Authors

- Priya Punatar

- Amy Stewart

geography

Topics

- Challenges and Crises

- Customer Centricity

- Digital Financial Services

- Enabling Environment

- Financial Capability

- Financial Health

- Fintech

- Human Centered Design

- Resilience

- Responsible Digital Finance

- Responsible Product Design and Delivery

- Small Business Owners

- Underserved Groups

Partner

The financial services landscape is crowded with a wide array of offerings, but vulnerable and low-income people across the globe still struggle to find products that are designed to meet their needs. This gap has been amplified though the economic fallout from COVID-19, which has disproportionately affected those without the access, resources, or network to weather the storm. Now more than ever, low-income populations need customized and responsive financial products and services to recover from the crisis and restart in the new normal.

To address this gap, in recent years many financial service providers have turned to human-centered design (HCD) methodologies to better understand their clients’ wants, needs and aspirations, hoping to update their product offering and drive usage. While many organizations have this goal, very few have been able to deliver on it. Many human-centered products are based on thoughtfully designed and innovative ideas, but ultimately do not end up gaining traction with customers or are disbanded when institutional priorities shift. Sometimes institutions focus on customer needs but overlook real operational and business constraints. Others design from the board room, without taking into account the customer’s life and the complexities around financial decision making and end up solving for the wrong problem. To be sustainable, innovative digital products must balance the customer’s needs with organizational capacity and should be built upon a solid business case to ensure that the product is supported in the long term.

