This report aims to consolidate lessons learned from a program implemented by Accion with support from Caribou and Mastercard Strive to digitize micro and small enterprises (MSEs) in Central Asia, with a focus on Kazakhstan and Uzbekistan. It examines the key enablers and barriers to digital adoption and financial inclusion, particularly in areas such as digital payment acceptance and access to embedded finance. Additionally, the report underscores the critical role of partnerships and inclusive solution design in reaching women-led and rural businesses, ensuring that these segments benefit from the region’s evolving digital ecosystem.

Authors

This report was written by Brian Kuwik with contributions from Nvard Gharakhanyan and Nail Almukhambetov.

Acknowledgements

The authors would like to thank the teams at Beksarand MayaSoftfor their collaboration on this program.

About Caribou

Caribouis a global consultancy working with ambitious foundations, companies, and governments to accelerate and deliver impact in a digital age. We apply deep technical expertise and rigor to fund and program management, strategy and policy design, impact measurement, actionable research, and immersive learning initiatives. We work towards a world in which digital economies are inclusive and sustainable, driven by secure livelihoods, innovative business models, and resilience to a changing climate. Follow on LinkedInand subscribe to the newsletter.

About Mastercard Strive

Mastercard Striveis a portfolio of philanthropic programs supported by the Mastercard Center for Inclusive Growthand funded by the Mastercard Impact Fund. From 2021 through 2024, Mastercard Strive reached 19 million small businesses across more than 30 countries, helping them go digital, get capital, and access networks and know-how. Follow Mastercard Strive on LinkedInand subscribeto its newsletter.

Executive summary

Kazakhstan and Uzbekistan are important markets in Central Asia for demonstrating the benefits of digitization and embedded finance for MSEs and for providing relevant insights for other emerging markets. The ecosystem for digital business solutions (DBS) and financial services for MSEs in the region has been quite dynamic over the past three years. Yet, MSEs have not been a priority segment for many of these new digital offerings. From 2022 to 2025, Accion implemented a project in partnership with Mastercard Strive to digitize MSEs in Kazakhstan and Uzbekistan, in collaboration with local DBS providers Beksar and MayaSoft. By connecting Beksar and MayaSoft’s MSE customers to digital tools and opportunities to access capital, the project sought to strengthen their resilience and accelerate their growth, particularly among women-led enterprises.

The shared project objectives were to:

Promote the digital transformation of MSEs.

Enhance data analytics by MayaSoft and Beksar.

Introduce segmentation scoring of MSEs.

Incorporate embedded finance into their business models.

To achieve these objectives, Accion supported enhancements to Beksar’s retail technology platform and MayaSoft’s smartphone-based point-of-sale system to drive greater adoption and sustained use by MSEs.

During the project, Accion, Beksar, and MayaSoft identified the following key insights:

Expanding the outreach of digital business solutions to MSEs requires an enhanced and holistic value proposition and targeted marketing by segment.

Enablers and barriers to digital business solution adoption among MSEs are driven primarily by solution design and existing infrastructure.

Partnerships and collaboration opportunities to offer embedded finance to MSEs can be challenging in emerging contexts, but opportunities are taking shape.

Transaction and sales data analysis generates predictive segmentation scoring models to enhance MSE lending and reduce churn.

One-size-fits-all digital business solutions fail to engage diverse MSE segments and increase churn.

Women-led MSEs represent the strongest untapped potential for digital solution uptake and growth in the region.

Rural MSEs face more constraints in using digital business solutions regularly.

Digital access does not guarantee financial empowerment.

Based on these insights and the project outcomes, we present targeted recommendations for the key stakeholders shaping the digital ecosystem for MSE solutions and financial services. It will take a collective effort from all stakeholders to continue raising digital adoption and deliver meaningful impact on MSEs in the region, and these recommendations can guide the way forward:

Embedded finance is an important opportunity that is currently limited in Central Asia to e-commerce platforms developed or owned by banks. Other platforms focused on serving MSEs could be leveraged more effectively, and partnerships between banks, microfinance organizations, and DBS providers can test data-driven lending models in addition to services tailored to the realities of women entrepreneurs.

