People

- Gayatri Mehta

- Kathleen Yaworsky

Regions

- Bolivia

- Colombia

- East Asia and Pacific

- Ecuador

- Guatemala

- India

- Indonesia

- Latin America and The Caribbean

- Nigeria

- South Asia

- Sub-Saharan Africa

Topics

- Access Usage Gap

- Agricultural and Rural Finance

- Challenges and Crises

- Consumer Protection

- Credit

- Customer Centricity

- Digital Financial Services

- Digital Payments

- Digital Transformation

- Embedded Finance

- Enabling Environment

- Financial Health

- Fintech

- MSME/SME Finance

- Responsible Product Design and Delivery

- Rural Populations

- Small Business Owners

- Smallholder Farmers

- Tech-Touch Balance

- Underserved Groups

- Women

Foreword

Ms. Lilavati Baral, a client of Accion’s partner Annapurna Finance, earns a living as a seamstress in a rural community in Odisha, India. She grew up with limited opportunities and never received a formal education. When she became a teenager, she taught herself how to use a sewing machine so she could begin working as a seamstress. Like many, she did not have the necessary paperwork or collateral to open a bank account at a commercial bank.

When she joined a solidarity microfinance group, Annapurna helped her access a business loan to meet her cash flow needs. As the pandemic negatively affected businesses and national lockdowns prevented people like Lilavati from attending group meetings in person, it became increasingly difficult for businesses and individuals to access finance. This was a major problem, especially when funds were needed to address emergencies. Annapurna was able to offer a near-instant emergency loan, known as a “just in time” (JIT) loan, to its existing 2 million clients, accessible via an SMS or WhatsApp message.

Digitally enabled financial products like the JIT loan can help more micro and small businesses like Lilavati’s build resilience in unpredictable times by expanding access to tools like credit, payments, insurance, and business management advice.

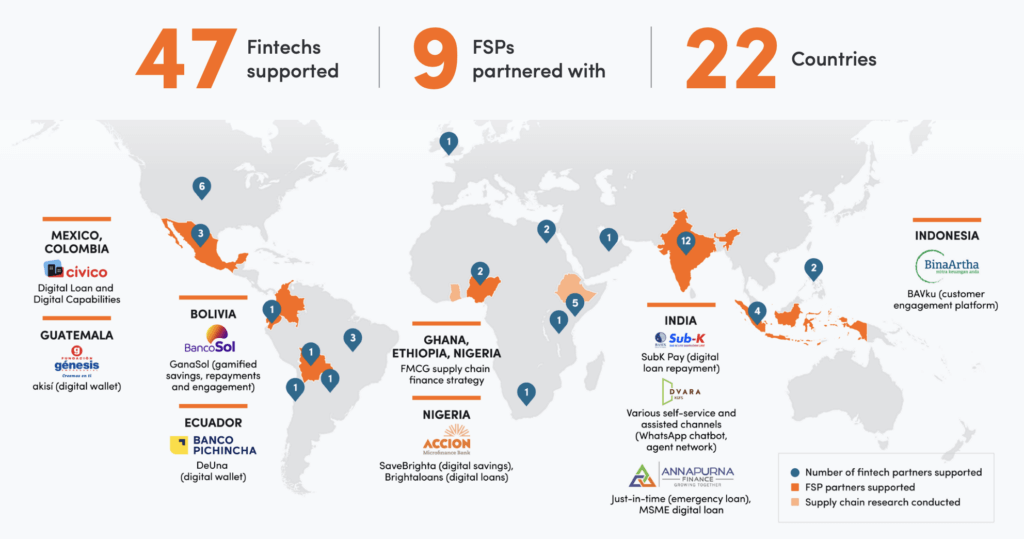

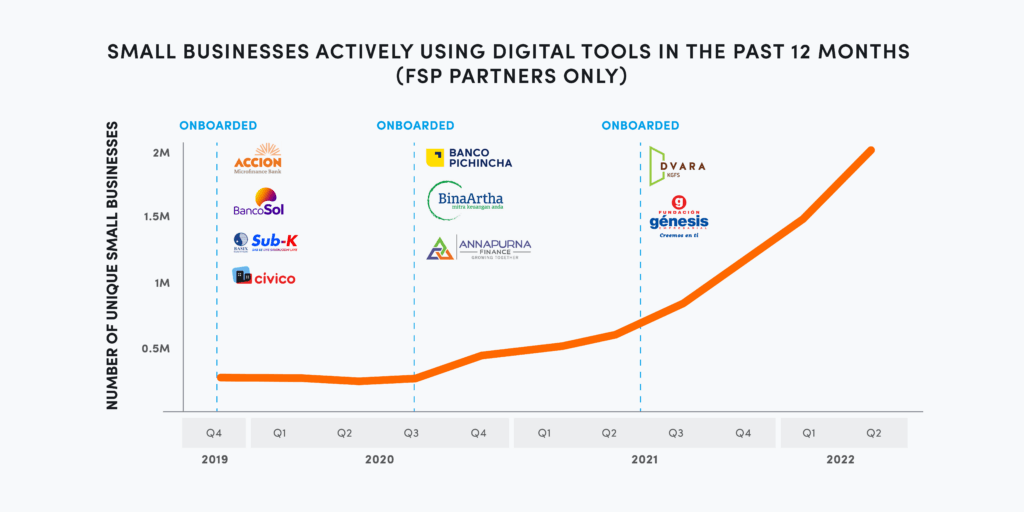

In November 2018, the Mastercard Impact Fund and Accion launched the MSE accelerator program (MAP) to support millions of underserved micro and small businesses around the world by digitally transforming their financial service providers (FSPs). The four-year program has sought to use digitalization and technology to enable better socioeconomic outcomes for micro and small businesses, including increased business growth and financial health. We have worked with a cohort of 47 fintechs and nine FSPs across Asia, Latin America, and Africa — helping them design innovative digital products, financial services, digital tools, and infrastructure to better serve the needs of 11.5 million micro and small businesses and individuals in the digital economy.

On average, our partners in this program more than quadrupled their number of monthly active digital users since joining the program. In many cases, growth in digital usage increased at a faster rate than growth in overall portfolio size, which indicating a significant portion of digital uptake is being driven by the digital transformation of existing customers. This growth is also accelerating, as unique monthly digital users across our FSP partners have increased more in the first 6 months of 2022 than in all of 2021.

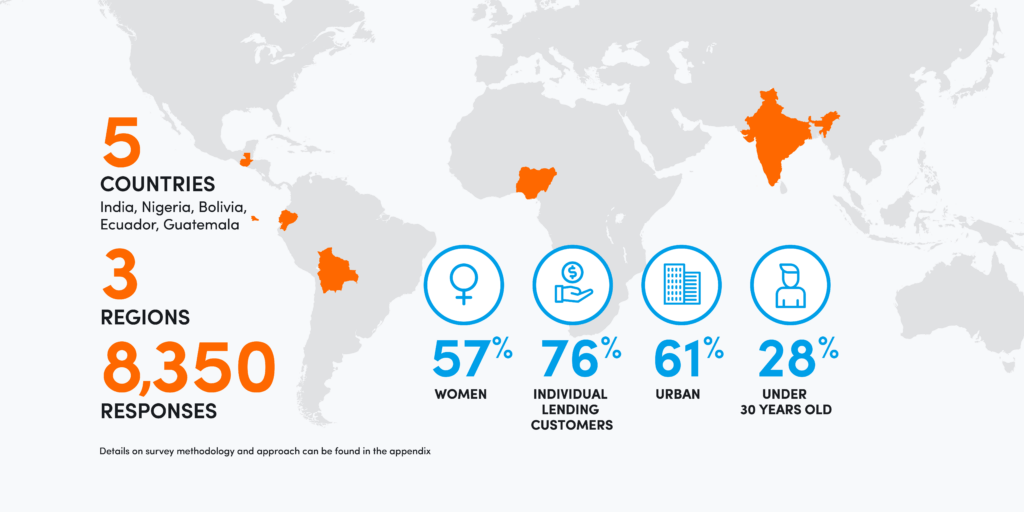

From the program’s results, it’s clear that digitalization benefits FSPs and improves their processes, products, and programs. But at the start of this program, we were eager to understand if and how the digitalization of FSPs benefits their end users, micro and small businesses. How has digital usage improved the lives of microbusiness owners, their businesses, and their financial health? To answer these questions, we conducted a 12-month longitudinal study with a final sample of 2,179 micro and small business customers, from six of the nine program FSP partners across five countries, and surveyed both digital product users and non-digital product users within the program. Our research and findings aim to grow the body of existing industry knowledge with insights that explore what it takes to drive the transformation of micro and small businesses to help inform future digitalization initiatives.

Overall, we have seen that digital product users have reported both business growth and financial health improvements since the start of the program. We hope these findings serve to inspire others and establish some potential models for replication.

We are thankful for the partnerships we have forged during this program and hope these insights will lead to further digitalization programs that improve the lives of millions of individuals and small businesses around the world.