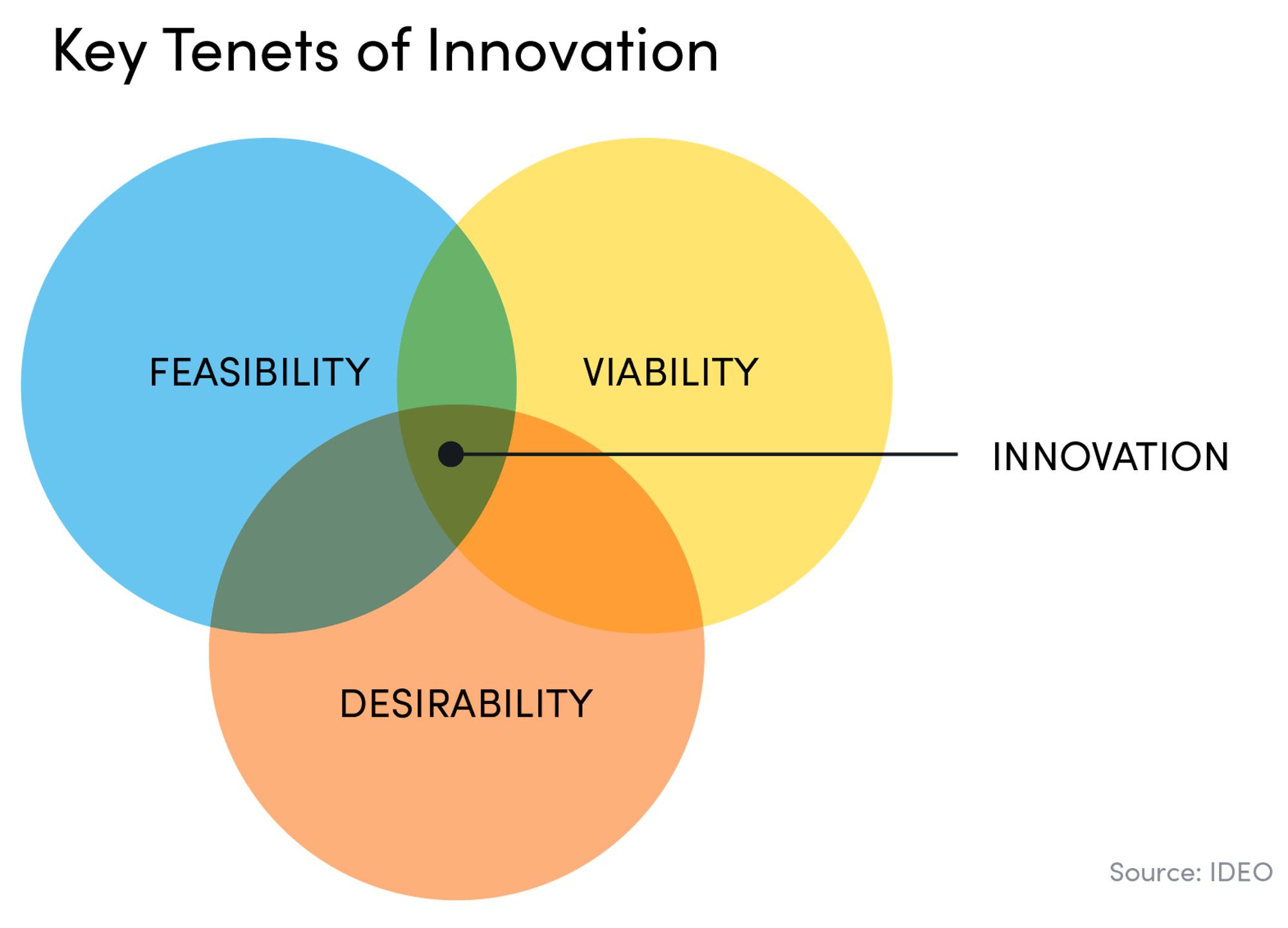

Accion, in partnership with MetLife Foundation, is committed to delivering high quality, affordable solutions for the billions of individuals who are still underserved by the financial sector. We do this by working alongside financial institutions to design, build, launch and optimize innovative products, services, and experiences for low-income customers that are desirable (wanted by and useful for clients), feasible (achievable given the institution’s operations, technology and resources), and viable (make business sense)—so that the products make it from concept to commerce.

This paper outlines how financial institutions can develop innovative and sustainable financial solutions. It draws on our recent experiences working with financial services providers and fintechs in Chile and Mexico over the last two years to design and launch behaviorally-informed products that build customers’ financial capabilities and ultimately improve their financial health. While the products were not specifically designed to respond to the impacts of COVID-19, they aim to build resiliency to financial shocks and enable users to pursue opportunities over time.

This paper will cover how we leverage human-centered design and a strong focus on behavior to create more desirable products, how we evaluate institutional capacity to ensure feasibility, and how we get the business model and KPIs right to ensure the product is viable and justifiable for the business for the long term—even during economic shocks. For customers, this approach translates to more intuitive financial products and services that are aligned with their behaviors and help build their financial health. For financial service providers, this approach leads to innovative products that are sustainable, use internal resources efficiently, and achieve business goals.

Using this approach in Chile, we developed a business management application with Organizame and Banigualdad, a financial health portal with Destácame, and a crowd-funding platform for microentrepreneurs with RedCapital. In Mexico, we developed a savings product for youth with Caja Popular Cerano, and a supply chain finance product with Caja Bienestar.

Desirability — are we solving customer problems?

To combat the persistent issue of dormant accounts, financial service providers must design desirable products that people will want to use, that are intuitive, and that will generate value. Desirable products solve customer problems, and to identify the right problem, institutions need to go to the customer. HCD methodologies stress talking to and observing potential customers to gain perspective and empathy for their lives. We’ve found it just as important to analyze how customers make decisions — both consciously and subconsciously — and how they behave, using qualitative and quantitative data.

How can we ensure products are desirable?

Conduct client-centric user research that seeks to understand customer behavior

We begin every design process by conducting user research to understand what customers want and why they act the way they do. Interviewers are trained to take note of physical and emotional reactions, feelings, and expressions as well as customer surroundings, observing their daily lives and understanding their broader context.

While social distancing measures make in-person interviews difficult, we found that this can also be done remotely. In Mexico, the team conducted remote video interviews with youth customers, and found that they were still able to capture non-verbal cues and build trust. Questions explore underlying attitudes that inform client decision-making. We listen closely to understand when participant behavior may have been affected by emotion, stress, or biases. This process helps us to ensure that we are building products that accommodate client realities, will align with how customers actually behave, and will make their lives easier.

