People

Regions

Topics

- Access Usage Gap

- Challenges and Crises

- Consumer Protection

- Credit

- Digital Financial Services

- Enabling Environment

- Fintech

- Insurance

- Partnerships

- Responsible Digital Finance

- Underserved Groups

Company

Thank you to our partners, Swiss Capacity Building Facility and SOCREMO Microbanco S.A.

Executive summary

In Mozambique — as in other parts of the world — microentrepreneurship is an especially risky endeavor. It is fraught with high-impact, disruptive economic events, with few mitigation or management tools available to those affected. Income is often unstable, making it challenging for entrepreneurs to save much money. Normal life events — from births to weddings to funerals — can have major implications for the microentrepreneur. For example, when a family member dies, the family is required to cover the costs of the funeral and hosting the extended family. As a result, many people get into significant debt and become unable to continue with their businesses.

Without adequate savings, access to capital, or other financial means to absorb these costs, many microentrepreneurs find themselves sinking deeper into a financial crisis. While many insurance companies have introduced voluntary products in the Mozambique market, the uptake has been low and many clients have missed payments, resulting in lapsed policies. Culturally, insurance policies are also viewed as a product for the elite among low-income earners and microentrepreneurs, who do not see it as a suitable product for them.

To address some of the gaps in existing offerings, the new product must offer customers significant coverage, convenience, and other benefits, all while incentivizing savings behavior for the long-term.

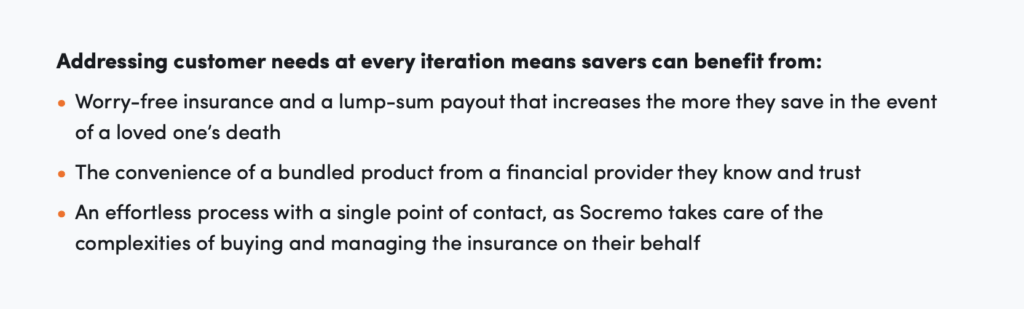

Bundled or composite products afford an organization the opportunity to offer convenience and cost savings to low-income customers. Having identified funeral coverage as a key need of its customers, Socremo, a leading microfinance bank based in Maputo, Mozambique, first partnered with Hollard Insurance to provide funeral benefits to existing customers of its loan products. With time, Socremo partnered with Hollard again to extend this benefit to its savings account holders. The funeral benefit attached to the savings product features a “balance multiplier,” which credits customers double the amount of their latest savings account balance in the event of death of the customer.

Over a two-year period and with support from the Swiss Capacity Building Facility, Accion used human-centered design to help Socremo improve its savings product to include this savings account balance multiplier benefit, which is paid out by the insurer. During the project, there were several iterations to cater to the needs of customers, increase uptake, and incentivize staff to sell the product. These iterations helped define a value proposition that aligns with customer needs and expands product delivery channels.

Partnerships play an important role in delivering tailor-made products that meet the needs of customers. Strong partnerships help parties leverage their strengths and experiences; this was demonstrated through Socremo’s collaboration with leading Mozambique insurer Hollard. Socremo’s deep understanding of low-income customers and Hollard’s expertise in insurance complemented each other well throughout the product’s development and deployment.

Ultimately, the various iterations and improvements resulted in a 60 percent increase in the savings product’s uptake and usage; however, the undertaking did not come without challenges. An initially weak value proposition, consumer protection issues, and regulatory and social norms were key barriers to adoption. Enablers such as awareness, financial literacy, and the use of digital tools for onboarding helped in removing these barriers, leading to increased adoption. The increase in adoption is clear proof that financial service providers have an important role to play in supporting consumers by investing in the right infrastructure, researching customer needs, and leveraging partnerships.