Data collection and analytics are a key part of scalable and sustainable business models. It is important to build internal capacity within these companies at an early stage, so that digital solutions for MSEs are strongly linked to real business outcomes. Fintechs and DBS providers seeking to reach MSEs can design their apps to function in low-connectivity environments and extend proven solutions to other markets in the region, particularly where MSEs have more limited resources and capacity to invest in digital business tools.

More space is needed within the digital financial services ecosystem to encourage innovation and collaboration. Measures to improve consumer protection and public trust in digital financial services are advantageous, such as investing in enhancing internet connectivity in rural areas, particularly where MSEs are concentrated. Further, governments can encourage the region’s universities to enhance education in statistics, new data analytical methods and tools, and related skills to help reduce gaps.

A bolder approach to funding regional innovation is encouraged. Capital is most effective when paired with mentoring, and investor-readiness training is key to enabling product scaling. Longer-term financing would enable innovative firms to strengthen their offerings and achieve sustainability beyond the pilot phase.

A view of Registan Square in Samarkand, Uzbekistan. Courtesy of Mastercard Strive.

Introduction

In the past decade, micro and small enterprises (MSEs) in Central Asia have been able to take advantage of new opportunities enabled by economic reforms in Kazakhstan and Uzbekistan. These two key middle-income markets have a combined population of 60 million people and 4.2 million active MSEs (excluding the agricultural sector) and are important bellwethers of regional progress. Together, they represent the two leading e-commerce markets in the region with a combined market size of US$3.7 billion.

MSEs comprise more than 95 percent of all businesses and are important contributors to economic production and employment. While many are informal in nature, MSEs generate high levels of employment, as much as 75 percent of the total number of jobs in Uzbekistan. In this context, Kazakhstan and Uzbekistan are important markets in Central Asia for demonstrating the benefits of digitization and embedded finance for MSEs, as well as providing relevant insights for other emerging markets.

The digital landscape for small businesses in Kazakhstan and Uzbekistan

The ecosystem for digital business solutions (DBS) and financial services for MSEs in the region has been quite dynamic over the past three years. New products and services have come to market. E-commerce has grown significantly. Yet, MSEs have not been a priority segment for many of these new digital offerings. Several key players indicated that they had invested significantly in capacity-building for small merchants to address gaps in digital literacy.