After conducting user research, interviewers document observations, facts, quotes, and impressions shared by customers. As the information grows, key themes, patterns, and relationships start to emerge. We learned that people often feel stressed and alone in managing their finances and financial challenges, and that microentrepreneurs tend to keep track of their finances mentally. These insights highlight the drivers of customer behavior and were used to guide the product concepts

With Caja Popular Cerano, we conducted a co-creation session with potential users, empowering them as active participants in the design process. Typically, co-creation works the best when you have a very narrow problem you are trying to solve. In this instance we worked with small groups of youth to explore how financial service providers could build better trust relationships with young customers. Through co-creation sessions, participants discussed how trust emerges from healthy relationships, and developed a marketing campaign with the hashtag #FinancialLoveExists.

Test products with customers in the field to see how they really react

Speaking with customers will only get you so far in developing a sustainable product. Institutions should quickly move to translate insights into prototypes, giving form to product ideas so that they can move out of the office and into the reality of customers’ lives. Initial prototypes should be “quick and dirty,” allowing teams to explore and get feedback on many options before investing in detailed design and development. Prototyping is an opportunity to gather customer feedback and to assess their behavior. Beyond asking for reactions, likes, and dislikes, we also ask customers to share how, when, and where they would use the prototyped product.

As opposed to early prototypes, which are usually drawn or presented on paper, later-stage ‘usability’ prototypes are close to final fidelity and allow customers to interact with and explore the product flows. Ideally, these prototypes are hosted on the final technology platform and can be tested in a user’s environment. Interviewers simply provide the customer with the prototype and see how they interact – this helps the team get a sense of whether the product is intuitive, how long it takes to complete certain tasks, and what additional features might be required.

For example, microentrepreneurs reviewing the Organizame mobile application told us that when inputting the price of their products into the application, it would be useful to have the option to choose whether that particular product is sold with VAT (value added tax) or not. The development team is now working to build out this option.

Financial institutions should seek to go to market quickly with a minimum viable product and plan for ongoing improvements, as they will likely receive the most relevant feedback after launch.

While prototyping provides important inputs to the design process, it is difficult to fully simulate how the customer will actually interact with the final product. Customers that sit and look at an application for an hour with an interviewer may only have 5 minutes during their daily lives, with constant interruptions, connectivity challenges, and competing demands for their time. Financial institutions should seek to go to market quickly with a minimum viable product and plan for ongoing improvements, as they will likely receive the most relevant feedback after launch. A strong MVP will have integrated feedback from process, technology and price point testing.

Leverage data insights to capture customer feedback and optimize your product over time

The best product designs often evolve over time based on user feedback and behavior. We help our partners build processes and tools that help them to easily assess customer usage, capture feedback, and continually refine and optimize their products.

Once the product is live in the market, it is important to monitor how it is performing relative to key performance indicators, which may include usage rates, transaction volumes, or renewal rates. Customer feedback data and transactional data from the products should be analyzed regularly to capture the customer experience. How long is it taking them to complete a certain task? Are they using features as we expected? How do they feel about the product?