Small business owner, Maputo, Baixa marketThe funeral policy product from Socremo gives me and my family peace of mind if there is a calamity and I am unable to service my loan or access my savings. It allows the family to be able to deal with the funeral and burial expenses which are usually a burden to families mourning a loved one. It is what has helped to keep me going with my business with hope.

Introduction

Why a bundled product with a funeral benefit?

Funerals are a major life event and are culturally significant in sub-Saharan Africa. Mozambican communities make funerals societal affairs and thus they carry additional costs beyond the money spent on coffins and burial-related activities. Funerals may last for several days, with community members gathering to console the bereaved families, who bear the costs of hosting. These costs have negative effects on immediate family members post-burial, as family savings can be depleted from organizing funerals. Micro and small business owners who do not have enough savings are forced to draw down on money from their businesses, affecting their long-term financial health. There are informal and well-established mechanisms such as funeral associations, community groups, and church welfare groups that may provide support, but in most instances, these mechanisms are inadequate. This is where funeral insurance becomes critical.

There are various insurers offering funeral insurance, but uptake is very slow due to the sensitive nature of issues around death, limited distribution channels, lack of an understanding of the targeted market, and the negative perception of insurers when it comes to claims. After two decades of working with low-income clients, Socremo has a deep understanding of their customer base. With Accion’s support, the organization partnered with a leading insurance provider in Mozambique, Hollard Insurance, to provide funeral insurance as a bundled product to be combined with Socremo’s existing savings product called Vitamina. This partnership provides Socremo the opportunity to add value through an existing, well-known product and meet the needs of its customers. It also helps Hollard reach a segment of the market it would not typically reach due to misconceptions about insurance as something only for the affluent.

Additionally, the fact that customers do not have to contact Hollard, and that Socremo handles all the paperwork and premium payments, makes for an easier, more seamless customer experience. As an organization that puts customers at the center of all its actions, Socremo’s decision to introduce this insurance product as a bundled product was influenced by direct engagements with customers.

Funerals are societal affairs, and any benefit that reduces the burden on the family is highly regarded. Socremo designed a savings product with funeral insurance for its clients. The value proposition: a balance multiplier, easy premium payments, no customer input required, and increased benefits with increased savings.

Product design journey and prototyping for savers

What is Vitamina?

Vitamina is a savings product that has the basic features of an ordinary savings product but with added benefits, such as bundled funeral insurance benefits and accompanying digital tools for product onboarding and utilization. This product is a voluntary product available to micro and small business owners who have an existing loan or who wish to only save with Socremo. Product enrollment is done via the loan officer, the branch network, or mobile application.

