Regions

- Brazil

- East Asia and Pacific

- India

- Indonesia

- Kenya

- Latin America and The Caribbean

- Mexico

- Middle East and North Africa

- Nigeria

- North America

- Philippines

- South Asia

- Sub-Saharan Africa

- United Arab Emirates

- United States

This report is supported by the Mastercard Foundation.

Executive Summary

The COVID-19 pandemic has altered the realities for inclusive fintech startups and the financially underserved customers they serve. Coping with lockdowns and social distancing, low-income people around the world are now turning to fintechs to save money, purchase insurance, or transact remotely. But fintechs are facing their own challenges, including unpredictable funding, a volatile investment market, and a severe economic downturn.

Investment funds seized up soon after the pandemic began, and while funding has started flowing again, venture capital may be less reliable and predictable for the foreseeable future. Startups need to focus on extending their financial runways while simultaneously finding ways to grow their businesses.

In the past, many fintech startups have followed a Silicon Valley model of chasing growth through customer acquisition. But customer acquisition can be costly: acquiring a new customer is anywhere from five to 25 times more expensive than retaining an existing one (without considering opportunities for cross and upsell). Fintech startups should consider alternative pathways to growth, namely via increased usage, uptake, and earnings among existing clients.

This shift to increasing value for users is extremely relevant in the era of COVID-19. Lockdowns and sharp decreases in demand for goods and services have left many families and small businesses extremely vulnerable. These people need more and new financial service innovations to rebuild their safety nets and livelihoods as their savings and inventories have been depleted. Increasing value for these users means finding new and better ways to meet their needs via meaningful, customer-centric value propositions.

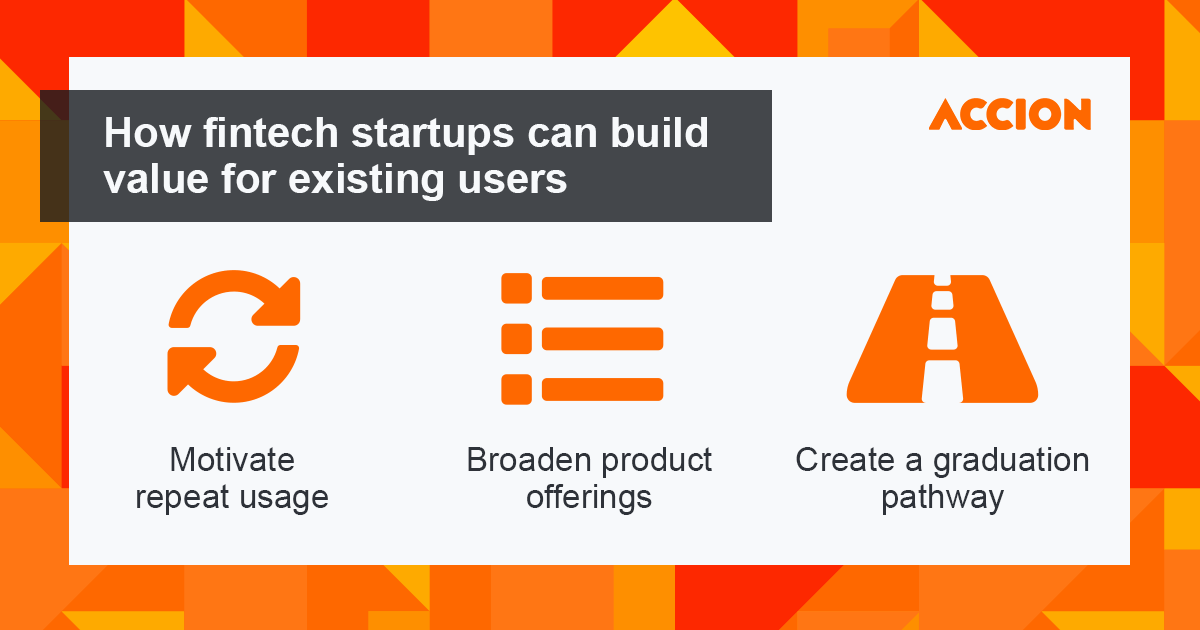

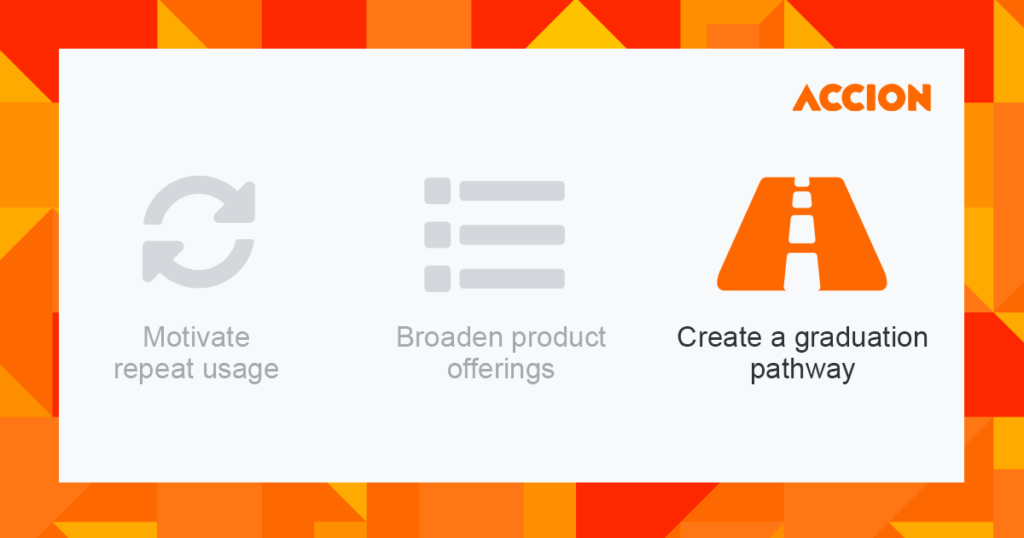

This paper features case studies on fintech startups around the world that have successfully grown their value propositions. These startups, all portfolio companies of Accion Venture Lab, illustrate three core strategies for growing value among existing users:

- Motivate increased usage of existing products,

- Broaden the suite of products specific to users’ needs, and

- Create a graduation pathway to reward retention.

The first strategy seeks to improve the user experience through features that encourage more frequent or in-depth use of products and services. The second strategy requires studying and applying users’ needs to craft a suite of products that address their particular pain points and fulfill more of their needs. Finally, the third strategy boosts value for users by sweetening and improving their terms over time so that they stay engaged. To execute each of these strategies, startups must stay closely attuned to users’ needs and experiences, and apply that knowledge to develop products that meet those needs.

Introduction

Inclusive fintechs face uncertain futures in the era of COVID-19

Fintech startups, particularly at the early stage, face a more uncertain investment climate in 2020 than in years past. Funding to fintech companies for the second quarter of 2020 hit $10.2 billion, up 11 percent from the first quarter, and 1 percent greater than last year. However, total deals to fintech companies fell 30 percent in the second quarter compared to the first, suggesting capital has been flowing to larger deals in mature companies than smaller investments in early-stage startups.

Financial service providers are also facing volatility in business activity. Some predict that lenders to small and medium-sized enterprises (SMEs) will face high default rates as their customers’ shops are shuttered, and others noted early in the pandemic that remittances, a critical lifeline for many low-income households in emerging markets, will drop sharply as a result of the economic crisis. While these trends are not good for financial service providers, the pandemic has also accelerated digital adoption and opened new doors to growth for fintech companies. Digital payments acceptance and usage has increased overall, governments are digitizing relief payments, and new opportunities are emerging for insurtech, digital lending, and payment platforms.

Moreover, underserved clients are more vulnerable than ever and need financial service innovations both now and as they reestablish their livelihoods. As lockdowns end, low-income families will find their savings exhausted, their businesses stalled or bankrupt, and their future incomes uncertain. The World Bank projects that the pandemic could push up to 150 million people into extreme poverty by 2021, at the poverty line of US $1.50 per day. Surveys from the Center for Financial Inclusion find that SMEs around the world are also making deep cuts to personnel, facing steep declines in profits, or are closing altogether. These vulnerabilities point to opportunities for inclusive fintech startups, as people need new income streams and financial services to build resilience, restart their businesses, and establish new ventures.

Furthermore, users may also be more open to trying new products from companies they trust as they find their old ways of transacting or savings are no longer feasible. This crisis is leading to step-changes in adoption of digital financial services, which bodes well for fintech startups. Others note that retention rates for existing and new users have actually improved since COVID. Startups may find their users more open to trying new services, especially since they have trusting relationships already in place.

Moreover, as communities reopen, the needs of these families will be different than they were before. For example, evidence suggests that households that experience a crisis also increase their savings rates. This crisis will likely cause lasting shifts as people become more reliant on e-commerce, gig work, and digital transactions.