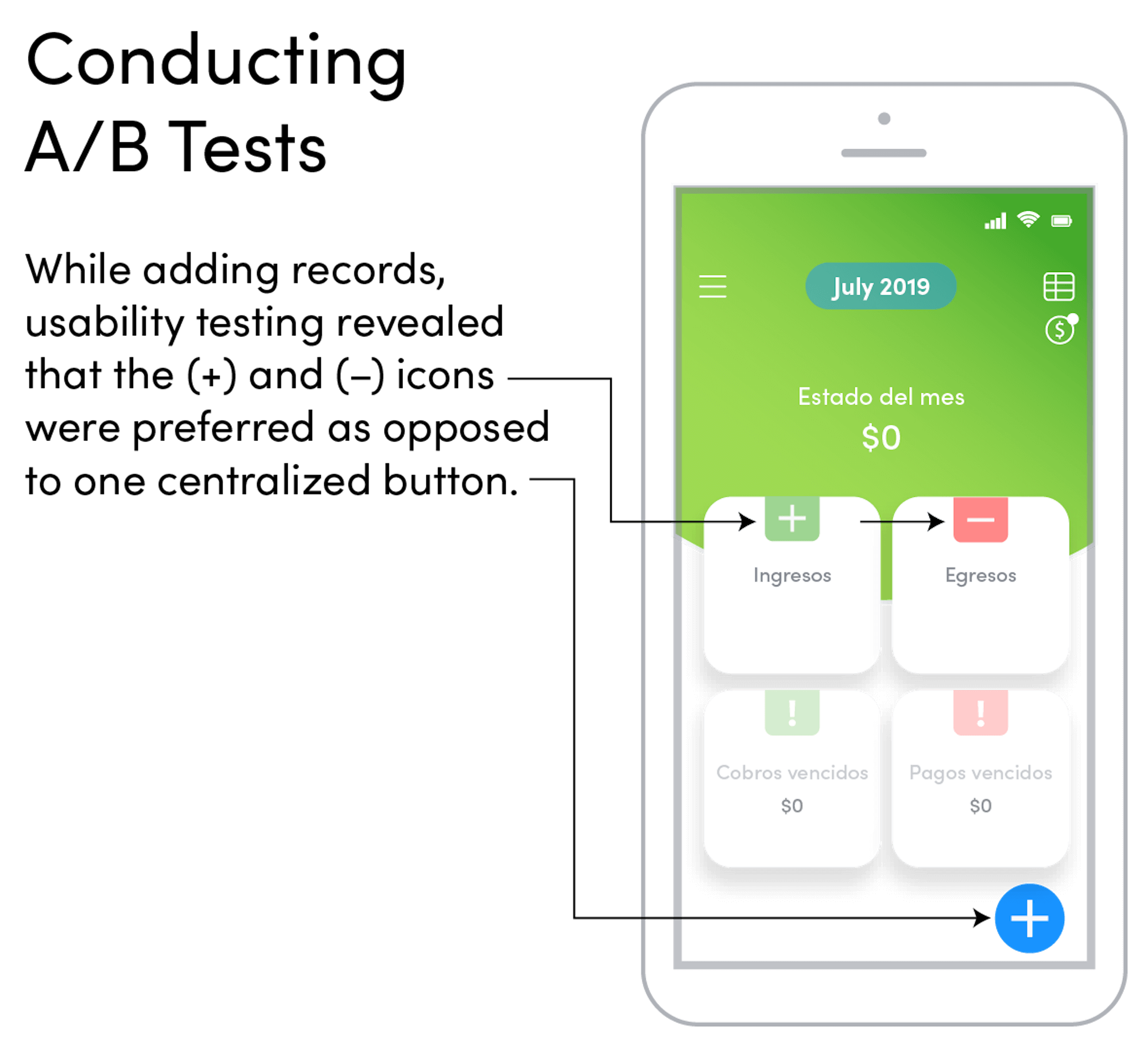

Institutions should make sure that they have systems in place to capture and use the right data to improve and refine processes and products. Organizame is using A/B testing to try out different visual layouts, images and text and see what resonates with the end customer. This provides them with a low-cost channel to quickly iterate and test new features.

Conducting A/B tests

At Destácame, a small, interdisciplinary team was established with representatives from design, user experience (UX), data, and development. The team met weekly to review indicators and user feedback, discuss implications and design changes, and agree on implementation plans. This included diving deeper into the data to better understand where and why users drop out of the customer journey. Based on initial user activity, the team is already working on a batch of design improvements to increase usage and conversion. For example, data showed that users were less likely to complete the budgeting tool if they received a ‘bad’ score on their budget diagnostic. The team hypothesized that the red, unhappy face and language accompanying the diagnosis design was discouraging users who tested poorly. They are now testing different designs and new motivational language to support users in completing the tool: ‘Don’t worry! We will work together to reduce your expenses so you can reach the end of the month.’

Common challenges:

- Organizations may have long-standing assumptions about their customers: Field staff and other customer-facing employees sometimes feel that customer interviews are not necessary, as they already know the customer well. However, these assumptions are often challenged through in-person conversations with customers. For example, at one institution, the field staff felt certain that their clients would want to learn about and apply for a loan through a mobile application. But after conducting a series of interviews, they learned that their clients perceived desktop computers to be more secure for conducting research and inputting their personal information.

- Interviewees might tell researchers what they want to hear. In general, people want to be agreeable. For example, customers will often say “yes” when asked if they would use a new digital tool to register their income and expenses every day, even if they use no other digital tools. Researchers should take results with a grain of salt, and look to cross-reference responses with other information provided (for example, if the user notes they dislike noting expenses in general, don’t frequently have their phone on them, etc.)

Feasibility — are we working within our operational strengths?