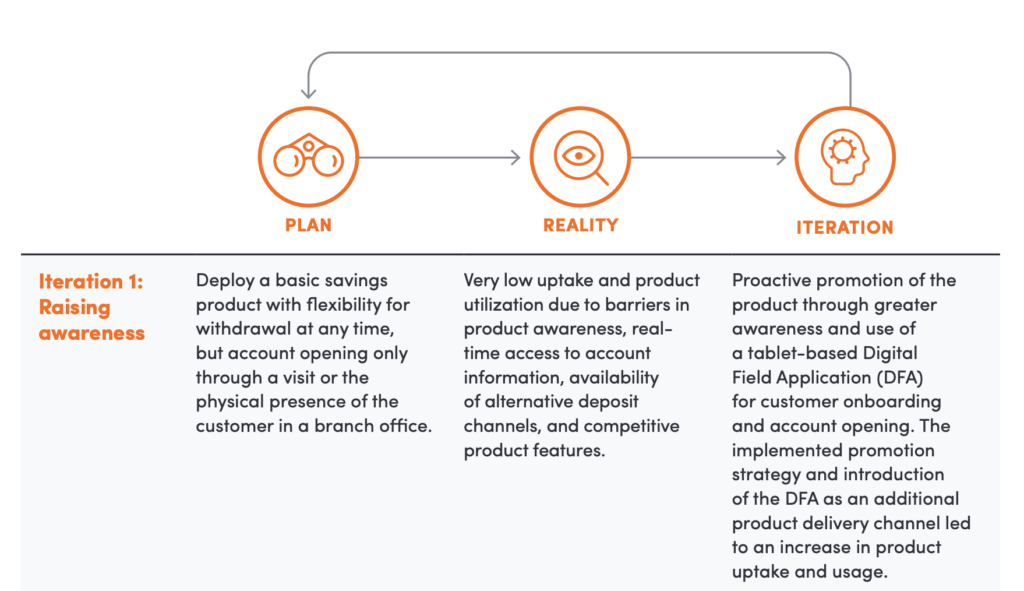

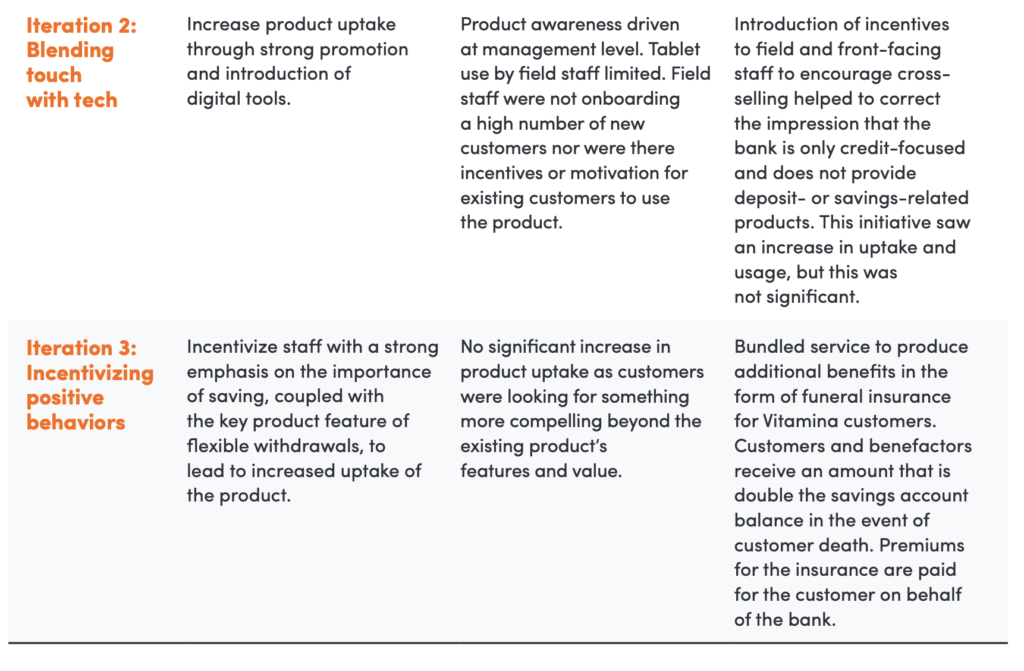

Iterating Vitamina

From its inception, Vitamina was conceived to be a savings product with very basic features, delivered like any other competing savings product. A product review exercise revealed a rather weak uptake and low product utilization, inspiring several recent iterations, which ultimately led to the current product. Human-centered design principles — spending time with clients in their real environment, following the client’s leads and needs, thinking about the whole customer journey around the product, prototyping and testing the product, and small and simple interventions — influenced the product iteration at each major stage.

The final product has the following features, including its key value proposition that in the event of death, double the savings balance is paid out:

- Voluntary savings

- M1,000 (US$16) minimum balance to qualify

- Socremo deducts the M1.76 (US$0.03) per M1,000 (US$16) premium cover from the interest paid monthly into the account, paying the insurer directly on behalf of the client

- Interest paid at 7 percent per year, above the average market rates between 4 to 5 percent per year

In the event of a valid claim, the benefit amount (which is double the savings account balance) will be paid to (in order):

- The Socremo savings account holder

- The nominated beneficiary

- The estate of the deceased

Distribution and payment channels:

- Branch network

- M-PESA wallet integration

- Socremo mobile app

- Staff field tablet application (DFA)

The benefits to Socremo include:

- Increase in number of savers

- Deposit mobilization

- Microinsurance inclusion

- Transaction income (as a collection agent for the insurer)

- Customer retention and stickiness

Growing an existing partnership

Socremo and Hollard first introduced credit-life microinsurance in Mozambique in 2014 through Socremo-funded credits (loans) to protect the client and the client’s family. Socremo administers the credit-life insurance in partnership with Hollard, and is responsible for distributing the product, collecting premiums, and paying the benefit amount directly to customers in case of death. This credit-life insurance is available for the duration of the loan facility and has been quite successful and impactful over the years.