Startups are well positioned to meet these shifts since they have the flexibility and culture to listen to users, innovate, and test opportunities. Though many investors wait for more clarity on what the future looks like, innovative startups that are client-focused will do best when it comes to fundraising.

It’s time to shift away from growth at any cost

Of course, startups must find a way to grow even in this challenging environment. They should do this by increasing value for their existing customers, starting on day one. While most startups have customer retention strategies within their sights, conventional wisdom among founding teams has been to prioritize new customer acquisition, and then turn toward providing extended value and (simultaneously) achieving profitability.

This wisdom follows the hockey stick model established by Silicon Valley and reflects a time when investment dollars were flowing more freely. To date, many fintech startups have secured investment dollars by demonstrating potential for scale via significant growth in customer acquisition and a sizable total addressable market. These early funding rounds were often secured without much to show for profitability and retention. Pitch decks associated with these rounds have tended to focus on strategies to acquire new customers and often fail to even mention customer lifetime value.

To demonstrate promising customer acquisition rates, startups that are still establishing their brands tend to cast a wide net via costly marketing campaigns. These wide funnels ultimately mean that few users ultimately contribute to profitability, thereby driving up customer acquisition costs.

But many startups’ are shifting their focus away from a “growth at all costs” mentality, driven by high profile failures of unsustainable growth, like the implosion of WeWork, and the volatility of investment dollars. This shift in thinking reasserts the need for good core business principles and advises the community against getting swept up in the hype around unicorns and hockey stick growth.

Given this shift, startups need other ways to demonstrate growth and profitability via greater engagement, usage, and value for users. Moving away from acquisition alone and toward value means building bigger, better value propositions and tracking how much startups are earning over time from each customer relationship. This shift also requires expanding performance metrics to capture and reflect how value has increased, including product usage rates (frequency and product type), retention over time, and customer lifetime value (the predicted net profit attributed to the entire future relationship with a customer).

Three strategies can build value for existing users

Working toward long-term customer value is not as simple as it may seem. Many early-stage startups are famous for acquiring customers only to lose them soon after, like a leaky bucket. Leaky startups may acquire users but then face low usage, low retention, and limited ability to grow their product offerings since their value proposition and/or execution does not resonate with users.

To avoid such a fate, startups looking for organic growth need to distinguish themselves with tailored value-added services and product offerings that keep customers engaged and satisfied in the long run to achieve growth and profitability. Startups with this approach will have more engaged users, higher NPS scores, and are more likely to secure referrals among their users. This approach is critical to creating social impact as inclusive, impactful businesses are the ones that consistently meet the needs of their customers beyond a one-time purchase.

At Accion Venture Lab, we have a front row seat to what works for startups. This paper highlights three successful strategies that our portfolio companies have deployed to increase value and build loyalty with customers.

Strategy 1: Motivate increased usage of existing products

Finding ways to grow the benefits and value of financial products can encourage users to use products more frequently and in-depth. Although adding features and value-added services to encourage usage can increase the cost of delivering a product, doing so can also drive business growth if the result is more-frequent, higher-ticket product usage and longer-term retention. After all, churned or inactive users are extremely costly to a business that has already invested in acquiring and activating them. Moreover, using a product infrequently may only produce limited benefits for users and greater usage may better help them achieve their financial goals. In this case, the concrete method for motivating usage will depend on the user and the service in question, however the strategic pathway to growth is to motivate increased frequency or depth of usage by growing the value of the product in question.

One of the startups in Accion Venture Lab’s portfolio, Tienda Pago serves MSME retailers specialized in consumer goods in Peru and Mexico via short-term rotating credit for inventory. Among the strategies Tienda Pago has tried—promotions, messages, and discounts—human engagement (via an in-person or telephone conversation) has most reliably increased usage of the product. MSME customers deeply value communicating and interacting with a person from the Tienda Pago team. But this engagement mechanism is costly, so the team developed a smart way for deploying it among users that are likely to churn, thereby furthering retention and increasing usage among new users.

Another startup, Field Intelligence, found a way to leverage its existing data collection routine to increase value for their customers by providing them personalized recommendations of their product offerings. Currently operating in Nigeria and Kenya, Field’s suite of products helps pharmacies overcome challenges in inventory management, distribution services, and financing. Field’s tailored recommendations for pharmacies have driven increased usage, growing both Field’s own business and those of their customers. By increasing the value that pharmacists derive from working with Field via data-driven recommendations, the team has been able to grow the number of products that pharmacies buy from Field, increasing the depth of the pharmacy’s usage of Field’s service.

Advance, a salary advance provider in the Philippines, started by acquiring employees via payroll companies. However, the team found that depending on payroll companies to intermediate contact with employees made it challenging to drive activation rates of its product. As such, the team introduced a B2B2C approach to be able to have direct contact with users to be able to market and demo the product directly with employees through their employers. This direct contact significantly increased customer activation and borrowing rates.

Strategy 2: Broaden the suite of products specific to users’ needs

To retain customers and provide them with real value, startups can develop products that meet more of existing clients’ unmet needs. Especially among underserved people and businesses, a number of unmet needs and gaps in service can arise, often because these users have particular needs (especially after a crisis like COVID-19) or because mainstream providers may be reluctant to serve them. Given that startups have already developed relationships with these users, earned their trust, and gained unique insight into their needs and preferences, expanding the suite of products to meet their needs can be an opportunity for growth.

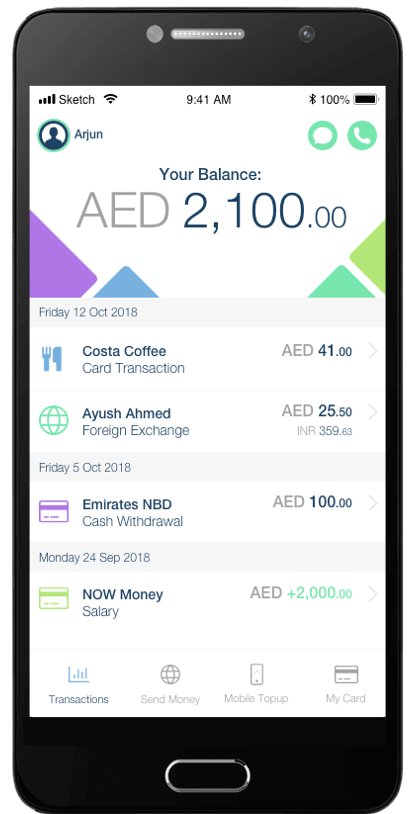

NOW Money serves employers of migrant laborers in the United Arab Emirates to provide payroll services. Instead of distributing cash cards like their competitors, NOW Money provides workers with a bank account, debit card, and smartphone application from which they can make local payments, international remittances, and cash withdrawals at local ATMs. Migrant laborers tend to have low trust in financial institutions and have a harder time conducting daily transactions given their exclusion from the local financial system. In response, NOW Money promoted mobile top-ups as a way to encourage users to maintain balance in their accounts and to create an entry-level product for migrants to execute a low-risk, low-cost transaction with which to build trust. NOW Money has been able to leverage their deep understanding of migrant needs to grow their business, meeting more of their financial needs.

Pintek, an education lender in Indonesia, started out serving private schools and training institutions with a payment product that manages invoices from schools and provides credit to qualifying families to help them break semester payments into monthly installments. Given the limited total addressable market, Pintek expanded their view of schools’ needs to offer credit to them directly. Schools have regular income but lack the collateral and structured income streams that banks need to issue loans. Since Pintek already had visibility into schools’ invoices, the team was able to leverage that knowledge to underwrite loans for repairs and emergency costs, as well as for longer-term expansions and rental contracts. Knowing their users so well has allowed Pintek to expand their suite of products to better serve their customers, thereby growing their business.

In Brazil, micro-entrepreneurs can register as Individual Microentrepreneurs (MEIs), allowing them to pay a single monthly tax to obtain benefits like social security and access to financial services. While acquiring and paying for the MEI classification is relatively simple, ongoing compliance with the tax payment is low. Fintech startup SmartMEI noticed this gap and started to acquire MEIs by offering a free tax and accounting app. Even as the app and user base grew as the startup added features and customers (e.g., gig workers), they still struggled to monetize the product. Once SmartMEI acquired gig workers, they realized that those workers couldn’t access their earned wages and were looking for ways to smooth their incomes. In response, SmartMEI launched a salary advance product that has rapidly increased revenues as well as the proportion of active users. This winning feature came from a close understanding of gig workers’ finances and has proven extremely valuable to SmartMEI’s original MEI users.