While critical to ensuring we are addressing customer pain points, focusing on desirability isn’t enough. Many innovative products that customers say they want or will use have ultimately failed or been discontinued after pilot. Ensuring that our product concepts are feasible requires moving the discussion from the customer to the institution, and is critical for sustainable innovation.

To assess feasibility, one must consider the institutional capacity and operating model, the external environment, and the value proposition of the product for the company. When we think about feasibility, we examine how the new product will leverage existing people, processes and systems, and quantify the gaps that will need to be filled for short- and long-term success. Innovative products often require new skills, updated technology or new partnerships — but feasible products never require a full-blown overhaul of the institution. If a new solution can leverage approximately 80 percent of the current operational capabilities, new capabilities can be built to cover the remaining 20 percent.

How can we ensure products are feasible?

Ensure strategic buy-in early on

Most critical to any successful project is ensuring that the initiative has buy-in from all stakeholders, including leadership, and is aligned with the organization’s strategy. A cross-functional project team is key to ensure that ideas resonate across the organization and that they are feasible for all areas of the business.

When working with early-stage companies, it is important to keep in mind that their priorities and plans may change. It may be that the company is still refining its value proposition or pivots its business model to take advantage of a new partnership or opportunity. To mitigate risk to the product development process and sustainability of the product, we communicated frequently with the institution’s leadership to have full visibility into any competing priorities or challenges that may arise. With one institution, our team met regularly with a board member to ensure that we understood the vision and interests of the board.

Assess operational and technological capabilities from the start — and plan to address gaps

At the outset of the project, we worked with our partners to assess their operational capabilities and take stock of their strengths, weaknesses, and gaps. This included assessing people (skills, capacity and commitment), processes (including data, products and channels), systems (including core infrastructure and enterprise architecture), as well as existing partnerships. We then considered requirements to successfully design, launch and maintain the new product, and created a plan to fill any gaps.

At one institution, the targeting of a new, more informal micro, small, and medium enterprises (MSME) segment required an updated credit risk methodology — for which the team did not have the expertise or data capabilities. Accion worked with the institution to develop a new scorecard using bureau records, an evaluation of the microentrepreneur, and the characteristics of their business, and we worked with the team to automate this underwriting process. Across all institutions, we brought in consultants and new staff to support effective product development, including UX designers, technology developers, and interaction designers. We made efforts to build lasting capacity in the institution, and ensure consultants were mentoring the local team and upskilling key staff.

Encourage a culture of innovation

The development of sustainable products that are useful to customers requires a culture of innovation within the organization. Teams should be encouraged to try new things, learn, and fail fast if something doesn’t work. Institutions that create pressure to generate revenues quickly incentivize speed rather than sustainability and reduce focus on long-term projects that require the team’s creativity, commitment, and motivation.