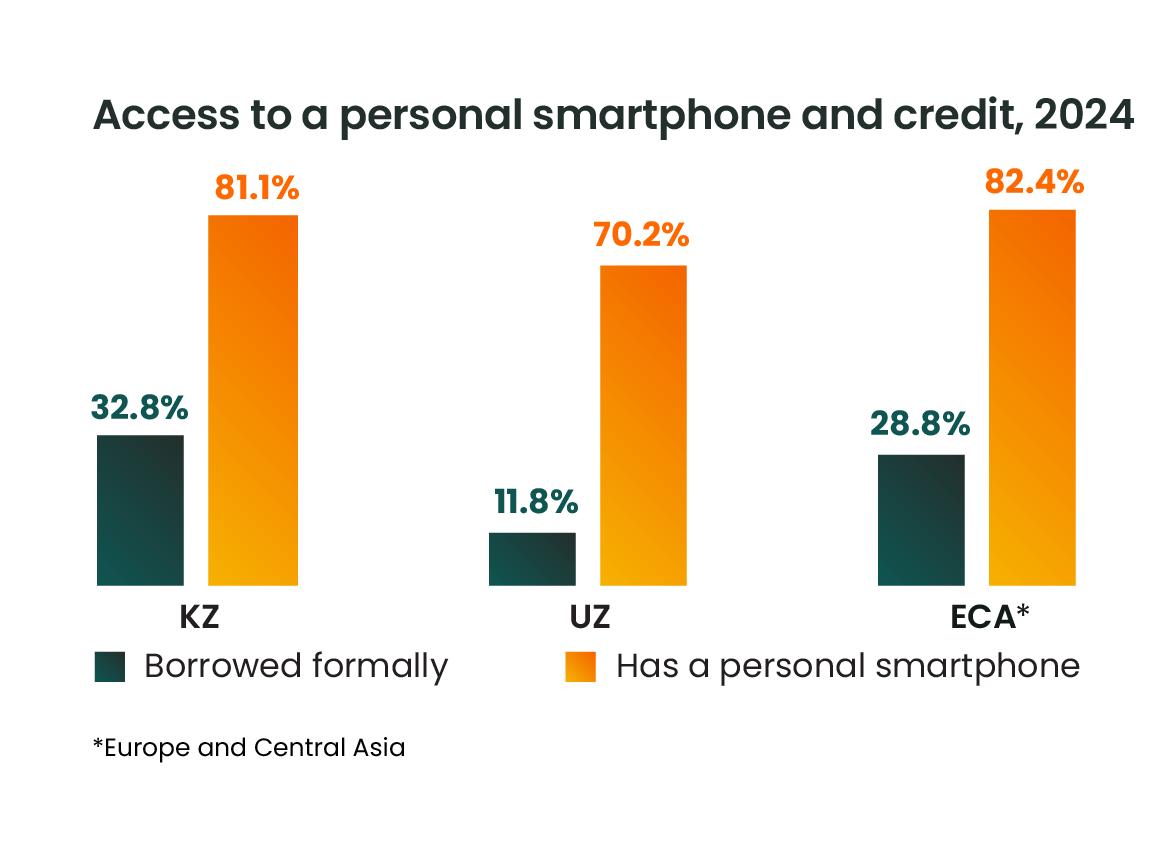

In Kazakhstan, smartphone and internet use among the general population is relatively high at 81 percent and 95 percent, respectively. In Uzbekistan, smartphone penetration reached 70 percent in 2024. These penetration rates have driven increased adoption in digital financial services. Many access the internet only on their phones. In rural areas of both countries, many cite inconsistent connectivity as an issue.