Strategy 3: Create a graduation pathway to reward retention

Some startups in Accion Venture Lab’s portfolio have been able to create business growth by helping their clients grow as well. This strategy is particularly valuable for startups with products designed to help customers transform their financial lives. In these cases, as customers grow, they may find that startups’ products no longer serve them. Startups can retain these customers by developing products that meet their evolving needs. This means creating durable pathways for evolving financial needs that promote and orchestrate a journey towards financial health.

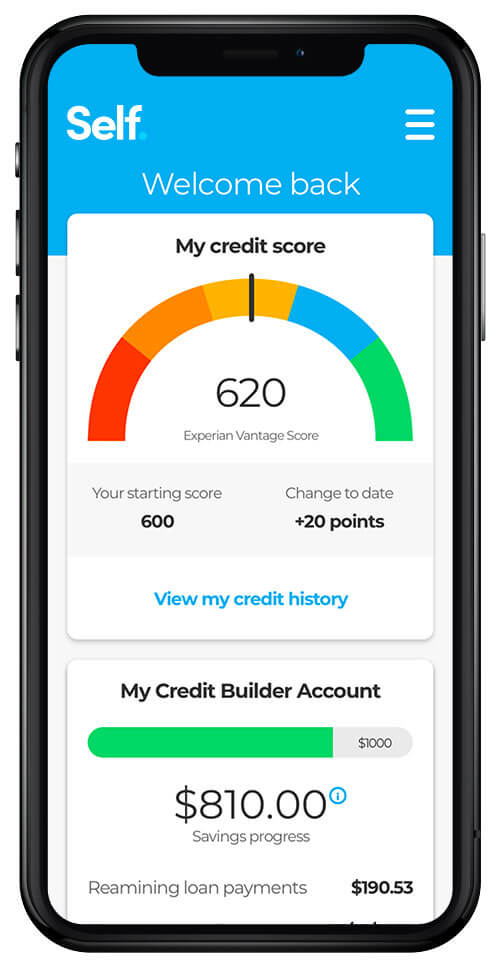

Self, a startup in the United States, has developed an innovate way for customers with thin or damaged credit files to build their credit scores. Through Self’s credit builder account, a loan is issued to a user to buy a certificate of deposit (CD). Once the CD is purchased, the user “buys it” back via monthly repayments, receiving the CD (plus interest) at the end of the loan term. Since the product is designed specifically to help those with inadequate credit scores build their scores, it only has a dramatic impact one time. Rather than lose their successful clients to other providers, Self has developed a secured credit card that seamlessly transitions users from the initial product and helps on the next step in their journey to financial health. The credit card helps them further increase their credit scores and establish good financial habits.

SmartCoin is a digital lender in India that uses an all-digital platform to provide instant, mobile-based loans to Indians who are unserved by both commercial banks and microfinance institutions. The startup built a simple interface that leverages a wide variety of alternative data to rapidly deliver credit products to this group. India has seen an explosion of digital lenders, and since apps can be deleted as easily as they can be downloaded, many startups struggle to build loyalty and retain their customers. To drive retention, SmartCoin has developed a number of strategies to gamify repeat usage and grow their value proposition among high-quality borrowers.

Apollo Agriculture helps farmers in Kenya improve their productivity and grow their incomes by providing an all-in-one farming bundle that includes financing, agri-inputs, insurance, advice, and other inputs, which together enable best-practice cultivation. However, Apollo found that farmers who needed the full bundle one year may not need the entire package the following year. To continue meeting these farmers’ needs, Apollo is building flexibility into their product suite so that farmers returning to Apollo can procure one or some of the inputs financed by Apollo, instead of all of them. This flexibility better reflects that variability that farmers face in their work and resource availability season-to-season.

Growing value for users is fundamental to success

Ultimately, startups’ success is based on their ability to meet their users’ needs. Instead of focusing on costly customer acquisition during lean times like these, startups should increasingly focus on growing with their existing clients by increasing the value provided to them via their existing product or by offering new products. The startups in Accion Venture Lab’s portfolio showcased in this paper illustrate a variety of innovative strategies to increase value for users.

Growing value for users means startups must be customer-centric, crafting products that meet their particular needs and circumstances. In turn, this helps customers build resilience, access new opportunities, and better manage their daily lives. Doing so will create the benefits and impact that inclusive fintech startups and investors like Accion Venture Lab have set out to create.

Case studies – Strategy 1

Case 1.1 Human engagement can prevent churn among SMEs

Once usage has dropped, re-engaging a customer can be expensive and often fails. Instead of waiting until a user has churned, it is helpful to identify those who are likely to do so, and motivate them to re-engage before the fact. Doing so requires investing in data analysis and abilities to predict who might churn, and developing effective (re)engagement strategies.

Tienda Pago serves SME retailers specialized in fast-moving consumer goods (FMCGs) in Peru and Mexico via short-term rotating credit for inventory, which allows them to place larger, more diverse orders at more affordable rates. Moreover, Tienda Pago partners with distributors to pay for inventory directly, thereby saving distributors cash management efforts and facilitating their access to smaller merchants. The company has found that if retailers stop using Tienda Pago’s credit product for several months, they are unlikely to resurrect down the road. However, they have found that reaching out to merchants can prevent them from disengaging and bring down churn rates.

Given these observations, the Tienda Pago team developed a data analysis and machine learning algorithm to target stores that are likely to churn, and invests in human-touch engagement to drive usage and create stickiness, thereby recovering users before they churn.

Background

The informal economy in Mexico is sizable, having contributed 26 percent of GDP on average between 2003 and 2012, and employing approximately six in ten Mexican workers. Most of these businesses are small, in fact nine of every 10 businesses in Mexico are SMEs.

Together, the large numbers of small enterprises and high levels of informality, mean that many owners do not have access to formal financial services. Research has found that more than half of SMEs lack a bank account and more than three quarters lack access to credit. Even those SMEs that do have access to credit via a commercial bank only do so via a guarantee scheme from NAFIN, Mexico’s main development bank.

Since access to appropriate formal financial services doesn’t exist for this group of SMEs, most depend on credit from suppliers. This poor access to credit severely hamstrings SME growth and operations since most depend on inventory credit to stock their stores.

While tenures and repayment schedules between SMEs and distributors match (retailers typically repay as they restock on a revolving basis), the effective interest rates are high and such credit locks retailers into disadvantageous relationships with specific suppliers.

Those who do not take credit from suppliers have few alternatives; they rely on informal lenders who evaluate the SME owner as an individual, rather than as a business owner, again at very-high effective interest rates.

About Tienda Pago

Tienda Pago saw an opportunity to serve these SMEs by offering inventory credit facilitated through partnerships with large distributors. The SME retailers use Tienda Pago’s app to make an order for fast-moving consumer goods, for which Tienda Pago extends the store a loan while paying the distributor directly. The retailer then repays Tienda Pago for the order (plus interest) on a weekly basis.

Tienda Pago benefits both retailers and distributors. With access to the Tienda Pago credit, retailers can increase their order sizes, improve the quantity and diversity of their inventory, and potentially generate 20-30 percent more in revenue. Distributors save on cash management since the delivery route effectively becomes cashless. Their delivery teams no longer need to collect payments, which means saved time, fewer errors, and lower risk. In fact, some distributors are now including areas for delivery that they had previously deemed unsafe since cash transactions are no longer unnecessary.

As of July 2020, Tienda Pago counts 45,000 registered users, divided among power users (use on a weekly basis), regular users (monthly), and occasional users (quarterly or less frequent). The challenge for Tienda Pago has been that regular and occasional users churn 30 percent more than power users.

Human touch for regular usage

To address these low usage rates, the team tested a number of engagement strategies. For example, the team tested digital discounts, free transactions, and reminder campaigns (via WhatsApp and the Tienda Pago app). They found that promotions from distributors or Tienda Pago, like a free case of beer, reliably got merchants to place orders but that such promotions were expensive to offer on a recurring basis. Moreover, taken as a group, they found that these strategies achieved an additional order, but none reliably moved the needle to establish more frequent usage. Instead, the team found that many retailers would just take advantage of the promotion and then wait for the next one, but never moved to become regular or power users.

Ultimately the Tienda Pago team realized that meeting or speaking with the owners (either in person or via the phone) was the most effective way to encourage more frequent usage. Regardless of the script used or the staff person involved, Tienda Pago found that users had a similarly positive response to human outreach. However, given the cost of this strategy, the team leveraged a machine-learning approach to target these conversations among users most likely to move into the regular usage category. This data-driven approach has targeted their efforts on two moments in the user journey: 1) establishing regular usage with new merchants, and 2) preventing churn among established users. Human touch, together with this data-driven targeting, has effectively established regular usage and prevented churn among 25 percent of users.