Balance blue-sky thinking with practicality

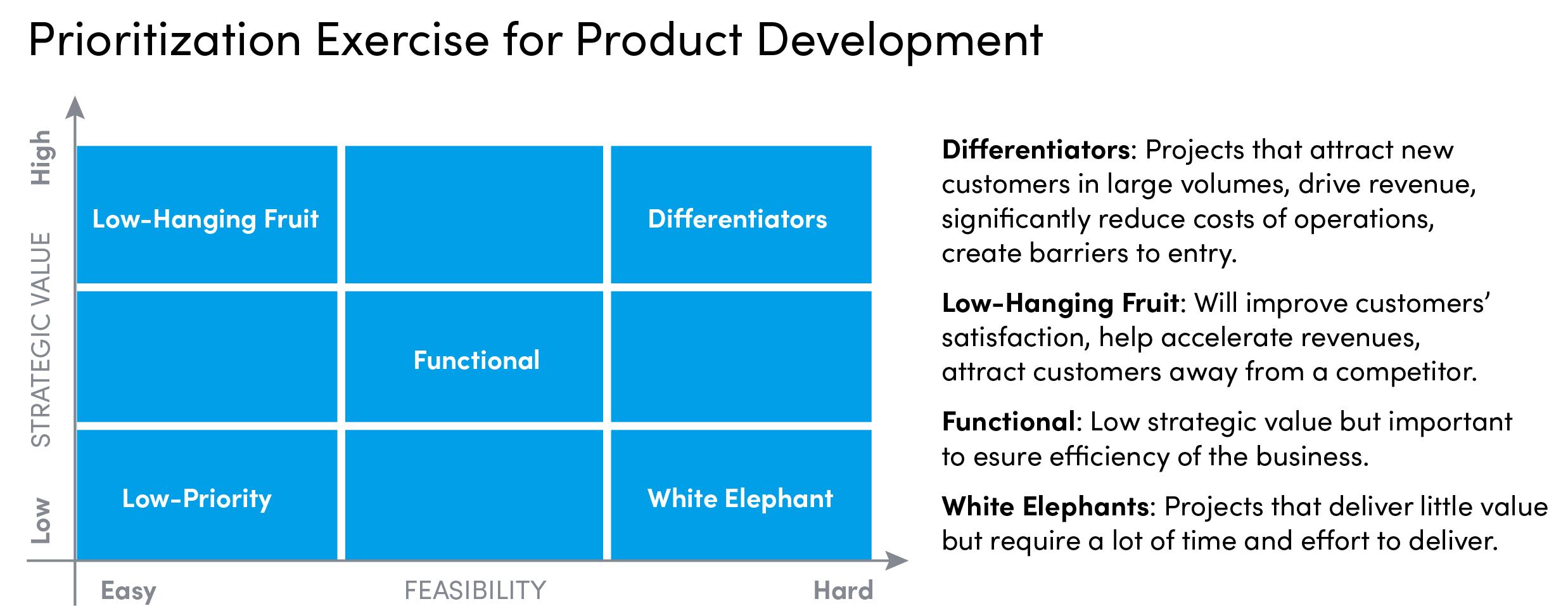

Thinking outside of the box is essential to promoting creativity and driving breakthrough innovation but can sometimes lead to ideas that are not feasible or viable in the long run. To ensure a balance between innovative thinking and feasibility, we prioritized ideas that came out of brainstorming sessions based on several factors: impact on customer financial health, alignment with customer needs, scalability, ease of development, and revenue assumptions. These parameters helped us ensure we were addressing our customer goals and considering key business realities. In some cases, we had to abandon ideas entirely — such as a fully automated chatbot at one organization — as the team did not have the data and technical capabilities necessary to support this feature and developing this capability would have been costly and time-consuming. This prioritization exercise helped us determine which product concepts to prototype.

A focus on disruptive innovation ignores an important reality — it is not always feasible to develop something that has never been done before. We work with our partner organizations to build on their operational strengths and focus on incremental innovation, which may be achieved by targeting a new market or improving an existing product.

Common challenges:

- Existing large-scale initiatives can derail product development efforts. For example, one partner was in the midst of updating its core banking system, a process that has a huge impact on organizational resources. To mitigate the impact on the new product, we worked to anticipate possible risks and assess the feasibility of developing a new product under these conditions. The key factor was generating team commitment. The new product was included within the strategic priorities of the institution, and a multidisciplinary design team, which includes members from different areas of the organization (commercial, risk, strategic planning, etc.) was developed to carry the project forward.

- Customers may not have the tools you are building for. It is important to remember to design for tools you know the target customer already has or is likely to have in the near future. For example, it is not useful to design a mobile application if few of your customers have access to a smart phone. Nor is it useful to design an application for the latest operating system if the majority of people in the market only have access to the previous operating system.

Viability — does the business model contribute to long-term growth?

The last pillar in developing sustainable products is ensuring that they are viable — that the business model is aligned with how customers will use the product, that customers are willing to pay for it, and that the idea ultimately has revenue potential. Viability is key to assuring the product’s sustainability and long-term success. It is not enough to create a product that customers love — it must support business growth and the bottom line.

How can we ensure products are viable?

Assess the market opportunity

At the start of the project, after conducting customer research to define the potential target segment, each of our partners evaluated competitors in the space and conducted an exercise to size their potential market. This helped to ensure that we were developing a solution that will be useful to the greatest number of users. For example, Caja Popular Cerano knew that they wanted to develop a product to better engage their youth customers and that few other cooperatives in Mexico were doing this. A study conducted by the association of cooperatives in the region showed Cerano that the total serviceable market in Mexico is just over 150,000 individuals between the ages 18 to 25 — a significant and relatively untapped market opportunity.