Prateek Shrivastava

Vice President, Digital, Accion Global Advisory Solutions

Payal Dalal

Senior Vice President, Social Impact, International Markets, Mastercard Center for Inclusive Growth

Executive summary

In November 2018, Mastercard Center for Inclusive Growth and Accion launched a first-of-its-kind partnership, with the aim of digitally transforming the lives of 10 million underserved people, of which 4 million micro and small businesses and individuals would regularly use digital tools and services. The program included several components: the digital transformation of micro and small business-focused FSPs in emerging markets, support to fintechs globally serving micro and small businesses, COVID-19 support to small businesses in the U.S., and research on the impact of COVID-19 on micro and small businesses. This has been the largest project undertaken in the more than 60-year history of Accion and was the Center’s largest partnership at the time.

- Accion’s work supported the digital transformation of nine FSPs across Asia, Latin America, and Africa — helping them design innovation hubs, digital lending and payments products, JIT loans, and digital tools, as well as building resilient digital infrastructure to better serve the needs of small businesses and individuals in the digital economy.

- Accion Venture Lab supported 47 fintechs with strategic and operational advice including product design, customer segmentation, process definition, partnership negotiation, board definition, and employee retention strategies.

- Responding to the pandemic, the Center for Financial Inclusion (CFI) housed at Accion undertook a longitudinal, six-wave research study (from June 2020 to October 2021) of the impact of COVID-19 on the lives of micro and small business owners (including partnership and non-partnership customers), along with the policy and investor responses to the pandemic. Roughly one year later (from Q3 2021 to Q3 2022), Accion Global Advisory Solutions conducted another longitudinal study focused on understanding the extent to which micro and small businesses using digital tools created or supported by the program saw an increase in their financial health and business growth.

- Accion Opportunity Fund (AOF) and Mastercard have provided working capital and resources to small business owners in the United States to help them recover from the pandemic. Over AOF’s history, more than 90 percent of AOF’s loans have gone to entrepreneurs who are Black, Latinx, low and moderate income, and The program has looked to scale AOF’s services nationally, use alternative data to improve credit decisioning, and strengthen digital channels and outreach.

The digital and organizational transformation work done under the partnership across its nine FSP and 47 fintech partners exceeded original targets and has reached more than 11.5 million people, with more than 4.4 million micro and small businesses served by providers within the program using digital tools on a regular basis.

In the 12 months prior to Q2 2022, the number of active digital users (one year active) has increased by more than 1.1 million across all program partners, including 800,000 in the last six months alone. Across our FSP partners, nearly 50 percent of digital users are active on a monthly basis. FSPs are seeing financial benefits from this increased digitalization, such as cost savings, operational efficiencies, and enhanced customer experience, thereby building support for the business case for digital transformation.

Beyond driving institutional-level benefits and increased adoption over the past four years, we wanted to know: Has the digitization of FSPs really helped micro and small businesses? What has been the effect of digital usage on the lives of microbusiness owners, and the impact on their businesses and financial health?

As of Q2 2022, on average, our partners more than quadrupled their number of monthly active digital users since joining the program.

When FSPs and fintechs take an intentional approach to designing digital products and supporting processes to serve the needs of micro and small businesses, there is potential for greater uptake and usage. CFI’s research reveals that digital adoption is not an easy or automatic process for small businesses, finding, for example, that usage of mobile money and ecommerce platforms decreased after an initial spike early in the pandemic. Additionally, over time, many micro and small businesses reverted to their old ways of doing business once restrictions on movement were lifted. Yet with the support Accion provided to FSPs and in turn to their customers, program product users demonstrated high levels of adoption and usage. This paper summarizes the results of the second longitudinal study completed by Accion Global Advisory Solutions, as noted above, of the impact of digital tools created or supported under the partnership on micro and small businesses. This study was conducted between Q3 2021 and Q3 2022. Findings show that nearly 80 percent of product users interviewed across five countries perceived an increase in their capacity to manage financial challenges, such as repaying their loans on time or accessing credit for their needs, to products produced by the partnership. Globally, women-owned micro and small businesses also reported significant improvements in their financial health over a 12-month period, with more than 70 percent reporting that the MAP digital products contributed to this improvement. The early stages of the program recorded digital uptake primarily amongst the male customers of FSP partners, but by Q2 2022, more than 70 percent of active digital users were women. While we cannot link all these changes to only the partnership’s programming, overall, we are encouraged to see MAP digital product users reporting improved business growth and financial health outcomes since the start of the program.

This paper presents our key learnings from speaking to customers, contextualized by details from our advisory support at each program partner. It also identifies areas where more research and work are needed. A further survey will be conducted in early 2023, as the final chapter of this longitudinal study, and we will publish an updated set of findings.

Six key learnings

By enabling entrepreneurs and the FSPs that serve them, the program has worked to globally advance financial inclusion and inclusive growth. There are six key learnings that have emerged from our research that highlight the potential of similar programs in driving economic prosperity amongst micro and small businesses. The below findings are derived from our micro and small business digital product user sample population across six of the nine program FSP partners:

- Using digital products can build financial health: across five countries, nearly 80 percent of MAP digital product users reported that product usage contributed to an increase in their capacity to manage financial health challenges.

- Digital products can empower women: globally, women-owned micro and small businesses that were MAP digital product users reported improvements in their financial health in the past year, and more than 70 percent reported that the products contributed to these improvements.

- Digital products can unlock growth: thirty percent of micro and small businesses said they were able to undertake more business growth activities, and 61 percent said this growth came through usage of MAP products.

- Frequent users can see more business value: those who used MAP digital products more frequently were 30 percent more likely than infrequent users to link improvements in business growth outcomes to these products.

- Digital payments are in demand: as micro and small businesses interacted with digital loan repayment mechanisms introduced through the partnership, 67 percent indicated broader demand for digital payments.

- Human touch is still needed: despite an increase in digital usage, fear and distrust of information found online is still high amongst micro and small business owners, highlighting that a certain level of human touch remains important.

Initial findings from our research indicate a positive relationship between usage of digital products and services and improvements in socioeconomic outcomes for micro and small businesses. These early trends strengthen the case for FSPs and the wider industry to invest in well-designed digital products and services for micro and small businesses, especially those that are women-owned.

Despite these successes and promising trends, digital transformation is and must be a continuous journey. We are already drawing upon our lessons learned and looking at wider industry trends to identify how we can continue to work with providers to support the digitalization of micro and small businesses and ensure no one is left behind.

Introduction

As the digital economy has grown in the new millennium, the proliferation of personal devices and available data networks has created an opportunity to enhance the value and accessibility of digitally enabled products and services to drive financial inclusion. Despite the development and availability of many different digital financial products on the market, uptake and usage among micro and small businesses and low-income individuals remained low.

Mastercard and Accion launched this partnership in 2018 as a direct response to the increased availability of data, connectivity, and personal devices, and to address the low uptake and usage of digital financial products among micro and small businesses and low-income individuals, and, ultimately, to improve the resilience and growth of micro and small businesses.

The COVID-19 pandemic, which triggered national lockdowns across the globe, accelerated the need among FSPs for digital tools to enable remote mechanisms to serve consumers, and required additional creativity and innovation to navigate the needs of vulnerable, resource-tight populations. Throughout the program, we witnessed these trends affect our FSP partners and increase their need to find digital ways to reach and interact with their customers efficiently and at scale. To adapt to the changing environment, FSPs needed to leverage customer data for more efficient credit management and product design, build a more flexible organizational structure, and upgrade their core systems. This required FSPs to coordinate across every aspect of their business to find digital ways of serving customers to compensate for the gaps and inefficiencies of manual processes.

Despite the many challenges faced by micro and small businesses throughout the pandemic, one silver lining is that the initial shock jump-started digital adoption globally, born out of necessity and sustained — at least initially — by an increased awareness of the benefits of digitalization. As countries began to shut down, businesses large and small needed to find ways to continue operating, often turning to online mechanisms to market their products, interact with their customers, negotiate with their suppliers, make payments, and transact remotely. According to the OECD, up to 70 percent of micro and small businesses increased their use of digital technologies during the COVID-19 pandemic. The latest Global Findex found that nearly 40 percent of adults in emerging economies (not including China) made their first merchant payment using their phones, the internet, or a card since the pandemic began.

Longitudinal research of micro and small businesses from around the world by CFI found that these businesses did not consistently use digital tools throughout the pandemic to continue operations during lockdowns, increase sales, and reach new customers. To understand the effect of the pandemic on the businesses and households of small business owners in emerging economies, CFI conducted six surveys of 1,600 micro and small business owners in four countries — Colombia, India, Indonesia, and Nigeria — between June 2020 and October 2021. It also conducted focus groups with 130 micro and small business owners in March and April 2022.

The report detailed the devastating initial blow and the long, ongoing process of recovery. The CFI study also found that usage of mobile money and ecommerce platforms decreased after an initial spike early in the pandemic. Over time, many micro and small businesses reverted to their old ways of doing business once restrictions on movement were lifted. This was especially true for women-owned businesses.