Become part of the established routine

A look at the data revealed that power, regular, and occasional users diverge early in their engagement with Tienda Pago; in fact, during the first 90 days of usage. If retailers made weekly or biweekly purchases in the first several months, they would likely go on to become power users of Tienda Pago. More precisely, data analysis showed reaching six transactions in the first 90 days correlated to a high likelihood of that merchant becoming a power user. Such users exhibit this behavior early in their engagement with the service, and very few get there by ramping up from a lower-frequency routine. Furthermore, once a user becomes regular, maintaining engagement is straightforward via WhatsApp and other low-touch mechanisms. This means that Tienda Pago needs to become part of the merchant’s ongoing purchasing routine soon after acquisition.

In 2017, the team found that 57 percent of new customers were reaching the weekly/biweekly purchasing routine (six transactions in 90 days), but that around 40 percent were falling into the low-frequency user groups fairly soon after registering.

Now, to address those who are slow to take up the product, the team carefully tracks usage during the first 90 days and immediately deploys various touchpoints to encourage more frequent usage. The team first tries to contact the merchant via phone, and if they are unable to connect with them, pays a visit in person. They target users who have made at least four orders (so have had some positive interactions with the service) but have yet to become power users.

This targeting has improved uptake. Whereas 57 percent of new merchants became power users in 2017, by 2020 over 67 percent do so, thanks to Tienda Pago’s additional engagement strategies.

Prevent churn

The team also deploys human touch when a merchant may be experiencing a change in their purchasing routine (perhaps due to a change in family circumstances, opportunities, or finances). Reaching out to these users before they drop off helps Tienda Pago prevent churn.

For the second group, those moving from high- to low-frequency usage, the triggering event is usually (around 50 percent of cases) a default. As such, the team works with high-frequency users at their first default to create a payment plan or find some other solution.

The team has also developed a machine learning algorithm that analyzes transaction size, frequency, recency, and other metrics to identify those retailers who are likely to churn based on historical data. Once identified, the team reaches out to remind the merchant about the service and to build the relationship with Tienda Pago.

In deploying these human touchpoints, the team must carefully balance cost and effectiveness. While a number of visits can reliably get merchants back to using Tienda Pago, at some point the cost of these visits can exceed the business upside of the individual account. The team makes an effort to re-engage a merchant for three months. After that period, they deactivate the client, so that, if he wants to reactivate, he has to do a quick training on how to use the app, ensuring the team has a chance to touch base and re-engage that merchant.

As SMEs start reactivating after COVID-related lockdowns, Tienda Pago is readying their operations to help them get back up and running. SMEs will need access to credit to restock their shops and intelligence to anticipate changing needs. In both cases, Tienda Pago will be an ideal partner to ensure their longevity.

Case 1.2 Features that increase value can grow usage

Growing product features so that users get more value from engaging with your service can increase usage depth (purchase size) and frequency and motivate long-term retention. In some cases, adding features and increasing value is just a matter of leveraging your existing infrastructure and data so as to better serve your users.

Field Intelligence launched a product called Shelf Life which provides pharmacies in Nigeria and Kenya inventory management, product distribution, and financing (via product consignment) as an all-in-one solution so that pharmacists can focus on patients and service. Shelf Life meets the varied needs of pharmacies and provides a broad, diverse solution because their team of agents develops deep relationships with each pharmacy, collecting significant amounts of high-quality data on a weekly basis.

The Field team has leveraged the data they already collect to help pharmacies manage their product mix, including which SKUs to carry and how to sell complements and substitutes. This has increased usage, thereby growing both the pharmacies’ business as well as Field’s.

Background

African countries account for only 0.7 percent of the global pharmaceutical market, and even this limited access is badly skewed. Only 10 of the continent’s 54 countries accounting for 70 percent of the total. As a result, half of Africans do not have access to essential drugs. This limited last-mile access is largely provided via independently-owned pharmacies and clinics since retail chains are small (together, the 10 largest pharmacy retail chains in Nigeria, Kenya, and Ghana only manage 186 outlets for a population of almost a quarter of a billion people).

Weak access is further compounded by the fact that pharmaceutical supply chains in emerging markets tend to be inefficient, featuring a fragmented web of importers, wholesalers, distributors, local distributors, and numerous retailers, often operating parallel distribution systems. This complexity, together with weak and inconsistent infrastructure, mean that inventory and stock are not well matched to local needs and rates of turnover. Together, these factors result in frequent stockouts, expired medicines on the shelf, and poor availability of specialized medicines.

Furthermore, pharmacy managers and owners are typically pharmacists by training, so struggle with the business side of inventory and liquidity management. The balance is difficult to strike as overstocking causes losses since expired medicines must be trashed, and understocking also causes lost income since customers have to go elsewhere to find their medications.

Fortunately, research has shown that simplifying the supply chain and allowing providers to directly order products from suppliers can improve the duration and frequency of stockouts.

About Shelf Life

Shelf Life is Field’s full-suite solution for pharmacies across Africa, starting in Nigeria and Kenya, that simultaneously solves pharmacies’ inventory management, distribution services, and financing problems.

The product started in 2015 as a logistics and software solution (Field Supply) to address last-mile distribution challenges in Nigeria. But the team soon realized that last-mile challenges would not be solved by software alone and, in 2017, expanded their efforts to launch Shelf Life, in which Field manages the pharmacy’s inventory by placing products on shelves on a consignment (Pay-As-You-Sell) basis.

Today, for a weekly subscription fee, the Field team provides inventory advice in the form of forecasting exactly how much stock needs to be on the shelf for the next supply period; sells the products, delivers and arranges them; and provides financing for their purchase. The cycle starts with agents visiting the pharmacy on a weekly basis. Agents leverage Shelf Life’s algorithm-driven inventory management tool, which considers the pharmacy’s historical sales records as well as existing inventory, to help the pharmacist place a weekly order. Field has direct relationships with wholesalers, distributors, and manufacturers, which ensures quality and authenticity of its products and also allows the company to offer pharmacies more medicines and at a lower cost, while also saving them the hassle of dealing with multiple distributors. The team then delivers the products, saving the pharmacist logistics and delivery costs, and arranges them on the shelf according to best practice, arranging displays and signage so as to maximize sales. Furthermore, the products are provided on consignment, freeing up working capital and decreasing pressure to take out expensive credit. Altogether, the risk of product expiration is gone, working capital not tied up, logistics are cheaper and simplified, and planning and stock keeping are covered.

Not only are Shelf Life pharmacies better run and more profitable, patients get more reliable access to high-quality medicines as well as the opportunity to purchase a more diverse set of goods. In the future, Field plans to provide an online directory of pharmacies and medicines so that patients (as well as producers) know where products are available. Within six months of launching, Field had onboarded 50 pharmacies, and was managing almost 200 pharmaceutical products for those pharmacies, focusing those with the highest-turnover and largest margin for pharmacists.

At the center of the Shelf Life model is the team of distribution and sales agents, who maintain close relationships with each pharmacist. A team member personally visits each pharmacy every week (bi-weekly during COVID) to count inventory, discuss trends, support marketing, and place orders. This high touch model is necessary to get the level and quality of data needed to power its supply chain management database, which powers the planning and forecasting for all Shelf Life pharmacies. To start, the agents give Field direct insight into the challenges and opportunities faced by pharmacists, allowing them to better anticipate needs and trends.

Secondly, the pharmacists value their relationships with the agents and Field has found that this value supports stickiness. The agents also provide advice and support on displays, shelf space, signage, as well as inventory. For example, many agents report that they convince pharmacists to stock contraception, which they may have been reluctant to do. Field will also deploy a senior pharmacist for technical advice when needed, for example, with new medications.

Growing value

While the agent network provides unquestionable value, managing them and the time it takes to collect this data is a cost center for Field, and one that is fixed. The agents spend as much as an hour a week at each pharmacy and as their numbers grow, hiring and managing the team is a challenge. As such, the team is always looking for opportunities to increase revenue earned for each pharmacy relationship so as to spread this cost over more revenue streams.

The Field team has recently found a way to provide even more value to pharmacists via product mix recommendations, thereby distributing the cost of agent management over greater value provided to users. This additional value both motivates retention as well as additional sales as the recommendations encourage users to add additional product subscriptions to their accounts.

Informally, the agents had started recognizing profitable product pairs, or when pharmacies were not ordering a product that was selling well at similar businesses. Seeing an opportunity, in 2018, the team started by picking a few well-run pharmacies, analyzing their inventory relative to similar pharmacies, and then offering advice on a few more SKUs via the phone. By 2019, these suggestions had increased the number of products purchased from Field by 60 percent, attesting to the power of evidence-based recommendations for increasing sales.