Building on the success of the credit-life insurance and to address the challenges that clients have with funeral expenses, Socremo and Hollard introduced a funeral benefit that is available to credit clients (during the lifetime of the loan facility) and Vitamina clients (driven by the saving balance). This new benefit:

- Guarantees a dignified funeral for customers and their dependents.

- Allows, in case of loss of life of the customer themself, for the family to avoid seeking funds for the funeral and repayment of credit, as well as giving up household goods for credit reimbursement.

- Helps reduce the incidence of customers taking money from their business to defray funeral expenses and thus a negative impact on the growth of the business.

- Helps prevent a situation where a customer has to sell family property to finance funeral expenditures.

Growth of the Vitamina product

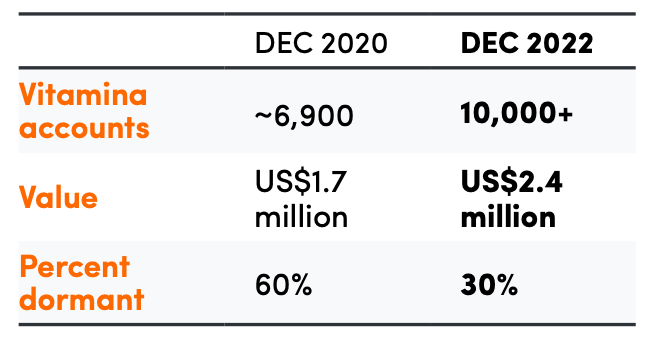

Through its various iterations, the Vitamina product has grown by over 60 percent since 2020, from 6,400 clients early in the year and after a regulatory determination in 2021 that called for the compulsory closure of accounts without adequate KYC. Socremo has also managed to mobilize deposits above US$2.4 million, with an average balance of US$235, by improving the value proposition of the Vitamina product.

Partnerships and long-term relationships with established players help with product design, go-to-market strategy, administration, and client retention. Socremo benefited from bundling microinsurance with its loan and savings products. By building on the experiences learned with lending customers, Socremo has been able to leverage the existing partnership with Hollard to extend this benefit to savings customers and increase customer stickiness.