CFI’s research reveals that digital adoption is not an easy or automatic process for these businesses. Yet with the support Accion provided to FSPs and their customers, MAP product users demonstrated high levels of adoption and usage.

When FSPs and fintechs take an intentional approach to designing digital products and supporting processes to serve the needs of micro and small businesses, there is potential for greater uptake and usage. Accion’s study on the digital financial products and services created or supported under the partnership, conducted between Q3 2021 and Q3 2022, offers initial evidence that increased access and sustained usage of digital products can lead to better and more inclusive economic outcomes for micro and small businesses, helping reduce the gender gap and digital divide by particularly benefitting women.

Under the partnership, Accion Global Advisory Solutions has helped financial service providers design innovation hubs, digital lending products, emergency loans with rapid turnaround over digital channels, and customer engagement solutions. To support our partners through their digital transformation, we have assessed their digital readiness, guided change management initiatives, implemented enterprise-grade data platforms, built mobile-based applications, and revamped branchless banking channels, among other things. Accion Venture Lab investments have focused on next-generation micro and small business finance, more responsible approaches to consumer finance, insurance products, and agri- fintech. CFI has conducted in-depth and quantitative research to understand the impact of COVID-19 on the financial health and resilience of micro and small businesses. This partnership helped FSPs see that digital transformation is not about technology, but change management of their people, and the resulting impact is clear.

As the program nears completion in Dec 2022, it has improved the lives of more than 11.5 million individuals, including more than 4.4 million micro and small business owners, by helping them to operate in, and benefit from, the digital economy. Beyond these figures, we are particularly excited about the spike in 30-day usage, with more than 1 million micro and small businesses using MAP products at least once a month as of Q2 2022, a number that has doubled in the last 12 months. This uptake is evidence of the importance and value of these tools.

The results of the partnership support the hypothesis that digitalizing small businesses and the financial service providers that serve them will lead to better products, services, and channels that will enable small businesses to fully participate in the evolving economy and drive greater financial inclusion. This paper demonstrates the value and impact that this program and digital transformation have had on our FSP partners and their micro and small business customers. We hope our findings will help catalyze strategic investments in the digital transformation of inclusive financial providers and their underserved customers.

Results

Context and overview

Beyond driving institutional-level benefits and increased adoption over the past four years, we wanted to know, how has digitalization of FSPs specifically affected the quality of life, financial health, and business growth of micro and small businesses and their owners? To achieve this, we conducted longitudinal client surveys starting in Q3 of 2021 (the “baseline”) and again in Q3 of 2022 (the “endline”). A third survey round is planned for Q1 2023. The final endline sample comprised 2,179 micro and small business customers of six MAP FSP partners across five countries. The survey sample included approximately 25 percent of micro and small businesses that had used MAP digital products at least once in the previous 12 months, versus 75 percent that were customers of the FSP partners but had not yet used these products.

The aim of this research was to enable customers of FSPs to share, from their own perspective, what changes, if any, they experienced during the survey period with respect to financial health challenges, business growth opportunities, and access and usage of digital financial services (DFS) — and whether MAP products had played a role in these changes.

It is critical to note that survey respondents’ perceptions of the impact of digital tools on their financial lives should be understood and interpreted within the broader context (or constraints) at the community and country level. There may be other factors, such as the existence or lack of government programs (subsidies, cash transfer programs, etc.), changes in political and macro-economic stability (debt moratoriums, elections, etc.), and varying social norms (behavioral and cultural differences, etc.), that could affect the sample population surveyed. Furthermore, a micro or small business’s ability to access and use digital financial solutions will also be affected by their overall financial resources and human capital, among other factors. Collectively, these factors contribute to the business’s ability to increase financial health and resilience and capture opportunities for business growth, which are the two primary levers contributing to the ultimate outcome we hope to see, which is improved well-being.

This is all to say that the pathways to positive socioeconomic outcomes for end customers are lengthy and complex, with many interrelated factors contributing to micro and small business owners’ lived experience — and it is difficult, if not impossible, to disentangle these pathways to definitively prove any straight-line path of causation. This study is not a randomized control trial and does not suggest causation in any of its findings. It does, however, provide a rigorous analysis and robust findings on the relationship observed between MAP digital product usage and financial health and business growth outcomes reported by product users.

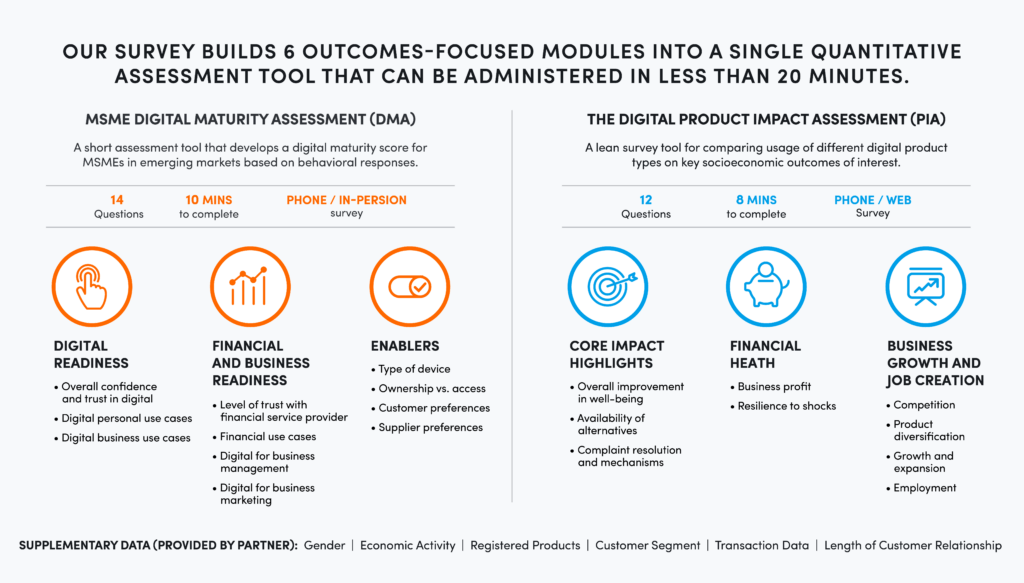

More details on the survey design and methodology can be found in Appendix B, but it is important to spend a moment here on definitions, to contextualize the survey findings.

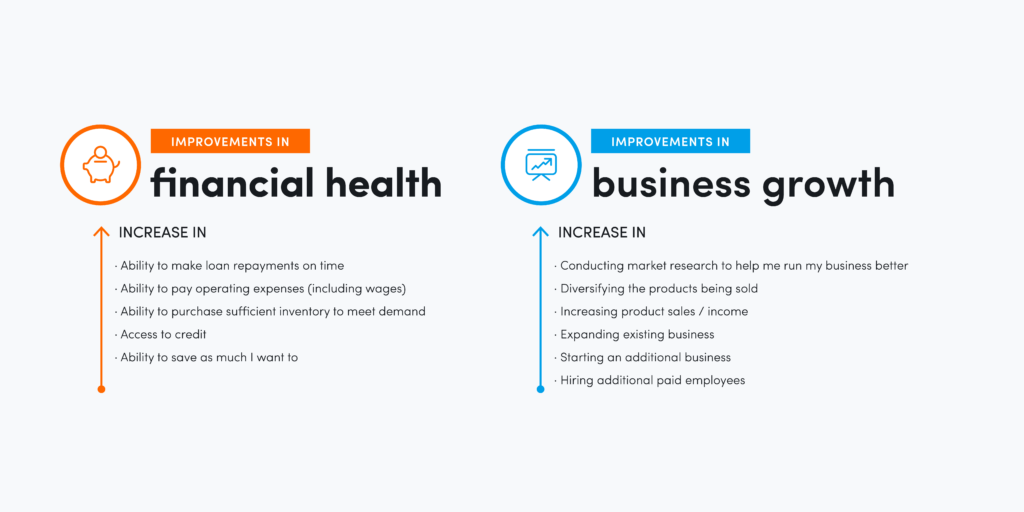

For the purposes of our survey, we define “improvements in financial health” and “improvements in business growth,” respectively, as an increase in at least one of the outcomes listed in the chart below.

Six key learnings

As we are seeing digital maturity and usage increase across the globe, micro and small businesses surveyed from Q3 2021 to Q3 2022 have reported that the digital products developed and enhanced through the partnership contributed to several improvements in their business growth and financial health. These benefits are especially salient for women-owned businesses, as well as for people who used MAP products on a frequent basis. Across the board, most product users reported they perceive these products as relatively better than available alternatives in their respective markets.

We distilled the following six key learnings from analysis of survey data. Additionally, in the case studies that follow each learning below, we provide specific examples of some of the main drivers of success that may contribute to these results, in terms of what each program partner FSP did and what influenced their ability to transform, especially with respect to strategies and best practices on digital customer relationship management, organizational change management, and governance.

1. Using digital products can build financial health

Businesses surveyed reported that using MAP digital products contributed to improvements in their financial health.