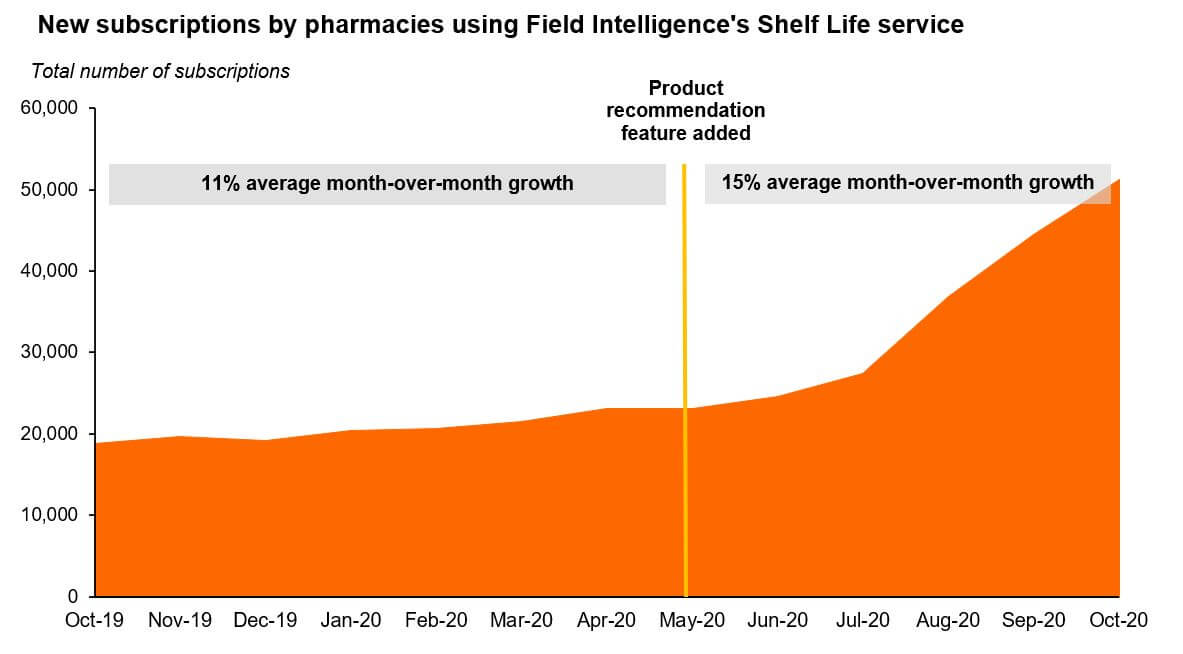

Noting this initial success, in February 2020, the Field team further invested in the analytics behind the recommendations, leveraging the data the agents already collect to provide more and better-quality recommendations, and with greater frequency. Now, along with their invoices, pharmacies receive a report on their performance relative to their competitors, areas for growth, a list of products are good complements/substitutes, and where there may be missed opportunities.

In turbulent times, these insights have allowed pharmacies to respond more quickly and more intelligently to changes in market demand so that they better avoid problems of over- and under-stocking. Even given the difficult times, the product recommendation feature has increased subscriptions (the number of products ordered at each pharmacy) by 15 percent on average in just a few short months (as high as 80 percent in some territories), dramatically increasing depth of usage even during a crisis. In Q3 2020, as COVID-19 lockdowns ebbed, the team was able to grow their subscription base by 79 percent.

Looking forward, the team is committed to supporting pharmacies as they grow their businesses and serve more of their customers’ needs. Their profound knowledge of the pharmacy business and deep relationships with pharmacists mean that the startup is well positioned to support their long-term success.

Case 1.3 Speak to your users directly

Many fintech startups pivot from B2C to B2B models to bypass expensive customer acquisition and to onboard many users at once. However, engaging a third party to intermediate relationships and outreach to users can be costly, especially when it comes to activating users (after acquisition). As such, fintech startups struggling with low activation and usage may want to develop channels to reach users directly.

Advance is a fintech startup that helps low-income workers smooth their incomes via salary advances. These advances help users meet expenses when liquidity is running thin by giving them access to money they have already earned. The team started by partnering with payroll service providers so that the Advance widget would appear on the employee income dashboard of employers (effectively a B2B2B2C model). However, the startup was dependent on the payroll company to communicate the value proposition and to promote the service as they did not have a direct channel of communication with users.

To craft a more direct channel to users, Advance has started acquiring large employers directly, giving them the opportunity to explain and demonstrate the product with users directly, thereby increasing activation and uptake.

Background

Like most low-income people around the world, most Filipinos live paycheck to paycheck (80 percent) and lack access to a bank account (69 percent of Filipinos lack a savings account). As of 2018, 34 percent of cities and municipalities still lacked a banking presence and just 12 percent of Filipinos had borrowed from a formal financial institution.

While a segment of these vulnerable people own/operate SME, many are also employed, as low-wage employees. In fact, work poverty is pervasive in the Philippines, given low access to productive jobs. The most vulnerable workers are in the informal market — self-employed or unpaid family workers — but many formal employees are also low income and share characteristics with informal workers. Although they benefit from labor and wage protections, they still struggle with access to finance and demonstrate poor financial health, running low on liquidity at the end of the month and depending on expensive, informal credit.

About Advance

Given poor financial access among hardworking employees in the Philippines, fintech startup Advance developed an API for payroll companies to integrate into their systems for employees to take out salary advances. The team reasoned that salaried employees needn’t rely on expensive credit when they had earned wages pending. They also realized that payroll companies, which already had thousands of employees onboarded onto their financial service apps, could provide them quick access to those employees. Even better, those payroll companies already had valuable financial information like earnings records and bank account details that could make salary advances seamless.

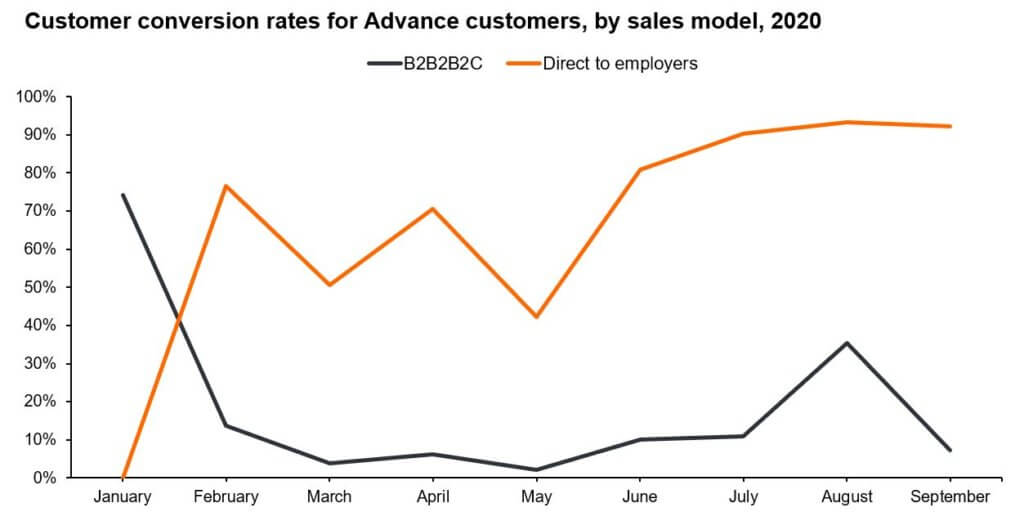

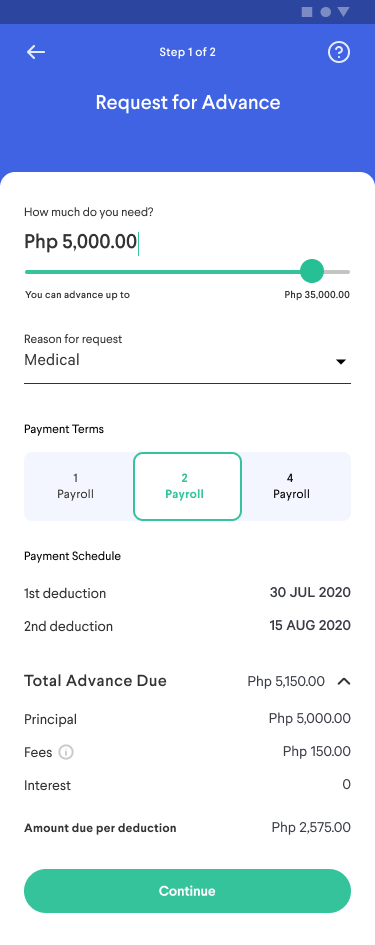

After developing the API, starting in 2018, the team set out to build partnerships with payroll providers. Starting with just a team of four, they quickly closed the two largest payroll companies, serving over 100 smaller companies and gaining access to over 150,000 potential customers. The Advance widget would appear within the payroll application, and users only needed to click it to request an advance amount. Advance offered users the opportunity to borrow up to 30-50 percent of their salary, with a repayment schedule of a few weeks or a few months. While 30-40 percent of users would click the widget, effectively “signing up” for the service, only 30 percent of those would go on to borrow. As such, effective activation rates were only 10-15 percent, meaning the number of total borrowers by mid 2019 was fewer than 500.