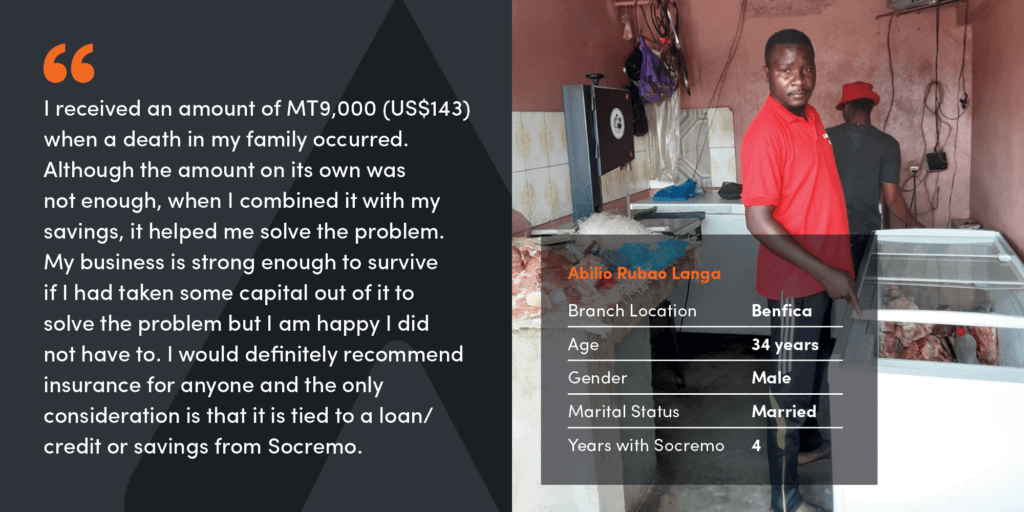

Client Testimonial: Abilio Rubao Langa

Vitamina: Implementation challenges

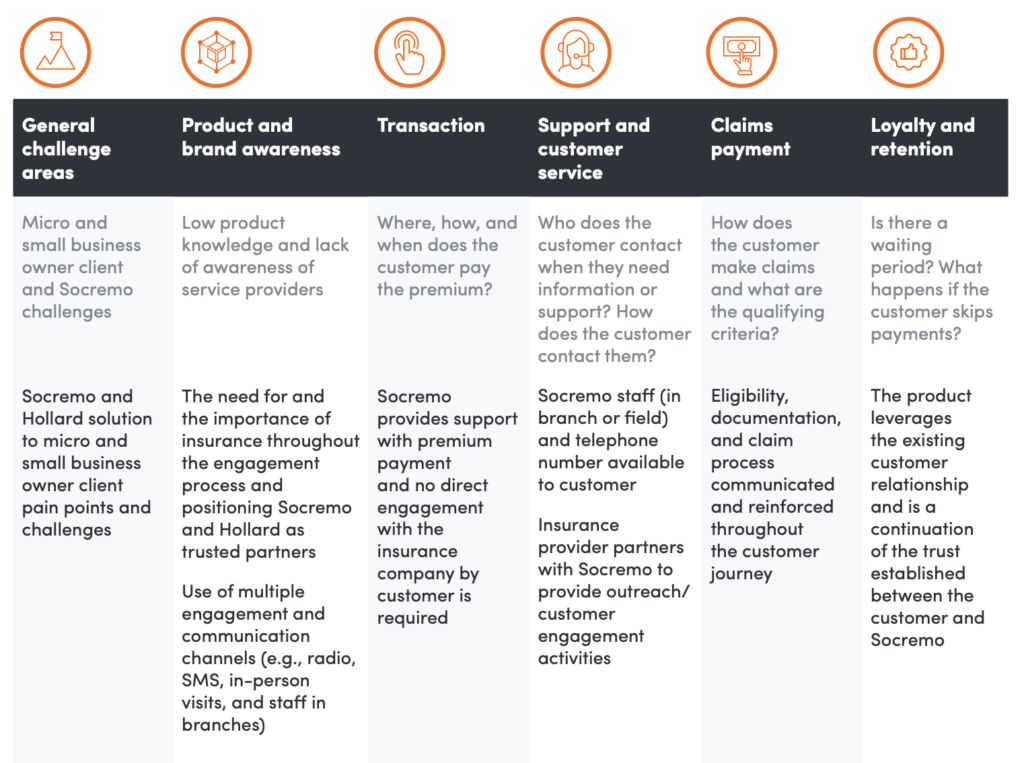

The challenges to adopting and using microinsurance products encountered in similar markets are also present in Mozambique. Throughout the implementation process, Socremo, Accion, and Hollard worked together to understand customer struggles, reduce friction points, and increase awareness of the customer target market. Involving field staff who have built long-term relationships with clients was important as trust is key; leaning on them to communicate the product offering made the process simpler and more consistent. The customers’ loyalty to field staff and Socremo also helped with adoption. After carefully considering key customer pain points, which were common to both the existing loan customers without savings accounts and the new savings customers being targeted, the team managed to overcome each challenge area as highlighted below.