Develop a business case

Once the product concept is developed, we work with teams to build a business case — identifying the potential customer segment, what they need, where they are, and their demand for the product. The business case should forecast user growth and revenue for at least five years, identify the expected break-even point, and be very clear about what assumptions are considered. The business case ensures that the project is aligned with the organization’s strategy and priorities and helps build buy-in throughout the organization. The document should be continually adjusted as circumstances change. Both COVID-19 and political disruptions in Chile have forced us to adjust the business cases to new realities — in some cases lowering projections of number of new users and credit disbursements.

Documenting the business case is critical to getting the business model right and to making strategic decisions. It helps to inform pricing, select the most effective acquisition channel, and predict the contribution of the product to the institution’s bottom line. It is also used to ensure that funds are used effectively throughout the entire product development and launch process.

Stay grounded in business considerations

At every step in the product development process, we worked with our partners to ensure that collectively we were aligning customer needs with organizational goals. When defining which financial capabilities to focus on for each product, we carefully considered the business’s priorities and objectives. For example, as Red Capital expanded their crowd-funding platform for micro and small businesses, their priority is to build capacities of MSMEs to more effectively manage their debt, better control their business finances, and plan for the future. These financial capabilities will not only help the clients improve their credit scores, have less financial stress, and greater satisfaction with their finances, but they are also aligned with Red Capital’s business model — to enable micro businesses to grow with the company.