The Advance team had known to expect this challenge via the payroll sales model. After all, they were effectively two steps away from users (B2B2B2C). The model facilitated quick acquisition but contact with users was mediated by the payroll providers and the HR departments of the employers themselves. These layers mean that getting past acquisition to activation was challenging, and that Advance had few avenues through which to address the challenge.

Furthermore, the team realized many of their “acquired” customers were not actually eligible for salary advances. For example, a company of 1,000 employees might include several hundred new employees or contractors who are ineligible for salary advances. Another couple of hundred may have financial obligations and debt burdens with the company or other service providers that disqualify them from an advance. The team would find that only a few hundred of the 1,000 employees were ultimately eligible for a salary advance.

Approach users more directly

Observing these challenges, at the end of 2019 the team decided to add another sales model for offering salary advances. Instead of depending on payroll companies to reach employees, the team decided to onboard large enterprise employers (staff size between 800 – 2,000) directly. The initial team of four expanded and built a direct sales team of another four team members.

The new sales team allowed Advance to acquire employers directly and, importantly, pitch and demo the salary advance product directly with employees. Selling directly to employers allowed Advance to remove a layer of intermediation and communicate directly with potential users via on-site roadshows, pamphlets, and demonstrations. This direct access provided immediate results; 70 percent of users that signed up at product demonstration sessions went on to borrow (relative to 10-15 percent via the B2B2B2C model). The team also noted that once users tried the salary advance, they felt the benefits immediately. Within a few quarters, Advance was happy to note that retention a year later was 88 percent and that retention on a 60-day basis was over 60 percent.

While the model has had advantages, it has also created some new challenges for Advance. For example, HR departments are not able to provide Advance with extensive financial and bank information like the payroll companies could. Instead of just “clicking the widget”, directly-acquired employees need to fill out their bank information, provide a payslip, etc. Moreover, HR is often quite leery of partnering with a salary advance company, and nervous about maintaining the proper legal controls in sharing information with Advance.

Furthermore, the model involves a long sales cycle. It takes between 4-6 months to acquire and onboard a new employer. There are more hoops to jump through with direct sales since these organizations are more complex, given their size and their existing ways of doing. Such companies are not accustomed to dealing with partners, especially when it comes to sensitive information like staff lists and contact information.

Addressing these challenges forced the startup to adapt and innovate, providing a number of important learnings that have ultimately positioned the team well for COVID-19. For example, to motivate new users to provide data and details, Advance has learned to craft a pathway for them — offering a rotating credit line that grows as users add more information about themselves. Providing just an ID is enough to get started with a credit line of about $50, but adding employment proof, a pay slip, or other data can increase the limit.

The team has also developed a user-friendly application so that employees can access the salary advances quickly and seamlessly. They no longer have to depend on the interface of a payroll company’s app. With the Advance app, the request takes just 15 seconds and users receive an SMS almost instantaneously informing them that the money is their bank account. This application and the direct access to users it enables was a great advantage for the startup as COVID-related lockdowns have begun and the team has been forced to operate digitally. In fact, even under lockdown, the team has seen significant growth in demand for its product, growing over 100 percent month-on-month since June of this year.

Even as Advance grows its direct sales business, the team continues to pursue partnerships with payroll companies. Today, the mix of salary advance users is 50 percent from payroll companies and 50 percent from direct sales. Even with this diversification, the team is confident they are reaching their target users; 73 percent of their borrowers are first-time borrowers and have zero credit history. Noting that these users are new to formal services the team is now developing additional features for the app to further their financial inclusion, including bill payments, remittances, and bank transfers. They plan to build on the established, trusting relationships they have with employees, to be able to meet more of their financial needs, creating true financial inclusion.

Case studies – Strategy 2

Case 2.1 Entry-level products can build trust and enable cross sell

Lack of trust is often a primary barrier to use so startups looking to increase value need to first grow their users’ trust. Building a suite of products tailored to the segment’s particular needs can help build trust and create opportunities for cross sell. In particular, an “entry level” product that is low risk and low cost can help by allowing users to test the service thereby building trust that can lead to greater lifetime value across other products.

Migrants in the Gulf states are excluded from the local financial system and are forced to use expensive, cumbersome providers to transact, primarily to remit money home and make local purchases. In this environment, NOW Money serves as a payroll provider to local employers, using the channel to acquire migrant workers to provide them a bank account, a debit card, and an app to remit funds home directly, thereby bypassing traditional money transfer companies.

To drive usage of the account and to increase value to migrants, NOW Money’s app has additional offerings like airtime top-ups and salary advances, which cater to the particular needs of migrant workers. Low-value services like airtime top-ups allow NOW Money to build trust in the app, thereby enabling cross sell to higher-value services.

Background

Migrants around the world remit $200 to $300 per year month on average, typically contributing accounting for 650 percent or more of their family’s income. Migrant workers remitted $554 billion to low- and middle- income countries in 2019, yet senders and receivers tend to be excluded from the formal financial system—and COVID-19 now threatens disruptions and reductions. Up to 30 percent of migrants originating from rural areas still use unregulated methods to send and save money.

This problem is particularly pronounced in the Gulf Cooperation Council (GCC) countries, where numbers of migrant workers are outstanding. As of 2019, there were 35 million international migrants in the GCC . In some Gulf states, foreign nationals are an overwhelming proportion of the population: more than 80 percent in Qatar and the United Arab Emirates.

In the UAE, 95 percent of remittances are cash-based, implying exorbitant fees, poor records, and exclusion from other beneficial financial services. As a result, migrant workers sending 40-60 percent of their incomes home, often lose 20 percent of that total on transfer fees. Most don’t have a bank account (perhaps because they feature barriers like minimum salary requirements or other documentation) and instead receive their salaries via one-time-use debit cards. These cards do not serve workers well as they cannot be used for payments or transactions, only withdrawals. Workers need to withdraw the balance in full (at a fee) and then transact in cash, thereby excluding them from a number of financial services and benefits, and exposing them to the risks of carrying cash.

About NOW Money

NOW Money is a banking solution for migrant workers in the UAE that acquires customers by providing payroll services to firms that employ migrant workers. Instead of disbursing their earnings via costly, one-time use cash cards, NOW Money provides workers with a bank account into which their earnings are deposited directly.

The bank accounts decrease administrative costs and effort for employers, and provide a myriad of benefits to workers. For migrants, the bank account allows them to participate in the local digital economy. With the app as a foundation, the company has carefully studied the financial lives of migrants and has rolled out services that match their needs. With the debit card, migrants can withdraw at ATMs and transact at merchants. The app that allows workers to remit home directly from their accounts via partnerships with local banks in their home countries. They can avoid fees and time spent for withdrawals; save on the cost, effort and risk associated with traditional money transfers; and also avoid the costs and risk of receiving cash for their families at the other end. Avoiding lines at remittance houses also serves employers since many reported high rates of absenteeism the day after payday as workers would line up to send the money home.

For employers, switching to NOW Money means they no longer need to pay for cards every payday and can avoid the logistics of disbursing them. Employers also note that NOW Money’s service supports worker retention, a valuable benefit for those employers that hire more skilled, technically-trained migrants.

Weak cross sell to higher-value services

The challenge NOW Money faced is that transaction and payments services are low-margin products, so the startup needed users to use a broad range of products on the app. In particular, NOW Money needed users to remit money via the app since such transfers earned higher margins.

Unfortunately, migrant workers are accustomed to withdrawing all their earnings at once and transacting in cash. NOW Money was finding that few workers would maintain balance in their accounts or use the app’s various features. In June 2019, soon after the app was launched, the team noted that almost half of users were using the app just for withdrawals, while only 24 percent used the card for local translations and only 14 percent for mobile top-ups. Worryingly, only 6 percent were keeping their funds fully digital and fewer than 8 percent of users were using the app’s remittance capabilities, meaning migrants were largely withdrawing the bulk of their earnings to transact and remit in cash.

While most of NOW Money’s revenue growth was coming from acquiring new employers and earning their payroll fees, the team realized they needed to keep users more engaged with the platform to create a defensible business model. They needed users to transact more on the app, to keep their earnings within the digital ecosystem, and to leave money in their accounts.

To understand the barriers to use, the team conducted user research. They found that users of Indian origin, who constituted 65-70 percent of their user base, had extremely low trust in financial service providers and were reluctant to entrust the application with their remittances, both because of the large size and importance of these transactions, but also because of the quantity of personal information for both the sender and receiver the transaction entailed.