Digital products developed under the partnership included credit, payments, savings, and gamification (Appendix C details the products supported or launched under the program and their relevant impact indicators). The program saw success in driving increased usage of these digital products, as well as early evidence that product usage is correlated with improvements in financial health.

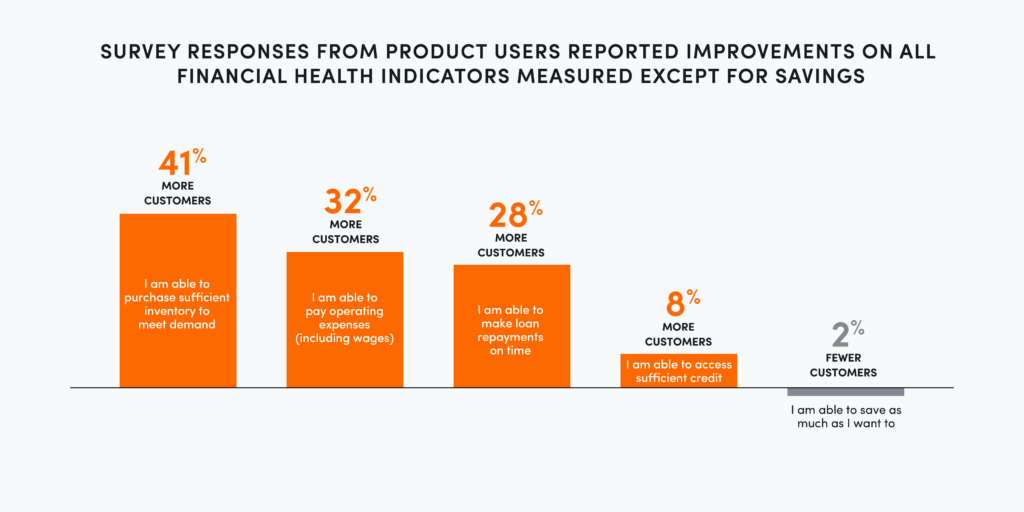

Product users reported improvements on all financial health indicators measured except for savings. From baseline to endline:

- 41 percent more customers were able to purchase sufficient inventory to meet

- 32 percent more customers were able to pay operating expenses (including wages).

- 29 percent more customers were able to make loan repayments on

- 8 percent more customers were able to access sufficient

- 2 percent fewer customers were able to save as much as they wanted

Globally, nearly 80 percent of users agreed that MAP products contributed to the improved financial health outcomes they reported experiencing.

Emergency digital loan users reported particularly strong financial health improvements; more than 90 percent said they could pay off business expenses, and 85 percent reported being able to buy sufficient inventory to meet demand.

For a gamified digital repayment channel launched in Bolivia, we saw a 30 percent increase in users who reported being able to repay their loans on time. During COVID-19, managing portfolio at risk (PAR) became a priority and challenge for many FSPs. As a response to the pandemic, we adapted the gamification scheme of a digital savings product to also enable rewarding on-time and digital repayments. Pivoting in this way helped the institution keep PAR in check, and lowered costs by encouraging digital repayment. Furthermore, nearly 90 percent of micro and small business owners who adopted this product said it helped them save time since they no longer had to visit a branch.

As we saw from CFI’s research, even by September 2021, 28 percent of micro and small businesses reported being unable to cover business expenses with revenue. Against that backdrop of slow global recovery for these businesses, the financial health improvements reported by product users are encouraging and speak to the important role digital financial tools can play in building resilience to and recovery from shocks such as the pandemic.

Partner Spotlight: Accion Microfinance Bank

Established in 2006, Accion Microfinance Bank (Accion MfB) is one of Nigeria’s most successful microfinance institutions (MFIs). This MFI seeks to make digital operations the new norm at the institution and encourage digital behaviors in their customer base. We partnered with the institution to build a digital bank within the MFI to scale SaveBrighta, a digitally enabled savings product, and develop BrightaLoan, an end-to-end digital credit product, a first for the institution. Under the program, Accion also advised the institution on its organizational design, agent network and channel expansion, and omnichannel and cyber-resilience strategies.

Since the start of the program, Accion MfB has more than doubled the number of customers using digital channels on a monthly basis.

After the redesign, we have seen a strong uptake of digital channels including mobile banking apps, feature phone, and third-party national payment channels. Since the start of the program, Accion MfB has more than doubled the number of customers using digital channels on a monthly basis. Furthermore, the value of transactions conducted through digital channels grew from 2.02 billion Naira in 2019 to 20.99 billion Naira in 2021. Eighty percent of SaveBrighta users reported that the product helped resolve financial resilience challenges they had experienced over the previous 12 months, such as not being able to purchase sufficient inventory to meet their demand and not being able to save as much as they would have liked. The number of non-loan related savers grew from 89,289 in 2019 to 184,398 at the end of August 2022, representing a 106% growth. The value of savings also grew by 37%, from 3.4 billion Naira to 4.64 billion Naira in the same period. Additionally, we saw a decrease in the percentage of individuals saying they would prefer to cash out of their digital wallets immediately. Even though the product produced under the partnership is not a digital wallet, this suggests increased confidence in digital store of value.

Taiwo Joda, Managing Director and CEO, Accion MfBWe saw the need to create a new digital department to fast-track the delivery of products and to have a team that will focus on our digital propositions. Our digital services empower people who run businesses in Nigeria because they provide convenience, allow for innovations in their businesses, and increase their efficiency and productivity.

2. Digital products can empower women

Women who owned micro and small businesses that participated in the program reported significant improvements in their financial health in the past year, with more than 70 percent reporting these improvements came through their use of MAP digital products.

CFI’s research shows that women faced higher rates of business closures and lower profit levels, and were less likely to cover business expenses with revenue than their male counterparts during the global pandemic. Eighty percent of surveyed businesses owned by men reported improving profit trends in Q3 2021, compared to 67 percent for women-owned businesses.

Digital uptake was slow, sporadic, and even declined among women micro and small business owners in CFI’s survey, pointing to the likelihood that the women-owned firms were not benefitting from the digital economy as much as their male counterparts. Women-owned micro and small businesses were less likely to use formal financial services or transact by mobile phone.

Accion’s second study, conducted with customers of program partners approximately one year after CFI’s longitudinal research, brought a refreshed outlook on women’s ability to adopt and benefit from digital products and services. The majority of the more than 11.5 million clients of our program partners are women. The early stages of the program recorded digital uptake among FSP partners primarily consisting of male users, but by Q2 2022, 75 percent of the 2.25 million active MAP digital product users were women, thus we were able to gather significant data on the impact of the program on women-owned micro and small businesses.

While the number of smartphone owners did not increase tremendously, we observed a notable improvement in digital maturity amongst the segment, indicating that this shift was driven largely by an increase in usage. More women deepened their consumption of digital products and services, and, in parallel, reported benefits in their financial health. Compared to other products, digital wallets seemed to fare most popularly amongst women micro and small business owners, with more than 80 percent reporting their quality of life had improved because of the wallet. Also, women who were MAP product users were twice as likely as men to make loan repayments on time, pay operating expenses, purchase sufficient inventory, and access credit. Seventy percent of women-owned micro and small business MAP product users reported that these benefits came through their use of MAP products.

These findings are encouraging, but it is important to consider external factors to contextualize and try to understand the stark contrast between how women-owned micro and small businesses generally fared during the pandemic and the experience of women who were MAP digital product users one year later. Women tend to be generally more disadvantaged at the “starting point” in terms of access to financial resources, human capital, and support — and therefore the gains they reported experiencing may be “low-hanging fruit”; in other words, it is easier to experience an improvement from a relatively lower starting point. Another interrelated factor may be the relative perception of value; these gains may be comparatively more important to and valued by women, given the deeper systemic challenges they face.

Opportunity for future research

These learnings and results from the partnership have highlighted the challenges facing, and solutions benefitting, women-owned micro and small businesses. Ultimately, more research is needed to better understand the role of appropriate and responsible DFS provided in conjunction with improvements to financial capability in potentially contributing to closing the gender gap and digital divide in financial inclusion. Furthermore, these findings suggest a clear business case to FSPs for serving women-owned businesses with appropriate and responsible DFS, to acquire and retain a highly active and loyal customer segment.

Partner spotlight: Banco Pichincha

Banco Pichincha has been an Accion partner for more than two decades and is the largest financial institution in Ecuador, with a 115-year history and a deep commitment to its customers.

Accion worked with Banco Pichincha to drive digital adoption by developing a digital payment strategy for the bank and coordinating merchant acceptance and consumer digital payment campaigns specifically to drive uptake of digital payments using the bank’s digital wallet, Billetera DeUna. For example, the “360 campaign” to drive digital adoption succeeded thanks to a dual focus on customers and loan officers — and, critically, did not just incentivize new customer signups, but rather continued digital transactions, especially merchant payments. Additionally, Banco Pichincha ran a localized Facebook campaign for shops, with an incentive scheme for shop owners to accept customer and supplier payments using QR codes.