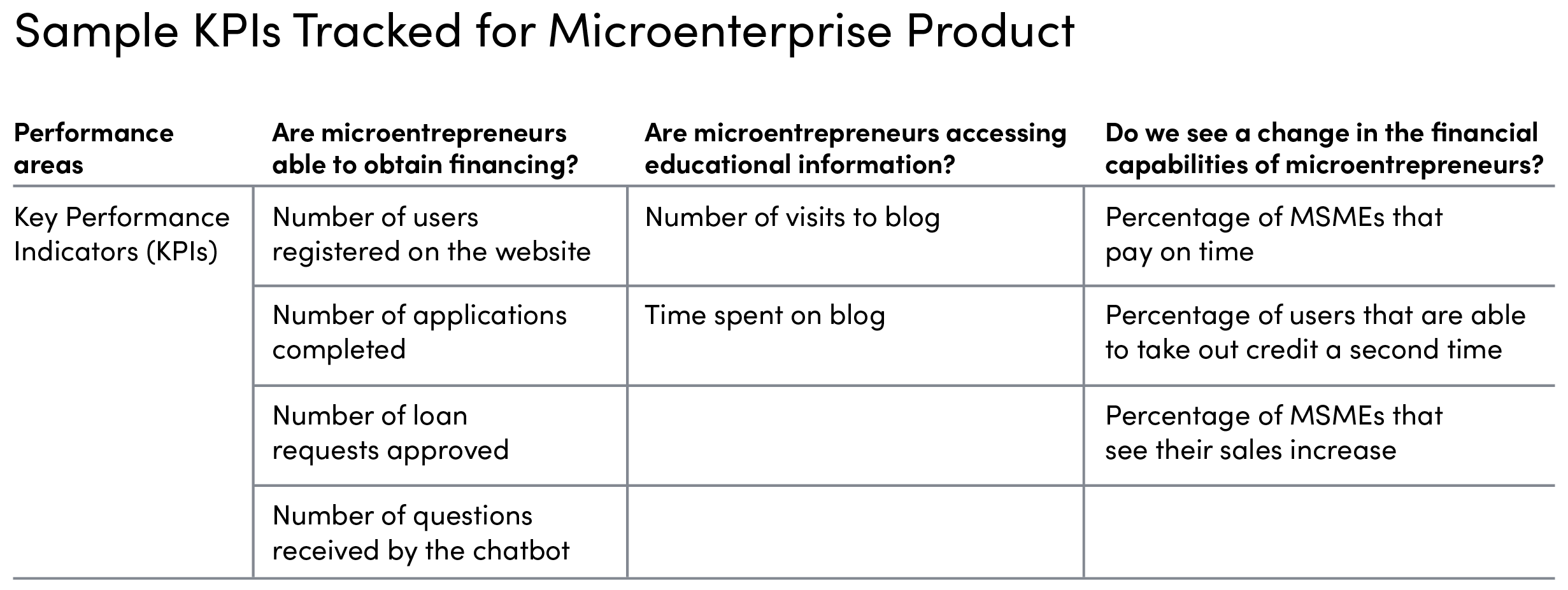

Get the KPIs right

The final key factor to ensuring the viability of the product is to select, monitor, and learn from the right key performance indicators (KPIs). A McKinsey study found that nearly 50 percent of companies do not have an objective way to assess the output of investment that is put into the design of products. We worked with our partners to develop clear KPIs to assess all the intended outcomes of the product — both on the business and on client financial health. How will the product support growth? How will we measure product profitability? How will we know if the client likes the product? How will we know if the client has improved financial health? Many KPIs were interconnected and had to be considered in tandem to assess impact — for example, the percentage of clients that received a motivational message and then chose to make a deposit.

Picking the right KPIs also requires thinking carefully about the measurement strategy and the implications for the institution. Some KPIs were already being monitored by the institution, while others required an additional field in a management information system (MIS) or extra data points from customers. Financial health indicators can be the most complex to measure, as they often require information about the client’s attitudes, knowledge, skills, and behavior, which is typically not captured by the institution. Those with digital platforms can look to identify proxy indicators or incorporate short surveys to assess financial health; others may need to use an additional longitudinal study to properly assess change over time.

Across all projects, we are disseminating short, digital surveys to potential customers before product launch, and to actual customers six months and twelve months after product launch to gauge how the product influences the customer’s financial capabilities and feelings of well-being. Questions are asked in the following areas: 1) Overall well-being, 2) Business management, 3) Budget management, and 4) Impact of COVID-19 on their business and life.

KPIs are only as useful if they are consistently collected, analyzed, and used to drive decisioning.

KPIs are only as useful if they are consistently collected, analyzed, and used to drive decisioning. Institutions should regularly assess progress against KPIs, benchmark with peers, and take action to course correct if necessary. Implementing dashboards can help to visualize trends and insights and determine where to dive deeper into the data.

Common challenges:

- Measuring and tracking financial health is not easy. This typically requires the institution to think creatively about how to capture the knowledge, skills, attitudes, and behaviors of their clients.

- The impact of behavior change on the business case is not always clear. In some cases, a product may require an element of behavior changes from the customer, such as the use of a digital tool for a task they conducted manually in the past. In these situations, the uptake of the product may take longer, and the break-even point may happen later.

- Working uncertainty into a business case is also a challenge. Institutions should keep their business case living and adjust assumptions over time. One institution reacted to the COVID-19 crisis by adjusting assumptions of new credit disbursals to near zero for two to three months to account for the difficulty of acquiring new customers during quarantine. At the same time, they placed more emphasis on promoting the usage of digital tools through the website so they could support customers remotely. The institution will continue to revise assumptions as the current situation continues to unfold.

Bringing it all together

What is desirable isn’t always feasible, and what is viable isn’t always desirable.

Successful and sustainable innovation requires balancing various — and at times conflicting — interests. What is desirable isn’t always feasible, and what is viable isn’t always desirable. To address these dichotomies, and to bridge the tensions that arise along the innovation process, it is important to be intentional in putting into place a way of thinking and working with the team from the outset.

While design thinking and human-centered design methodologies have risen in popularity, few organizations have reported on the role of leadership, the complexity of organizational change processes associated with a design-led innovation approach, the technology needed, and the hard work required by the institution to ensure the product is sustainable. With each of our five partners, we sought to address that gap, marrying the three pillars of desirability, feasibility, and viability to create customer-centric products built on a foundation of long-term success.

For all of our partners, the products developed are closely aligned with their strategic plans. For Caja Bienestar, Red Capital, Organizame and Banigualdad, and Caja Popular Cerano, the institutions were looking to reach new segments and increase their market share. For Destácame, the updated user experience with a value proposition squarely around building financial health, is well-aligned with providing more personalized recommendations for products on the Destácame website.

We will continue to share learnings about ways to align desirability, feasibility, and viability, as well as challenges faced, as we monitor the sustainability of these five products in the market and make continual adjustments to ensure their longevity.

This brief is a part of our Building Financial Capabilities and Strengthening Institutions through Customer-Centered Innovations project, supported by MetLife Foundation