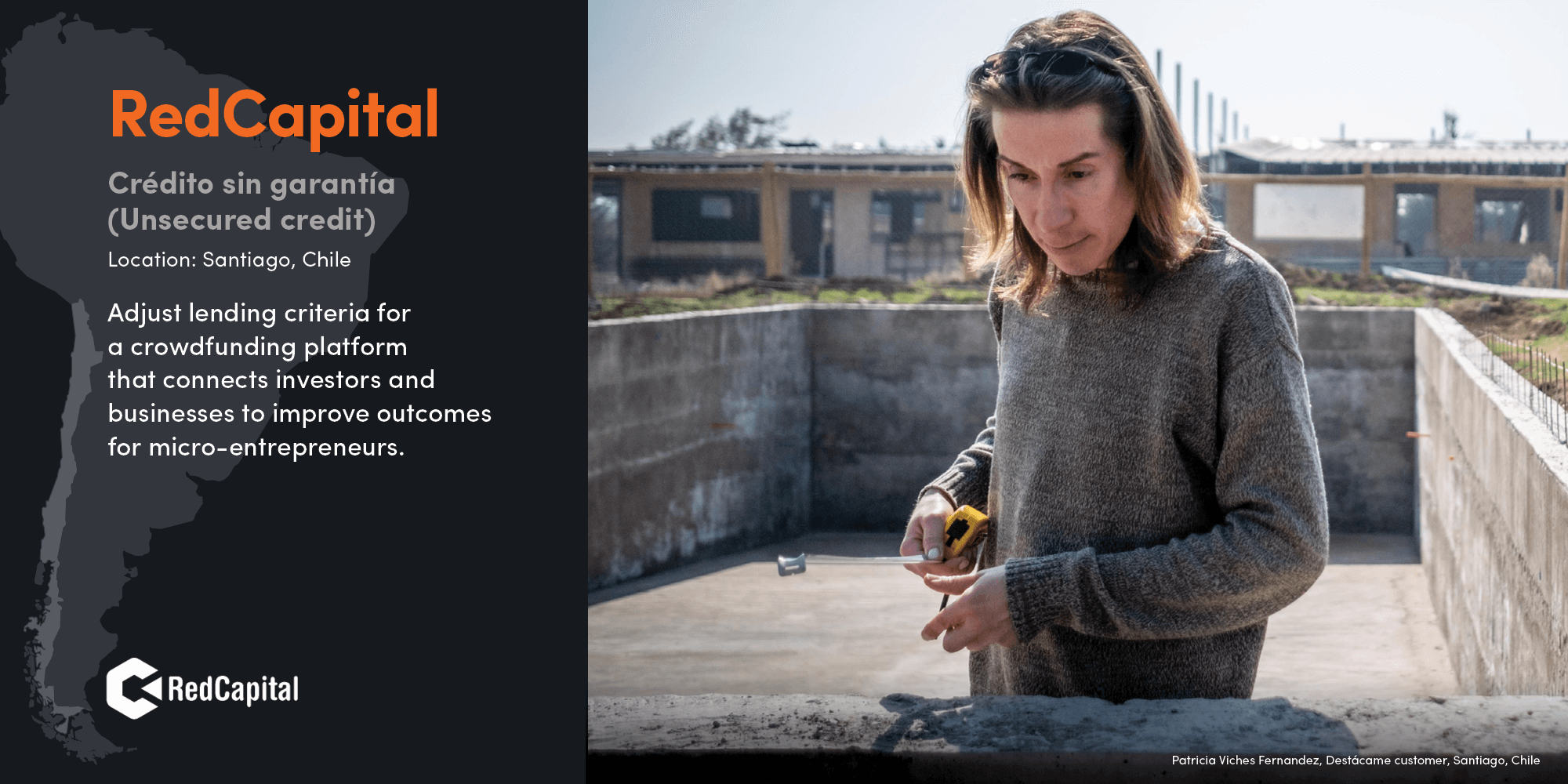

Case Study: RedCapital

Chilean banks and authorities have made critical advances to increase financial inclusion. Between agent networks, payment platforms, and the CuentaRUT account — a simplified deposit account with a debit card that state-owned Banco Estado has made available to anyone with an identity card — Chile has nearly reached universal access to financial services.

Despite the advances, many small merchants in Chile cannot find financial tools to meet their needs. Micro, small, and medium enterprises (MSMEs) make up 98.5 percent of enterprises in the country but almost a quarter face difficulty accessing financing in times of need. This has been especially true since COVID-19 infections soared last year, especially since nearly 30 percent of the population that works in the informal sector has no access to social protection.