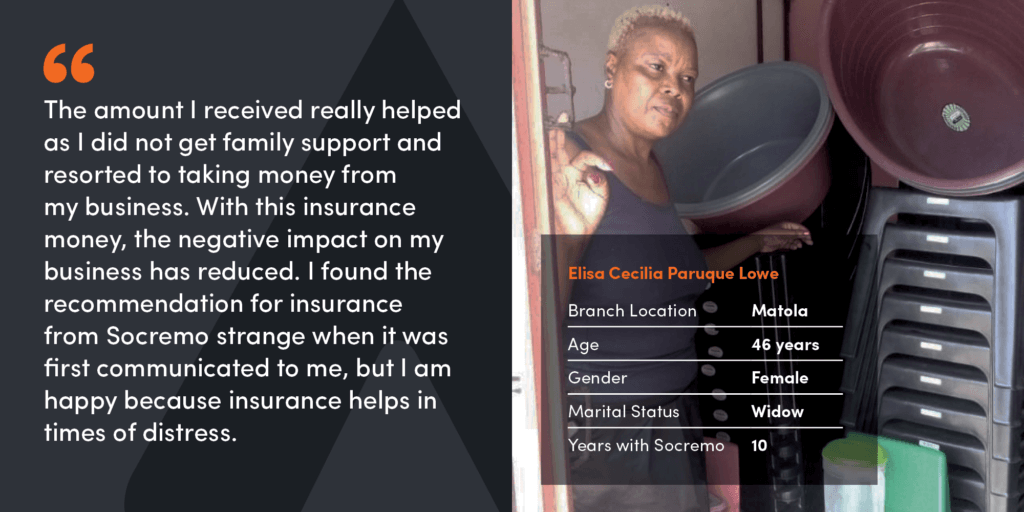

Client Testimonial: Elisa Cecilia Paruque Lowe

Vitamina: Adoption challenges

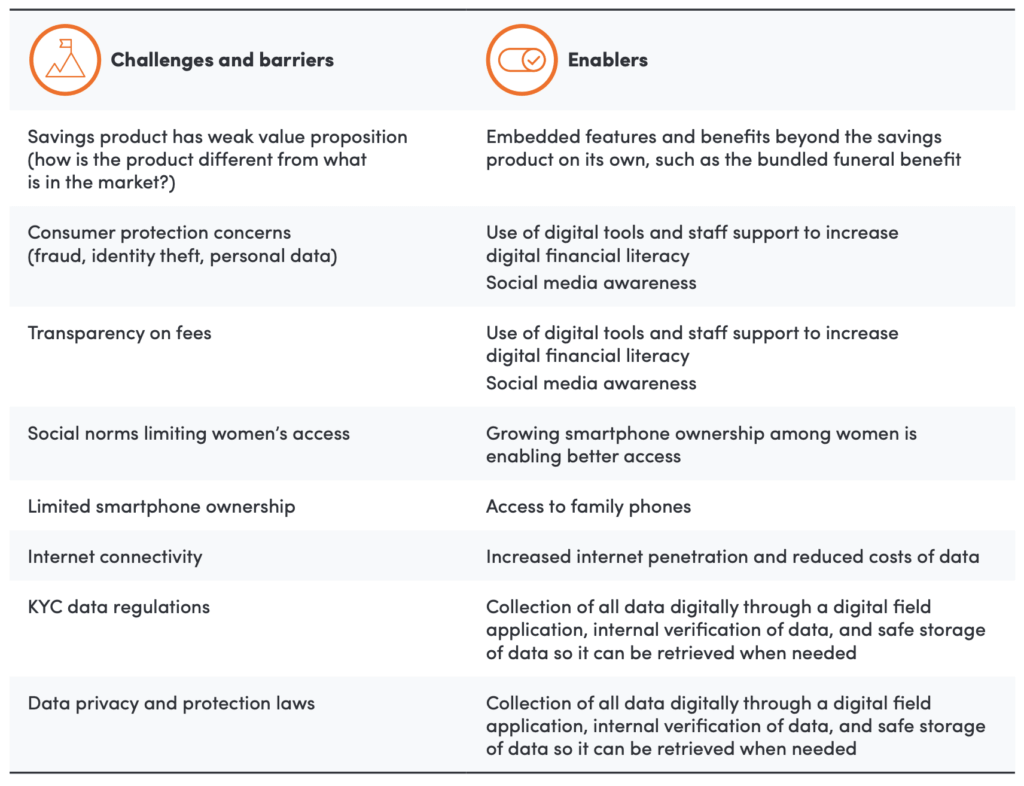

Barriers and enablers to adoption

Socremo had to undergo numerous iterations of the savings product Vitamina, due to low adoption and conversion rates. Some of the barriers and enablers employed over the two-year project period were as follows:

Results from the project show that institutional capabilities and capacity can drive the adoption of microinsurance for micro and small businesses through focused research, investments in digital infrastructure, partnerships, and digital literacy tools.