They also realized that users were withdrawing in cash to pay off local loans or to loan money to friends within their labor accommodations, who could not accept digital payments. Furthermore, retail outlets in the labor accommodations, where the migrants were making most of their purchases, do not have point of sale devices and must be paid in cash.

Build trust for cross sell

Given these findings, the company made a number of improvements to their offer. Some adjustments improved the user experience, but the key change was to feature mobile top-ups as an entry point to the suite of offerings, thereby providing a first step toward deepening engagement with NOW Money.

A closer look at the data also revealed that users who used mobile top-ups were more likely to try (and to continue using) the remittance services. The team hypothesized that mobile top-ups were serving as a low-cost, low-risk way for users to test the service and establish trust. Given this insight, they ramped up marketing of mobile top-ups via automated SMS marketing campaigns and other channels. This included establishing user segments who were yet to make a mobile top up or a remittance and proactively reaching out to them via SMS and push messaging to encourage the initial low risk transaction as an entry point into remittance and other NOW Money app features. This was backed up by leveraging existing NOW Money users as brand ambassadors on the ground to educate users regarding app features with an aim to build further trust and a sense of familiarity with fellow workmates. Timing of any in app messaging also played a key role in messaging success. Automating messaging upon receipt of salary payment and during user downtime was an important aspect of improving conversion.

Noting the importance of low-risk, low-cost, entry-level products, the team also introduced salary advances as well as local bank transfers (to pay local contacts as well as merchants). They continue to develop such services and are preparing to launch bill payments as well as in-app transfers.

With these efforts, NOW Money has found that over 25 percent (five times) the proportion of users are now fully digital, meaning they never withdraw their earnings. The team believes that UI improvements like adding additional languages (e.g., adding Hindi, Urdu, Malayalam, Arabic, which cover the mother tongues of 90 percent of the user) and simplifying the remittance process explains part of the growth. However, they note that 50 percent of the entire base has now used mobile top-ups, creating an entry point for low-trust users. Whereas only 8 percent of users had used remittances in 2018, double that proportion currently remit via the app. The team has also noted that on average remittance amounts grow 36 percent from the 1st to the 5th remittance as users gain trust in the service. Many start with small transfers and remit greater amounts over time as their trust in the services grow.

In all, the team is focused on staying connected to their users, understanding their needs, and growing their offerings to meet their particular needs. For example, they are growing their remittance partnerships to be able to offer migrant workers more options among receiving institutions and at a lower cost.

Case 2.2 Grow products tailored to your users’ needs

If you know your customer well, you are likely to observe other unmet needs and gaps in their lives. While many startups plan to grow by extending their existing product to new segments, it is worth considering whether to maintain the segment and expand your product lineup to meet more of your existing customers’ needs. This move allows you to leverage the trust you have already built with users and to diversify your risk among various product lines.

Pintek is a lender in Indonesia that started out by extending credit to qualifying families to break lumpy, semester payments into smaller monthly installments. The product grew from Pintek’s realization that the financing needs of schools and their students were not being met by traditional financial service providers. As they got closer to schools and parents, Pintek noticed other opportunities. What started out as short-term loans to parents for tuition now includes direct lending to schools for IT equipment, repairs, assets, and other expenses, as well as short term credit lines for parents across education levels to manage any bills issued by the schools (tuition, books, IT equipment, uniforms etc). Pintek is also launching software products for schools to help them manage better their operations.

Pintek was able to leverage their relationships with schools to broaden their product portfolio into a unique set of offerings, serving the broad, yet particular, financial needs of schools and parents.

Background

The fourth most populous country in Asia, Indonesia struggles to provide high-quality public education to its 267 million citizens. Although the average years of schools have doubled since the 1980s, the number still remains low at only eight years (less than the Philippines and on par with Mexico). Moreover, even among those who complete school, educational attainment is low. The World Bank reports that more than half (55 percent) of Indonesians who complete school are functionally illiterate (compared to only 14 percent in Vietnam). This may be because public education spending as a percentage of GDP has stagnated over the past decade and remains well below the recommended levels. This limited spending also means that capacity as public schools is limited, especially at tertiary levels where public universities often do no have the capacity for the growing number of high school graduates.

In this environment, many families are sending their young people to private schools, particularly for higher education and enrichment via specialized training centers; 57 percent of schools at the lower-secondary level and 70 percent at the upper-secondary level were private as of 2010.

About Pintek

For families turning to these private institutions in tertiary education, making payments can be difficult. Private institutions expect payments twice a year, at the beginning of each semester. This schedule does not match families’ incomes, which tend to be monthly. Noting this mismatch, Pintek developed a product to extend credit to families by acquiring schools. In 2018, they started offering selected families a credit line to break semester payments into monthly installments.

Within the year, the product gained substantial traction, and Pintek was financing 3,000 students across 28 Indonesian provinces, with over 50 percent of users being first-time borrowers. Pintek earned fees from the schools and then incomes from the loans.

Low ceiling for growth

However, the team worried the total addressable market was small, as it was limited to students from schools and training centers that require semesterly payments. They estimated that only 8 million of Indonesia’s 60 million students attend this type of private institution and that only 10 percent of families at any institution would qualify for credit.

Fortunately, the proximity to schools had allowed Pintek to note an additional opportunity to support schools. Insight into schools’ cost and revenue streams revealed that schools themselves needed access to credit that was not currently met by mainstream providers. Financial service providers do not understand schools’ income structures and often they are limited in their options given they are registered as foundations and not-for-profits.

Although schools have regular income streams, those streams rarely match their costs structures. While they typically collect a large sum at the beginning of the school year and then smaller amounts on a monthly basis, they face ongoing costs (e.g., materials and maintenance) and lumpier expenses for larger assets (e.g., IT equipment, facilities and upgrades). As such, unexpected repairs during the middle of the school year can be difficult to manage. Furthermore, rental contracts in Indonesia typically require three years of rental payments upfront so many education institutions need credit to make these payments.

Moreover, school administrators often come from an educational background, rather than a business background. As such, they likely find capital issues beyond their scope and may not have the financial relationships to get the help they need.

Meet more needs

With relationships with schools already established, Pintek was able to add to their suite of product offerings, thereby growing their business with their existing customers.

Given their existing relationships with schools, Pintek was able to observe the schools’ additional needs and tailor a specific line of credit in response. The team found it relatively easy to start underwriting direct loans to schools. For example, when one of their schools needed to pay three years of rent, Pintek stepped in to finance the payment. Since they understood the school’s income flows, issuing them credit directly felt like a natural next step. Although this move shifted Pintek from being just a B2C lender to a B2B lender as well, the team saw the move as an opportunity to meet the needs of their customers, not as a pivot.

These initial loans led Pintek to offer schools to launch both working capital and infrastructure loans. The working capital loans are made against invoices to bridge key payments like repairs for durations up to 12 months. Infrastructure loans for expansions or other asset purchases have slightly longer tenures, between one and three years.

The team notes that they use their insight into invoices to finance more of the schools’ books without increasing their risk dramatically. In addition to the 10 percent of invoices they finance directly with parents, Pintek now finances up to an additional 15 percent of invoice value directly with the schools. These additional funds allow schools—much like the students’ families—to better match their payments schedules with their income streams. For example, paying down three year rental payments in monthly installments. Furthermore, the administration and customer acquisition costs for Pintek are marginal since they are already in these schools and need not invest in additional sales activities.

Just a year after launching the B2B credit, Pintek is now lending to 45 schools. Although lending has slowed with the COVID pandemic, the team is anticipating growth in demand as schools invest in infrastructure like sinks and showers to manage contagion, as well as computers and cameras for online learning. The team is also expanding their sites to include edtech platforms and suppliers that are ramping up under COVID conditions.

In general, the Pintek team is continuously looking for ways to support schools and students. This often goes beyond financial services. For example, Pintek realized that schools needed support getting IT equipment and software to run online learning. In response, the team has started to build a network of distributor companies to support schools as they deploy the loans. Additionally, Pintek is working on launching its own suite of software products to help manage school operations, such as receivable management software expected to launch in Q4 2020.

Looking forward, the team is focused on meeting their user’s needs. They note that students who they financed through secondary school often lack access to financial services as they pursue tertiary education. Since Pintek already knows these students and has existing relationships with them, they are developing products to continue supporting them even after they graduate. The team continues to grow the business by getting to know their users and then growing their offerings to meet those needs via their established, trusted relationships.

Case 2.3 Grow offerings that match users’ needs

In the world of digital and e-services, many providers start with a freemium business model, first building a user base and then finding a way to monetize those relationships over time. Once the base is established, finding the right product for monetization may take several tries. In the case of vulnerable populations, income-smoothing may be a good place to start, since these populations face unpredictable incomes.