RedCapital, a fintech and crowdfunding platform in Chile, was founded in 2014 to help formal small and medium enterprises (SMEs) get the funding they need. On RedCapital’s platform, individual investors lend money or provide factoring for SMEs, giving Chile’s small businesses the financing they need to expand, and investors are provided with attractive returns.

While the platform has served SMEs well, microentrepreneurs, especially informal ones, have been more difficult for RedCapital to serve for several reasons. They tend to prefer informal credit with simpler processes, lack the documentation required by the RedCapital’s original credit scoring system, and are often less comfortable using a digital platform to meet their financial needs. To continue growing the platform and address the credit gap faced by MSMEs in the country, the team needed to find a way to expand down market. By RedCapital’s estimations, there is a projected USD $10 billion market opportunity to be accessed by serving MSMEs that lack access to finance.

RedCapital Client“[The banks] never gave us a loan, one because we were not banked and the other because the interest rate of the banks is very high, but once we met RedCapital and we saw that the interest rates were manageable and that it was not so difficult to apply for a loan, we decided to do it.”

RedCapital and Accion partnered to conduct market research with Chilean microentrepreneurs and found that MSMEs are eager to grow their businesses but need support to understand how to use short-term credit to control their levels of inventory, manage their debt, and to deploy simple strategies for setting and meeting growth goals. Many informal entrepreneurs said they were uncomfortable taking out loans from a digital platform, and preferred to speak with a person when sharing personal information or addressing key questions. These findings made it clear to the team that, in addition to simply redesigning their platform for MSMEs, they would also need to adapt the customer experience to provide microentrepreneurs with a way to grow their businesses and help them to understand and improve their financial health in the process.

The Solution

To create such a product, Accion helped RedCapital completely redesign their platform and digital customer experience to better serve microenterprises. The team adapted the platform’s processes, credit-scoring methodology, pricing, and the customer experience to provide greater transparency and support to microentrepreneurs. And they created a low-cost, easy to access credit product, coupled with business management lessons, to build the financial health of microentrepreneur users of the RedCapital platform.

The lending product was adjusted to better serve microentrepreneurs and support their financial well-being through the following features:

- A credit scoring model more appropriate for the MSME segment. As a fintech, RedCapital’s business model leveraged technology and a proprietary credit scoring system utilizing publicly-available tax and utility data. However, the model excluded MSMEs, which did not meet the credit-underwriting criteria. With this project, the team developed a new scoring model, using Accion’s credit risk methodology, to provide credit to MSMEs that exhibit an entrepreneurial spirit and growth mindset, profit potential, and some level of tech usage.

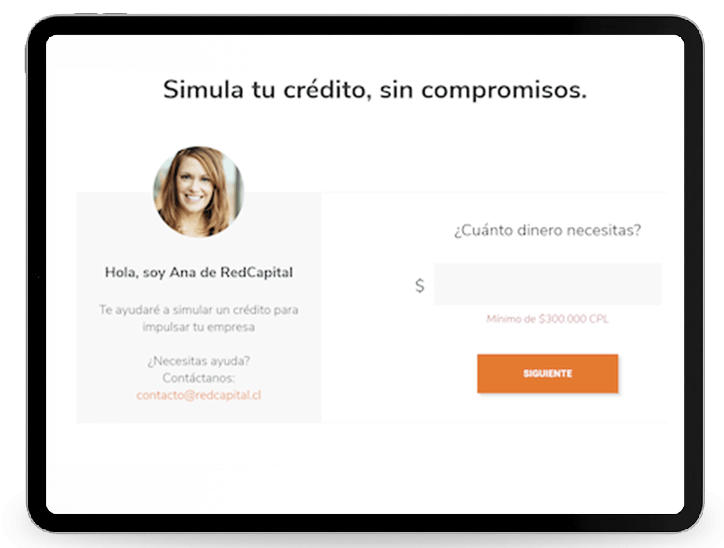

- A chatbot to mimic human interactions. The research found that users were not comfortable inputting their personal information into a website. The team created a chatbot to mimic an interaction that users trusted and felt more comfortable with. Customers can get ongoing support through the intelligent chatbot at every step of the journey — and there is also the option to connect to customer service if additional hand holding is required, balancing tech and touch in the digital journey.

- Financial-health focused exercises that help MSMEs grow their businesses. To address the key pain points that MSMEs face in growing their businesses, the team created video and blog content to help their customers spend, save, borrow, and plan better by: (1) organizing their finances, (2) controlling costs, (3) planning for their future, and (4) managing debt. The content was designed to help entrepreneurs gain skills as their businesses became more established.