After 12 months of using DeUna, 80% of women said they feel less overwhelmed in managing their expenses and debt because they could better manage their money.

More than half of Banco Pichincha’s customers are women. After 12 months of using DeUna, 72 percent of women micro and small business owners said their use of the product contributed to improvements in their financial health, and 80 percent said they felt less overwhelmed in managing their expenses and debt because they could better manage their money. This represented a 10 percent increase from the baseline in those feeling less overwhelmed.

Since joining the program, the number of Banco Pichincha customers using digital channels on a monthly basis has increased by more than 80 percent.

Patricia Chávez, Manager of Commercial Alliances, Banco PichinchaFor me, it is personally rewarding seeing that our clients can work with the DeUna wallet, being able to understand their needs, and receiving feedback from our clients with the help of Accion so that we can continue improving the platform, which will become part of a payment ecosystem that we are planning to roll out in the future.

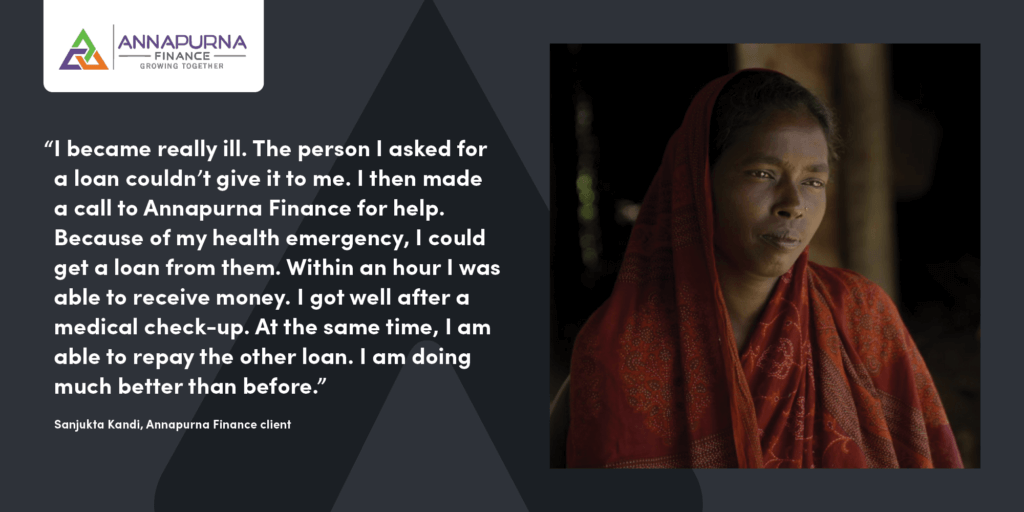

Partner spotlight: Annapurna Finance

Annapurna Finance Pvt. Ltd. (AFPL), established in 2009, has its roots as a part of a not-for-profit entity, working for the development and welfare of unserved sections of India’s society. Over the years, AFPL gradually transformed to become a nonbank financial company (NBFC) and scaled up across the country, while staying true to its mission. Today, AFPL serves more than 2.3 million clients across 21 states with more than 1,000 branches, giving it a truly national footprint.

Since introducing digital products and processes in Q4 2020, uptake among AFPL’s customer base has scaled to more than half a million active monthly users.

AFPL has two distinct verticals: an MFI vertical for serving rural customers, and a vertical for small businesses in the urban and peri-urban geographies. We partnered with AFPL to drive digital transformation through the development of a digitally enabled emergency loan ( JIT loan) and a digital loan for small business clients. Under the program, we have also reimagined the engagement model for group lending, leveraging digital customer engagement tools and digital payments. Since introducing digital products and processes in Q4 2020, uptake among AFPL’s customer base has scaled to more than half a million active monthly users.

At AFPL, women-owned small businesses reported significant improvements in their financial health and resilience over the 12-month survey period from Q3 2021 to Q3 2022, with nearly 60 percent saying these improvements came through the JIT loan. The loan helped alleviate pressures that arose from financial emergencies and more than 90 percent of women who used the product reported they were able to pay operating expenses on time, as compared to 31.5 percent during the baseline survey.

Dibyajyoti Pattanaik, Executive Director, Annapurna FinanceDigital adoption, with the help of technology — it’s a big enabler for us to bring a more efficient solution to the client and envisage our entire digital transformation, from a very heavy physical process to a digital process. Whether it is client onboarding, client sourcing, underwriting, risk management, payment solutions — all our processes.

3. Digital products can unlock growth

In the past year, customers have reported that using MAP products directly improved their ability to undertake more business growth activities and expand their businesses.

During the height of the pandemic, and for many months after, many small business owners struggled to keep their doors open. Those who were doing well prior to the pandemic focused primarily on surviving, while many others were forced to pivot activities or close shop. In Nigeria, for example, we saw a 25 percent decline in MAP digital product users who were able to open or start a new business from Q3 2021 to Q3 2022, while other regions remained mostly stagnant.

However, when we looked closely at many of the other business growth indicators, such as hiring new employees, increasing product sales and incomes, and expanding businesses, we saw a more promising outlook. From Q3 2021 to Q3 2022, MAP digital product users reported a 30 percent increase in business growth activities, and more than 61 percent of these product users linked these improvements at least partially to the digital products used.

Across MAP product users, digital wallet users were most likely to report that their use of the product helped expand their business and increase their income. Digital wallets, as with other digital tools, facilitate increased business velocity — showing micro and small business owners can get more done in less time. More than 75 percent of wallet users said “saving time” was the most important benefit they got from the product. For business owners who are running full-time businesses while managing the household, time is a scarce and valuable resource. Any opportunity for time savings can be reinvested into their business to drive expansion and growth.

Users of a digital repayment application we designed in India were most likely to start an additional business, and credit the product with their ability to do so. Streamlining repayments for small businesses and facilitating access to a diversified suite of credit products are key enablers to business growth activities such as setting up a new business. Given most MAP digital product users linked their successes, at least partially, to their usage of the product, these early trends in business growth indicate that well-designed digital solutions can contribute to supporting micro and small businesses in not just surviving, but also growing post-pandemic. It is important to note, however, that micro and small business owners who are more likely to use these types of digital tools may intrinsically have additional characteristics that may make them more successful business owners. Further research is needed to disentangle the key behavioral drivers that lead to positive business outcomes.

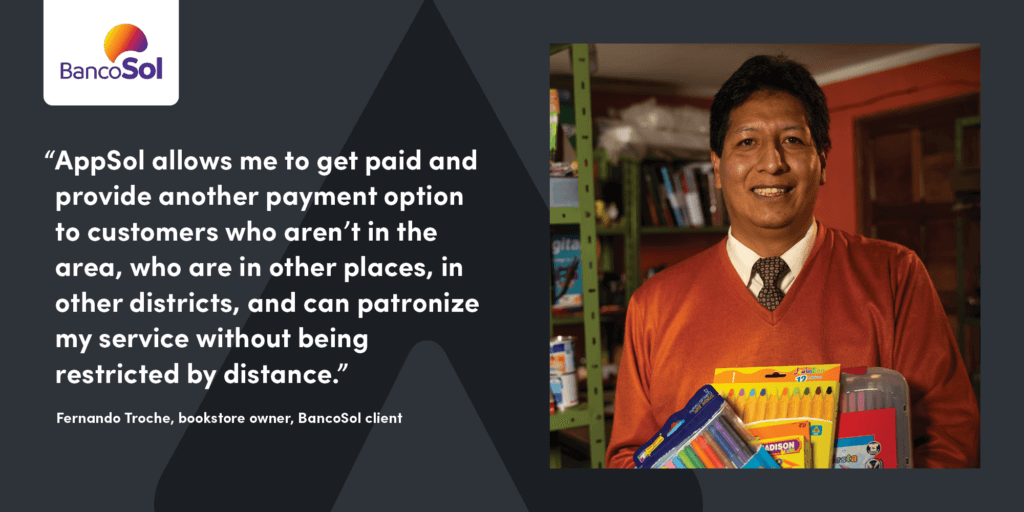

From the FSP’s perspective, beyond seeing improvements in business growth outcomes of their customers, they have also benefitted directly from digital transformation. Digital channels for customer acquisition and servicing are more cost effective and can drive significant efficiencies for FSPs in how they operate. For example, BancoSol reported a reduction in customer acquisition costs by diverting many transactions that previously took place at branches to its mobile banking application. Across the bank, digital transfers, deposits, and payments have increased. More digitally mature customers are twice as likely to receive electronic payments, as well as those who pay for services and/or providers electronically.

Partner spotlight: BancoSol

Established in 1992, BancoSol is the largest MFI in Bolivia, currently serving more than 1.1 million low-income customers. At BancoSol, we designed an innovation hub within the bank to create innovative products and solutions to address the needs of its micro and small business customers in new ways, thereby driving growth of the bank.