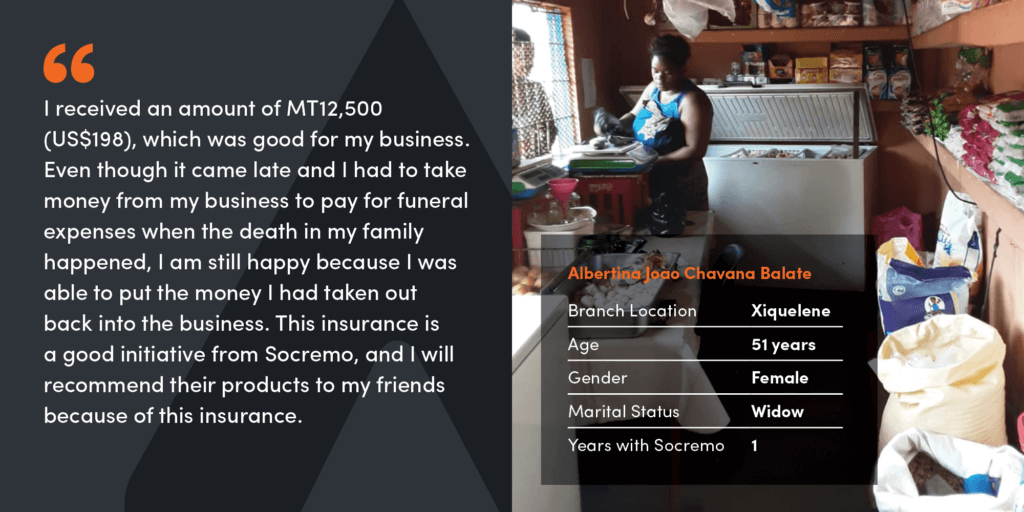

Client Testimonial: Albertina Joao Chavana Balate

Conclusions and recommendations

Socremo has been able to design and develop an inclusive microinsurance product to increase their number of clients by 60 percent, create new revenue streams, retain customers, and cross-sell this new product to existing clients.

From this experience, we have learned that:

- The value of accepting microinsurance for small businesses must be tied to an anchor product. Accepting microinsurance brings a greater value proposition that leads to the expansion of customers, increased customer spending, improved business management, better insight into revenue and income, ease of access to financial accounts, and increased safety, as well as keeping up with customer preference.

- Partnering with microinsurance facilitators is driving inclusion by reaching people and business owners who were not clients before. Growth can be driven by new businesses through lead generation from non-traditional microfinance clients. Positioning the bank in the market beyond credit can attract women-owned businesses that may be using informal microinsurance products like burial societies.

- Digital infrastructure helps with customer onboarding and data collection. The lead conversion rate can be improved with digital infrastructure that allows for seamless customer acquisition and strategic use of data. Staff-assisted and self-service models like the Socremo mobile app provide customers greater flexibility and payment options.

- Payment acceptance supports growth. Digitally enabling financial service providers and automating systems, from onboarding to payment systems, helps micro and small business owners make claims and receive payments for claims.

For other financial service providers that intend to follow suit, these are some of the key considerations that should be examined and acted on:

- Reliable and easy-to-use technology must be incorporated to increase awareness for small business owners. Products such as microinsurance do not need complex technology; by continuously making small changes and interventions, financial service providers can continue to bolster adoption, use, and promotion.

- Investing in research to better understand clients and their needs is critical. Market research on existing and new clients can improve the understanding of why, how, and under what conditions various segments of micro and small businesses adopt and benefit from certain products. Testing products with existing clients allows a better understanding of the pain points and needs. Socremo made use of branch champions to solicit feedback faster and make adjustments.

- Partnerships can complement your existing product. Financial service providers can set up partnership frameworks to foster product design, innovation, implementation, support, and client retention. Partnerships require new competencies to manage the new business model and also to support clients who are not typical financial service provider clients.

Acknowledgment

This report was authored by a team led by Gift Mahubo, Kwashie Agbitor, Gildo Daniel, and Wellington Chinanzvavana. This report was authored by a team led by Gift Mahubo, Kwashie Agbitor, Gildo Daniel, and Wellington Chinanzvavana.

This project and report were implemented and produced with support from the Swiss Capacity Building Facility (SCBF), an innovative public-private platform to enhance inclusive finance for low-income clients, especially women, smallholder farmers, and micro, small, and medium enterprises in emerging contexts. SCBF enables financial service providers to access the expertise required to develop and scale innovative solutions that address the unique challenges these clients face. So far, SCBF has co-funded over 169 projects across 48 countries, reaching over 2.9 million people with financial services that improve their living standards, build resilience, and advance economic empowerment. Connect with SCBF at www.scbf.ch or tag @SCBF on LinkedIn.

We would like to thank the team at Socremo for working with us on this project and sharing their learnings and expertise.

We also thank Hollard Insurance for their partnership in providing inclusive microinsurance products to micro and small businesses.

We are also grateful to Boaventura Chicuele and Sabino Esteira for their valuable inputs, insights, and contributions.

Cover photo credit: Palomisa Schavelle, beverage business owner, Shapow, Mozambique

Explore More