In Brazil, micro-entrepreneurs can register as MEIs, allowing them to pay a single monthly tax to obtain benefits like social security and access to financial services. While acquiring and paying for the MEI classification is relatively simple, ongoing compliance with tax payments is low. SmartMEI noticed this opportunity and developed a free tax and accounting app for MEIs. Even as SmartMEI’s active user base grew and the startup added product lines and customer segments, they still struggled to monetize.

Once SmartMEI acquired gig workers, they developed a salary advance product that rapidly increased revenues as well as the proportion of active users. The startup realized that gig workers had earned wages they couldn’t access even as they needed ways to smooth their incomes.

Background

In an effort to address informality, Brazilian authorities created the MEI (Individual Microentrepreneur) category in 2006 to support freelancer and informal enterprises. By registering as an MEI, the entrepreneur pays a single monthly tax to gain a variety of benefits including an operating license, social security coverage, a business bank account, and others.

As of 2019, 8.6 million freelancers and businesses had registered as MEIs, with the numbers of MEIs growing since app drivers can also apply for the classification. However, 54 percent of those registered go on to default on their tax obligations.

These low levels of compliance may not be surprising given the habits of most informal businesses, which typically struggle to maintain records and regular schedules. To avail of the benefits offered by the MEI classification, these entrepreneurs need help calculating their payments and making them in a timely fashion. Unfortunately, most software solutions have been developed for larger enterprises with multiple employees and are too expensive and complex for MEIs. Moreover, MEIs have specific management needs like separating household from business finances and organizing unpredictable expense/revenue structures with varying sources of credit.

About SmartMEI

SmartMEI recognized that these micro-entrepreneurs needed help meeting the requirements of the MEI classification. In response, in 2015, the startup developed an accounting and tax filing application for MEIs. The primary functionality, generating the tax payment amount and making the transfer, was free but users could pay additional fees for billing features so that MEIs could invoice their customers directly from the app. The invoicing functionality was provided for free, but SmartMEI would collect a fee on the payment made by the MEI’s customer.

While the freemium functions attracted a number of users and many were active (46 percent), few were purchasing services within the app (3 percent). In 2017, the team continued to add functionality to the app including deposits and a prepaid debit card to allow MEI owners without bank accounts to more easily send and receive payments. These functions each improved monetization via transaction fees as well as a monthly fee for business insights.

By the end of 2017, the strategy of adding products and functionalities had helped the startup acquire almost 40,000 active users. Unfortunately only 1,200 were paying for services on a regular basis, and marginal revenue on each transaction was extremely thin. The team knew they needed to get users to move more money through the app via more transactions and more types of transactions.

A new segment leads to a winning product

Opportunity came knocking as the platform economy took off in Brazil. Like MEI owners, gig workers needed access to digital payments but lacked bank accounts, so SmartMEI acquired the platforms as customers, creating accounts for their thousands of workers to accept payments. By mid 2018, the startup had acquired four platforms, including Rappi, and counted over 100,000 users. However, as with MEI users, SmartMEI struggled to monetize these accounts since workers would receive their payments and then withdraw the entirety of their earnings immediately.

As they had been doing since the startup’s inception, the team approached the problem by increasing the value proposition of the app. This time, SmartMEI added a salary advance function. They noticed that although gig workers logged more or fewer hours according to their urgent financial needs, they could only access those earnings at the end of the month (or the quincenal). The workers had earned wages waiting for them, but couldn’t access them even for urgent costs like fuel or repairs to their vehicles, which they need to continue working.

The response to the salary advance product was outstanding. For gig workers, it was far cheaper than credit and helped smooth their income, a massive benefit for vulnerable, low-income people. At launch, 60 percent of workers offered the advance took one. Not only was the response high, it was sustained. Once workers experienced the benefits of salary advances, they took them out reliably, at the rate of two advances a month on average. The product was also a winner for SmartMEI because they earned more on advances than they could on simple transactions. The team had finally found a winning product for monetizing their app.

Seeing the initial response, the startup has continued to improve how the advances are offered and featured in the app. For example, a UX adjustment in 2018 reorganized the app’s main menu to more prominently feature the advance and to provide a dashboard view for users to see the extent of their credit line. These improvements pushed the percentage of paying users up from 5 percent in March 2018 to 15 percent in May.

Even as SmartMEI continues to develop additional products — e.g., a professional plan that includes withdrawals and other benefits, and a healthcare plan — the salary advance product continues to account for the bulk of SmartMEI’s revenue. The startup now counts 300,000 users, of which more than half are active and almost 80,000 are paying.

As the startup looks to the future, they are continuing to add functionality to the app and to offer it to more user segments. As a growing percentage of the population in Brazil and the region turns to gig and part-time work, SmartMEI is continuing to find ways to grow their offerings and their business.

Case studies – Strategy 3

Case 3.1 Develop products that meet users’ evolving needs

Products for underserved populations may lose relevance among customers as (or if) they are better able to access mainstream financial services. Rather than depending on the acquisition of new users to drive growth, startups can develop new products that meet their existing users’ evolving financial needs, thereby building on the trust and knowledge they already have with current users.

Self helps Americans with incomplete or damaged credit scores build their credit by giving them a loan to purchase a certificate of deposit (CD). Self then holds the CD, allowing the customer to pay in installments until the loan is paid for in full. At that point, the customer receives the principal back. This credit builder account (CBA) allows customers to improve their credit scores by 32 points on average, while those without scores often see jumps into the 600s. While the CBA product has an NPS score of 93, the credit score jump is only so dramatic the first time.

To continue serving their users after the CBA, Self has designed a secured credit card product, the first step for many consumers toward accessing unsecured credit. This product is the next step in a longer graduation pathway that helps customers improve their damaged credit, build their financial health, and allow the company to serve them over the longer term as their needs evolve.

Background

More than half of Americans have been rejected for a credit card, loan, or car financing due to poor credit. These low scores are driven by people unaware of credit scores and how they work, and as a result have either too many credit cards (38 percent of Americans have three or more credit cards), or none at all (28 percent of Americans between 18-54 don’t have any credit cards). Those with too many cards end up carrying unhealthy credit balances, meanwhile those without any do not have the chance to build up a strong credit score. Nearly 26 million consumers have no credit history, and an additional 19 million are “unscorable” due to insufficient data in the credit bureau. Moreover, in the context of COVID-19, the numbers of people with bad credit are likely to go up as unemployment soars and people struggle to make ends meet.

Once an individual’s credit score has fallen due to a bad loan or excessive credit card debt, it can be very difficult (or some might say it can feel impossible) to improve it. Most advice is to organize the debt, magically acquire superior financial planning and discipline overnight, and slowly pay it off. Of course, all these plans assume no hiccups or emergencies along the way, which is unrealistic for people who have low or irregular incomes. Overall, there are few structured or realistic pathways to help people escape poor or thin credit.

About Self

To improve poor credit scores, people need access to productive credit and to pay off loans in a timely fashion. Payment history represents 35 percent of FICO® scores for consumers. For those who have not developed good financial habits, it can be difficult to secure new debt and to pay it off responsibly.

To give users exactly this chance, Self structures a credit builder loan savings, so as to incentivize and facilitate good repayment. To do so, Self charges customers a $9 activation fee to issue them a $520 or $1,663 loan to buy a one- to two-year CD, allowing them to pay for the CD in installments as it matures (current options can be found on Self’s website). This way, once the loan is repaid, customers are able to receive the CD principal. Knowing that they are working toward earning a lump sum and offering a variety of monthly payment options makes it more likely for customers to pay off the debt, while also having the benefit of improving their credit scores. As they repay the loan, users see their credit score increase by 32 points on average.

While Self’s CBA product has a Net Promoter Score (NPS) of 93, and boasts excellent customer ratings from its nearly one million clients, the startup did not always have a clear path to retention and customer lifetime value. After all, the product’s dramatic credit score bump is not replicable so the marginal benefits for consumers decline with subsequent use (assuming their improvements hold or consumers continue to improve their credit using other tools). That said, enthusiastic clients love the product so much that 15 percent of them take out a credit builder loan a second time. Customers enjoy the “forced savings” aspect of the loan so even though paying the activation fee to save may seem expensive, many utilize the product a second time.

Build a pathway

To address this retention problem, Self is building out a long-term product roadmap that allows the company to support its customers as their financial health evolves over time. Since Self already knows these users and has built trust with them, the startup is adding products to meet users’ maturing needs rather than lose them to other providers.

As a first step, the company has launched a new product that grows its business as its customers grow — a secured credit card that doesn’t require an upfront deposit. Once customers meet Self’s eligibility requirements, they are able to access the liquidity they have built up in their CBA through the use of a secured credit card, instead of having to wait until the end of the CBA loan tenure. For example, if a client meets the eligibility requirement and has made $200 in savings progress, they can access a secured credit card of up to $200. To date, customers have found the credit card proposition quite appealing, with many CBA users opening a secured credit card with the company.