GanaSol, a gamification-based platform that was deployed to encourage savings, on-time loan repayments, and use of digital channels, saw 10,000 new users within the first four weeks of launch in April 2021. The first solution was promoting digital savings; however, given that Bolivia experienced the world’s longest nationally mandated moratorium on loan repayments during COVID-19, BancoSol pivoted to leverage GanaSol to promote timely loan repayments. Since the launch of GanaSol, BancoSol has increased its monthly active digital userbase by more than 50 percent.

Several initiatives were launched to increase customer awareness and uptake, including branch champions who executed a campaign to onboard customers to AppSol, BancoSol’s mobile banking app, while they waited in line at branches, as well as the implementation of revised key performance indicators (KPIs) for loan officers. The digital activation campaign at branches served two purposes: relieving bottlenecks at the branch and converting new digital customers.

Ninety percent of GanaSol product users reported the product helped resolve key financial challenges such as not being able to make on-time loan repayments or not saving as much as they would like to, while 65 percent reported use of the product improved their business growth. Furthermore, 78 percent of users reported that GanaSol helped them save time, and 72 percent felt it was better than available alternatives in the market.

The innovation hub has been a success in fostering a culture of innovation across BancoSol. Staff now proactively suggest testing out new ideas, and the bank is leveraging customer data more strategically in support of these initiatives. In 2020, Accion and Mastercard partnered to conduct Bolivia’s first “datathon.” The datathon developed the methodologies and a proof of concept for how BancoSol and other microfinance institutions can take a more data-driven, customer-centric approach to support small businesses’ recovery and resilience, including, for example, analyzing customer banking patterns to help identify customer segments that are most likely to go digital, equipping loan officers with insights to match customers with products that meet their needs, and enabling the bank to reduce attrition by proactively engaging customers before they begin to disengage.

Marcelo Escobar, Co-CEO, BancoSolBancoSol supports our customers with tools and processes beyond digitalization so that they also have an important differential added value. We don’t lose the personal connection that the bank has always had with its clients. We humanize technology to close the digital adoption gap that exists in Bolivia, and in South America as a whole.

4. Frequent users can see more business value

Those who used MAP digital products more frequently were more likely to report that these products contributed to improvements in business growth outcomes.

Increased depth of MAP program product usage was positively correlated with an increase of users reporting that the digital products contributed to business growth opportunities. More active digital product users (as defined by product activity in the last 30 days) were 30 percent more likely to report that MAP products contributed to improvements in business growth, compared to one-time or very infrequent digital product users.

Furthermore, increased usage seems to contribute to a “virtuous cycle” of customer engagement; frequent users were more likely to report that products contributed to business growth, and, in turn, a more favorable perception of the MAP product. Further, initiatives to promote sustained usage of DFS may help FSPs improve customer engagement and loyalty, and perhaps contribute to increased customer lifetime value in the long run. For example, at Annapurna Finance, more digitally mature segments were three times more likely to agree that accepting digital payments would be good for their business. However, more frequent users may also increase their expectations over time, requiring FSPs to “up their game” periodically to continue to meet or exceed customer expectations and maintain market leadership.

These initial trends indicate the importance of and benefit from increased frequency of usage of digital products and services, as increased depth of usage is positively correlated with the value perceived by the end user and therefore supports the business case in driving active usage. While we may expect well-designed products to receive a more favorable review from end users, further research is required to dig deeper and understand what elements of the design drive higher uptake.

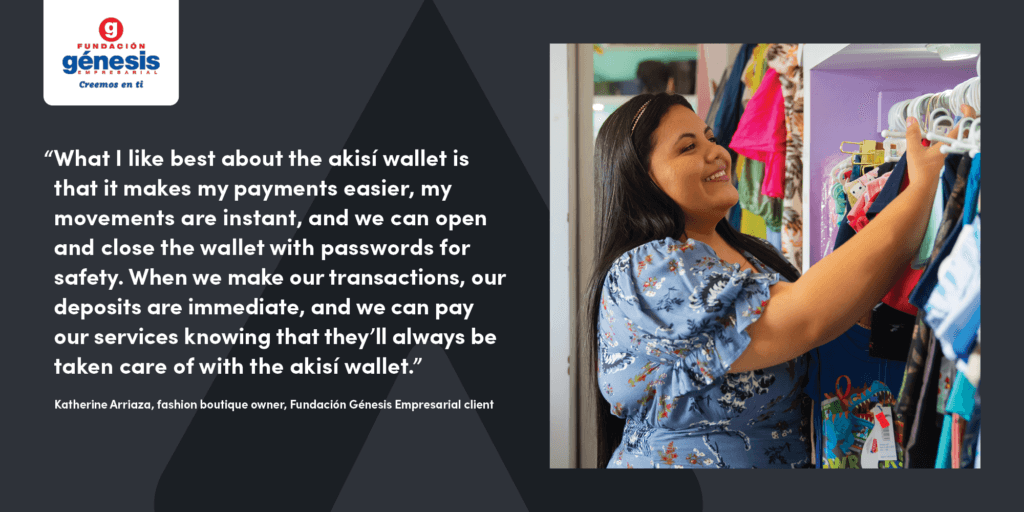

Partner spotlight: Fundación Génesis Empresarial

Founded 34 years ago, Fundación Génesis Empresarial is Guatemala’s largest nonprofit microfinance institution, offering a comprehensive portfolio of products and services that include working capital, housing improvement, education loan products, agricultural financing and advisory, insurance, and remittances to MSMEs and rural communities across the country. Accion partnered with Génesis to scale adoption of its digital wallet and digital credit products in Guatemala, along with expansion of its Pronet agent network across the Northern Triangle.

In the past year, the number of Génesis customers repaying their loans via Pronet agents has increased by nearly a quarter to 84% of the overall customer base. A smaller segment of individuals leverages the akisí digital wallet to make certain transactions, like repayments, airtime top up, or bill payments.

76% of akisí users reported the product helped them undertake more business growth activities.

While the number of akisí users is small, those who have adopted akisí are high frequency users, transacting at least 1-2 times per month on the wallet. Seventy-six percent of these active users attributed the product to helping them undertake more business growth activities.

Critical to continued scale will be Génesis’ ability to shift strategically from seeing akisí as a separate business line to an integrated value offer that reinforces other product lines. Accion’s support has been focused to that end, for example enabling digital loan application and disbursement through akisí.

Edgardo Perez, General Manager, Fundación Génesis EmpresarialWe’ve focused on maintaining a financial and social balance that allows us to elevate our clients’ standard of living. This is done through products and processes focused on their well-being. The akisí wallet saves our clients time with their transactions, payments, transfers, and remittances, so it’s no longer necessary to travel large distances to access these services.

Partner spotlight: Dvara KGFS

Founded in 2008 as a non-banking financial institution in India, Dvara KGFS (Dvara) aims to support their rural customers’ wealth creation and financial well-being by using a combination of traditional physical branches and digital banking to bring credit, savings, and insurance to rural communities in India.

Since launching digital channels in early 2022, uptake has grown to 23,000 monthly active users.

Accion has supported Dvara with developing and implementing a digital omnichannel strategy to boost operational efficiency and drive greater engagement amongst its customers through enhancing the customer experience. Key activities included development and launch of a CRM system, expansion of Dvara’s agent network and WhatsApp conversational platform, and an integration with the Unified Payments Interface (UPI) for digital payments.

With KGFS Pay, customers can repay their loans digitally and use WhatsApp as a primary channel of communication to interact with the institution. Since launching digital channels in early 2022, uptake has grown to 23,000 monthly active users.

Murty LVLN, Managing Director & CEO, Dvara KGFSWe are in a new era of digital-led customer experiences and will keep innovating further given the opportunity in the rural market segments that we operate in. As part of our omnichannel strategy and digital transformation journey, we will continue to balance innovation and growth while delivering value-based products and services for our customers.

5. Digital payments are in demand

Subsequently, a behavior shift strengthened toward broader digital payments acceptance, supported by increased demand globally for digital payments among micro and small businesses since COVID-19.

Across digital maturity segments, there was a modest increase of about 10 percent from baseline to endline in the number of customers who used their phones to make and receive digital payments; however, 67 percent of micro and small businesses reported it would be better for their businesses if they could accept digital payments more widely. This number was 73 percent for MAP product users versus 62 percent for non-MAP product users.

As customers of micro and small businesses are adopting digital channels to buy goods, place orders, make payments, and more, those businesses are starting to appreciate the potential benefits in their own businesses as well, from increased revenue to efficiency, security, and cost savings.

Digital loan repayment mechanisms can be a simple way to start to familiarize micro and small businesses with the value proposition of digital payments, over time opening potential opportunities for FSPs on several fronts, such as increasing functionality of wallet or payment products, or introducing new offers for cross-selling through partnerships with platforms or other embedded finance players.

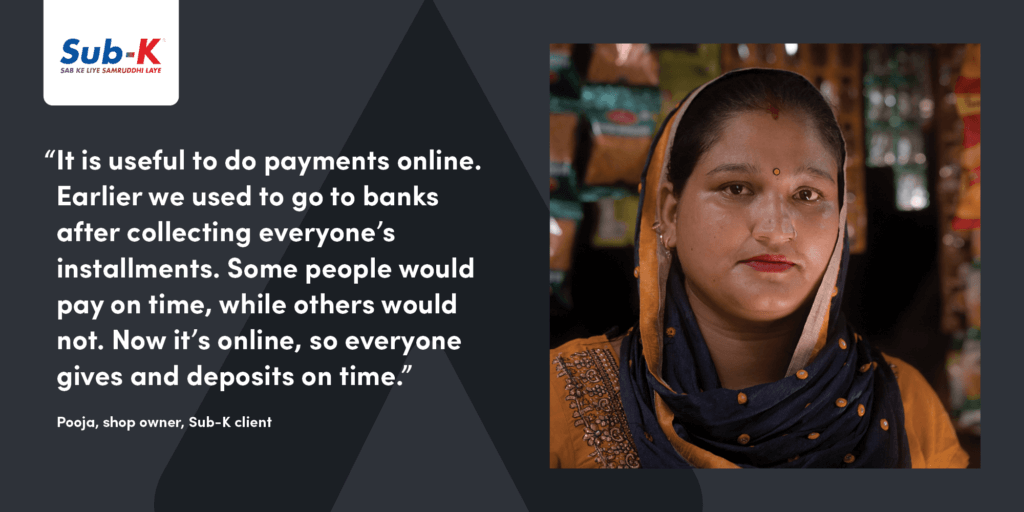

Partner spotlight: Sub-K

Sub-K is an innovative financial service provider in India that uses a digitally enabled model and a large network of agents to reach underserved people in rural communities, especially women entrepreneurs, and connect them to banks.

Sub-K’s initial focus on a marketplace proved difficult with COVID-19, as partner banks dramatically scaled back lending, so the company quickly pivoted to digital loan repayments through Sub-K Pay, expanding channels and points of interactions, accompanied by an incentive scheme for loan officers to encourage their customers to repay their loans digitally. Interestingly, the program quarterly KPI reporting noted a dip in digital usage after the incentive program’s expiration, which recovered after it was reinstated. This shows the importance of incentivizing loan officers to offer the human touch required to transition customers to new digital channels, as well as underscoring a broader cultural shift at Sub-K toward strategic use of data to monitor performance and make operational adjustments accordingly.

The number of customers using digital channels to repay their loans at Sub-K has increased by almost 100%.

The strategy and tactics are paying off. By Q3 2022, 72 percent of MAP digital product users reported no longer finding it challenging to make loan repayments on time, and 50 percent said this improvement came, at least partially, through the use of Sub-K Pay. Many have even gone as far to say that they would like the functionality to expand beyond loan repayments to enabling other digital payment functionalities.

Sub-K’s operational costs to manage repayments have reduced as more customers repay via Sub-K Pay, suggesting that digital adoption is increasingly driving cost savings and efficiencies, as well as greater flexibility in risk management. The number of customers using digital channels to repay their loans at Sub-K has increased by almost 100 percent.

Jitender Kalwani, Chief Financial Officer, Sub-KThe Sub-K Pay app is one of the most successful initiatives of Sub-K.

6. Human touch is still needed

A certain level of human touch remains important as barriers evolve, even for the most digitally savvy of customers.

Interestingly, an increase in digital maturity across micro and small businesses was met with a parallel shift in fear, misuse, and distrust of data and information found online. The nature and types of barriers to access and usage tend to shift as digital maturity increases, with the relative importance of physical barriers such as access to a smartphone and cost of data services decreasing, whereas behavioral barriers such as confidence and trust subsequently take on increased importance.

We are seeing a demonstrated shift in the level of maturity across our survey sample, with more micro and small business owners moving out of beginner and intermediate levels of maturity and into more advanced levels. As these individuals “graduated” into higher digital maturity segments, people’s confidence and trust in navigating digital tools may have increased, but they still reported concerns around security; these concerns were often higher amongst the more digitally savvy segments. Nearly 70 percent of MAP digital product users said they were confident in using their phones to make online transactions; however, 63 percent reported concerns around misuse and theft of their identities and private information if they engaged in DFS. Most of these individuals came from more digitally advanced segments.

This trend was most notable in Latin America, where about 70 to 80 percent of customers noted distrust and fear of data privacy, compared to 61 percent in Nigeria and 35 percent in India.

Understanding how to maintain and grow user confidence and trust in DFS in an increasingly digital and interconnected world is key to accelerating digital transformation at scale. As digital users increase their online presence, the risk exposure to data breaches and fraud heightens and creates new vulnerabilities for users.

Enhanced cybersecurity, increased transparency around the usage of customer data, and fraud protection are necessary steps for any FSP looking to digitalize their products, services, and channels. FSPs are increasingly compelled to bolster their institutional capacity for cybersecurity and build cyber resilience. Doing so is essential to ensuring longevity and protecting their businesses and vulnerable customers from the significant and often irreparable damage that can result from cybercrime.

Further to the efforts FSPs can make to secure their gates, key interventions that can drive trust directly in the minds of users are also needed. Such interventions may include the promotion of peer groups to dismantle concerns and encourage adoption, access to call centers for quick troubleshooting and support, and notifications sent to consumers around how to use the service or how to secure their devices. Empowering employees, especially those who are customer-facing, to speak out about any areas where they may suspect risks or mistrust amongst customers can help accelerate product improvements.

It is imperative to understand and respond to these new risks. Rather than digitalizing all processes overnight, especially amongst a segment that is only recently taking on more digital ways of doing things, we design with a combination of physical and digital touchpoints, particularly when it comes to areas of customer support offered throughout the product lifecycle. We will continue to improve our understanding of what is needed through increased research on customer data protection and interventions that incorporate “privacy and protection by design.”

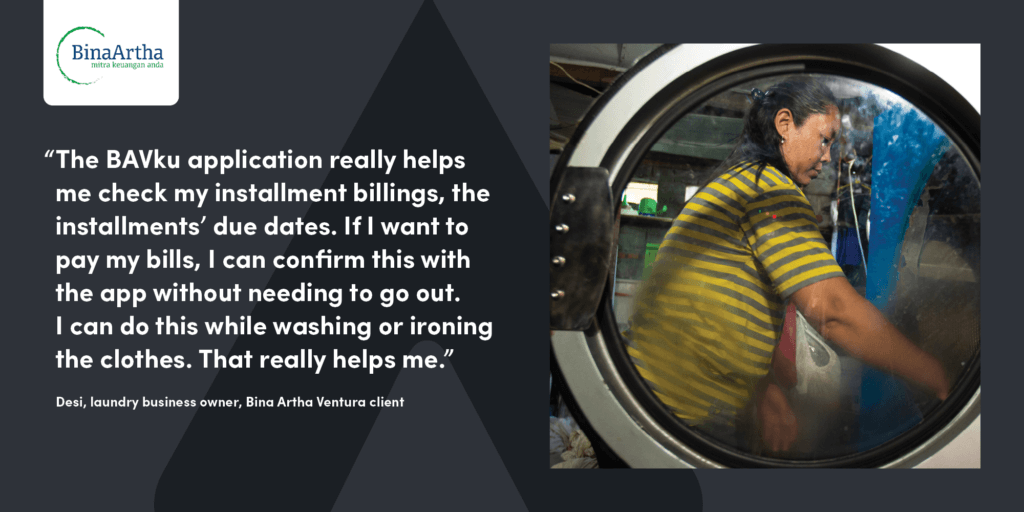

Partner spotlight: Bina Artha Ventura

Bina Artha Ventura (Bina Artha) is a leading financial service provider determined to bridge the gap between Indonesia’s formal and informal financial sectors. Bina Artha aims to better serve its customers, of whom 95 percent are women, by lowering costs, delivering credit faster, and reaching even more customers across the country — all while ensuring the right balance between technology and human touch.

Accion helped Bina Artha design and launch a digital customer engagement platform (CEP) — the BAVku app — through which customers can digitally interact with the institution.

More than 30,000 users downloaded the BAVku app in its first two months since launch.

Many of Bina Artha’s customers are new smartphone owners or have never used digital channels to access financial services. To build trust and confidence in using the platform amongst their customers, Bina Artha leveraged its field officers, who have a long-standing history and personalized relationship with their borrowers, to drive adoption and usage of the CEP. More than 30,000 users have downloaded the BAVku app in its first two months since launch.

Gonzalo Gonzalez, President Director, Bina Artha VenturaOur dream is to see that our clients can use their cell phones, smartphones, to check not only the next installment they have to pay or the balance of the current loan, but also to request a new loan, send transfers, or make top-ups or payments. Having additional products and services available on the app is the final goal.

Institutional readiness

We structured our work with FSPs and their clients to support six key strategies that financial inclusion-focused institutions need to keep in mind as they progress toward digital transformation. While we covered this topic at length in our FSP guide to digital transformation, we include a summary below. Additionally, the case studies presented in the key results section above provide specific examples of some of the main drivers of success and what influenced FSPs’ ability to transform.

Combating the digital divide on multiple fronts: Financially underserved individuals and businesses have varying levels of digital maturity, attitudes, and behaviors. Some segments may not have internet or smartphones, or simply do not trust DFS due to unfamiliarity or privacy concerns. Other segments may be early adopters of technology-enabled services and conduct their lives through their phones. FSPs can use their digital transformation efforts to reduce, rather than exacerbate, the existing digital divide by developing clear value propositions to help customers run their businesses better. FSPs can more effectively attract and retain clients by designing for both sides of the digital divide through omnichannel customer engagement strategies that balance tech and touch.

Optimizing organizational design: Traditional MFIs are radically different than digitally native financial companies in their ethos, culture, and organizational design. The digital transformation of MFIs requires developing a plan and implementing it simultaneously, and therefore also requires careful thought about how to integrate two very different operating models — one that is digital-first, the other not — under one roof. There is no one right way to organize for digital transformation, and how an institution decides to organize depends on their starting point, their digital maturity, and their desired end state. Although there are many ways to organize, there are three broad approaches: (1) a fully integrated holistic digital transformation where all departments have collective responsibility for transformation; (2) a digital center of excellence that sits within the organization and is responsible for driving digital solutions; and (3) setting up a standalone unit that builds, tests, learns, and launches products outside the FSP’s existing business operations.

Building (and rebuilding) a culture of experimentation: Many financial institutions tend to focus on short-term goals and quarterly targets. Typically, KPIs are not designed to encourage risk and innovation. However, digital transformation requires a culture that is willing to experiment, learn what works, and adapt. This requires institutions to seek alignment and buy-in on organizational priorities across the organization: the board, C-suite, management, and field staff. The development of a safe space to fail encourages a test-and-learn approach that is essential to organizational growth.

Having a clear data strategy: Data tools are often implemented to meet management reporting requirements. Data is not leveraged in a strategic way to empower and enable core initiatives of the business — including creating greater customer value and process efficiencies or making meaningful product innovations. Institutions can harness the power of data in their digital transformation by deriving greater value from the data they already have, acting based on insights, and prioritizing the management and governance of data to ensure it is used effectively and responsibly.

Future-proofing transformation with the right technology platform(s): Microfinance organizations often struggle with legacy technological systems, which have monolithic designs and are written in dated programming languages. These systems are inflexible, unable to support innovation, and can introduce security concerns. Digital transformation must be built on solid technological foundations. The more digital an organization becomes, the more it needs to invest in building future-proof and resilient platforms that can easily connect to cloud and open APIs. This requires balancing their long-term vision and short-term agility and ensuring backup and disaster recovery on the cloud where possible. Cybersecurity will increasingly be a key area for investment to prevent attacks on digital channels and systems.

Forming partnerships to achieve scale: Potential partnerships that can support financial institutions’ business goals often fall through due to a lack of a clear business case that aligns the goals of all parties, as well as questions that arise regarding ownership of the customer relationship. But partnerships with institutions such as telecommunication providers, ecommerce players, digital payment providers, or fintechs can enable new ways to leverage data, evaluate risk, and reach new customers at scale. Partnerships expand financial inclusion by building a digital ecosystem and a deeper integration with the formal financial services industry. To realize these benefits, FSPs should seek win-win partnerships and expand their definition of a partner.

Conclusion

Micro and small businesses reported a range of benefits from MAP digital product usage, from improvements in financial health (including the ability to repay loans on time, cover business expenses, and purchase sufficient inventory to meet demand) to business growth (including increasing sales revenue, hiring more employees, and starting new businesses). In Latin America, for example, 11 percent more MAP digital product users reported being able to hire new employees at the endline assessment, while in India, we saw a 20 percent spike in those who were able to increase their product sales and incomes. Women micro and small business owners reported especially salient financial health benefits, which they said came through their use of MAP digital products. Furthermore, active usage drove perception of value, and digital payments emerged as an area of opportunity.

Time savings were a recurrent theme in how customers perceived the value of the digital products they were using. Digital wallets and payment products that enabled or incentivized digital loan repayment saw particularly strong uptake and popularity amongst micro and small business customers, especially when supported by targeted FSP efforts to drive usage, such as branch activation campaigns and loan officer incentive schemes, for example.

However, despite increased usage, confidence and trust issues remain, pointing to the ever-evolving nature of digital risks. In the wake of COVID-19, low-income and vulnerable segments need the continued support of FSPs to navigate the new normal, restart their businesses, and build financial health so that they can build resilience to future crises and ensure they are not left behind again.

Why should FSPs prioritize and invest in digital transformation?

Digital transformation is not a one-size-fits-all solution. To serve micro and small businesses and low-income individuals effectively and at scale in this nascent digital economy, a robust digital infrastructure that can enable digital payments, digital identity verification, and data sharing platforms is essential.

Per the World Bank’s 2020 Digital Financial Services report, there are 850 million registered mobile money accounts across 90 countries with US$1.3 billion transacted per day. The GPFI/IFC “MSME Digital Finance: Resilience & Innovation during COVID-19” report stated that “77 percent of banks reported that improving customer experience for existing customers is the most important driver for digitalization. More than half of the banks cited attracting new customers as the second most important factor pushing them to digitalize, followed by lowering operating costs at 44 percent.” As digital payments, mobile banking, and relevant value-added services continue to grow in terms of usage, customer demand, and expectations, the business case for digital transformation has never been clearer for FSPs.

Under this partnership, FSPs are seeing financial benefits from increased digitalization, such as reduced customer acquisition costs, greater flexibility in managing PAR, and increased caseload productivity.

The results of the partnership provide powerful evidence in support of the business case for digital transformation; when done well, it can be a win-win for FSPs and their micro and small business customers, driving efficiency and cost savings for both, and contributing to building a fairer and more inclusive economy that expands opportunity and choices for all. However, success in digital transformation is determined more by an FSP’s ability to pivot and react to failures than it is by its ability to get everything right the first time.

What comes next?

Despite these encouraging results, there is still much work to be done and much to learn. Sustained usage of DFS is not a given — there is a need for intervention. FSPs must work proactively to achieve those results and encourage long-term behavior change amongst their micro and small business customers for them to convert to regular active users and reap the full promise of digital adoption.

We see value in continuing to directly ask customers to share their perspectives on their own lived experience. This survey represents a first attempt by Accion to “go beyond access” at the end customer level and understand how increased access and sustained usage of quality financial solutions — in particular of DFS — can help micro and small businesses benefit by growing their businesses, improving their livelihoods and strengthening financial health and resilience. Going forward, Accion aims to deepen its efforts to understand the impact of its work on the underserved.

Meanwhile, the digital divide and gender gaps persist. Work done with FSPs under the partnership demonstrated that well-designed solutions can drive sustained usage and see greater uptake by women, which underscores the continued need to help bring tailored solutions to reach women-owned micro and small businesses in particular, to help them rebuild and recover.

Significant shifts in the global economy continue to create new vulnerabilities for micro and small businesses. The pandemic severely impacted these businesses, and they continue to face challenges due to conflict, supply chain disruptions, inflation, and more. Meanwhile, increasing digitalization creates new consumer protection risks. More research is needed, for example, on emerging digital risks and social protection program design. At the same time, support is needed for FSPs and other players to create financial solutions that address these vulnerabilities sustainably.

We are confident that digital transformation is a powerful tool that can continue to address these challenges to scale appropriate, responsible, and sustainable financial solutions that meet customers where they are. We hope you will join us in this journey. Onward!

Cover photo credit: Toyin Adejoke Olu-Ayeni, provisions store owner in Nigeria, Accion MfB client

This paper is supported by the Mastercard Center for Inclusive Growth.

Accion would like to thank the following organizations for sharing their expertise and learnings for this paper: Accion Microfinance Bank (Nigeria), Annapurna Financial Pvt. Ltd. (India), Banco Pichincha Microfinanzas (Ecuador), Banco Solidario (Bolivia), PT Bina Artha Ventura (Indonesia), CÍVICO Digital SAS (Colombia), Dvara KGFS (India), Fundación Génesis Empresarial (Guatemala), and Sub-K IMPACT Solutions Ltd. (India).

The authors are also grateful to those who contributed to the success of the program, including: Program and Transformation Managers (Debdoot Banerjee, Iain Brougham, Sandra Calderon, Diego Gaviria, Mona Kapoor, Luis Merchan, Prateek Shrivastava, Raliat Sunmonu, Amy Stewart, Jose Wolff, and all project team members); the data analysis team (Henry Bruce, Siddardha Nelapudi, and Devika Misra); the survey implementation team (Aditya Agarwal, Maria Belen Garrett, Tannaz Daruwalla, Amit Gupta, Emma Morse, Siddardha Nelapudi, Leonardo Tibaquira, and Anjuna V K); as well as those who contributed their time and provided input, guidance, and editorial insights (Robert Abare, Lauren Braniff, Iain Brougham, Charlene Navarra, Megan Peterson, and Victoria White).

Explore More