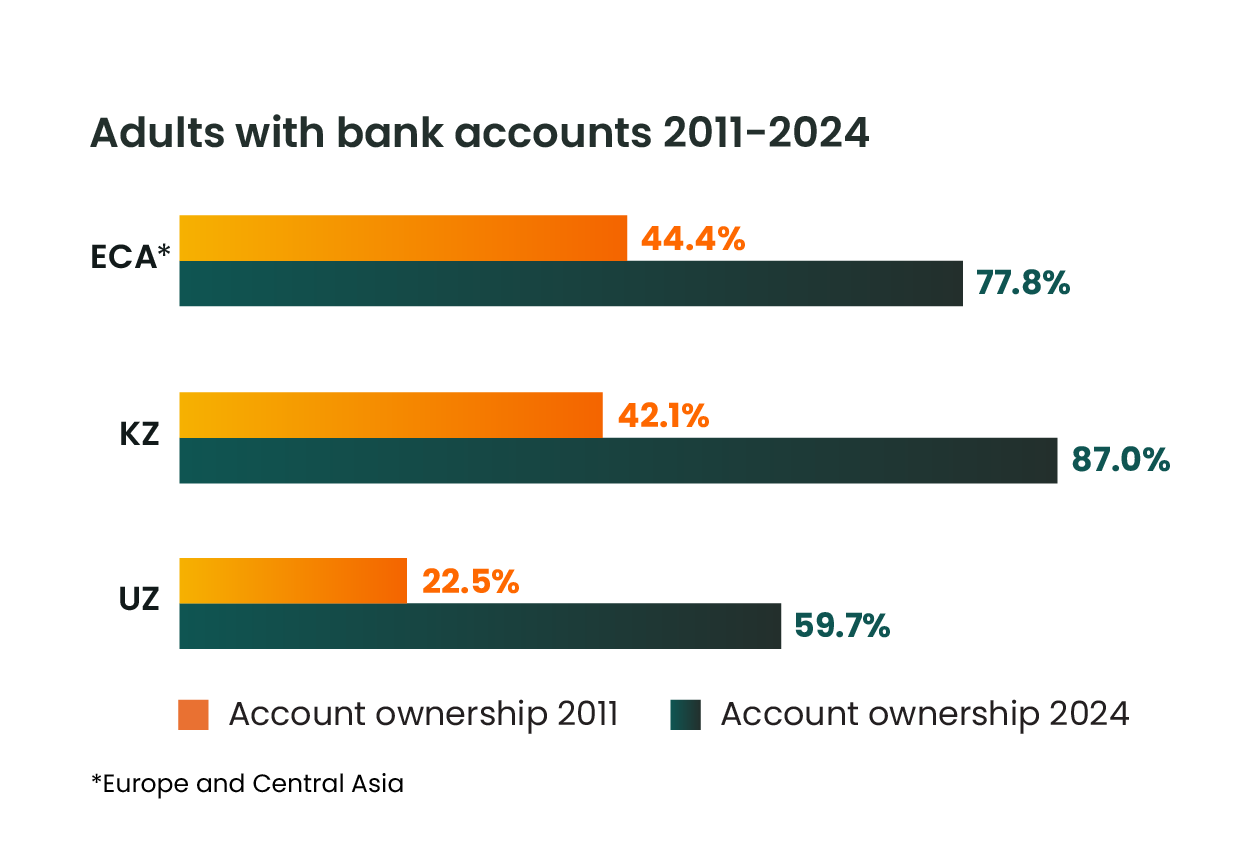

In 2024, 87 percent of Kazakh adults had a bank account, up from 42 percent in 2011, indicating rising confidence in banks. A similar increase in bank accounts has emerged in Uzbekistan, where 60 percent of adults have a bank account, compared to 22.5 percent in 2011.

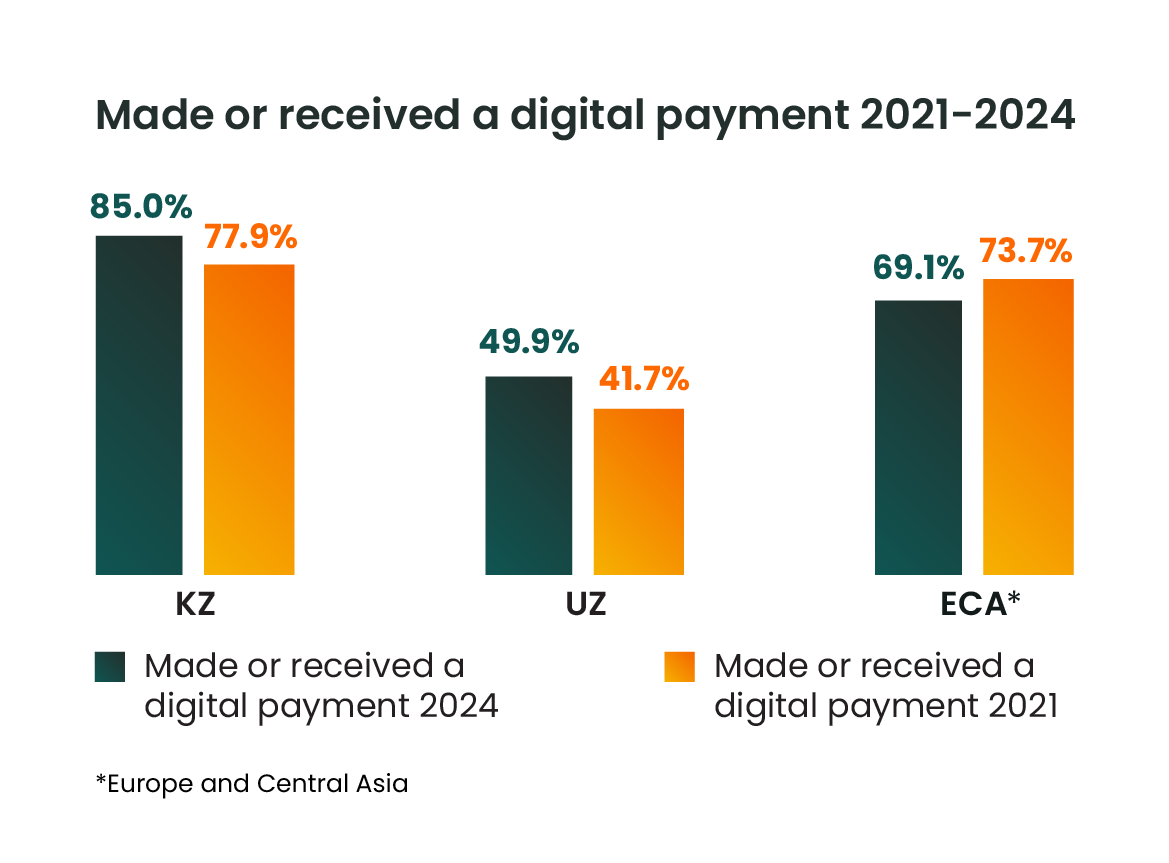

Digital payments usage has increased in both countries, with Kazakhstan even outpacing the region. Uzbekistan still relies significantly on cash for transactions.

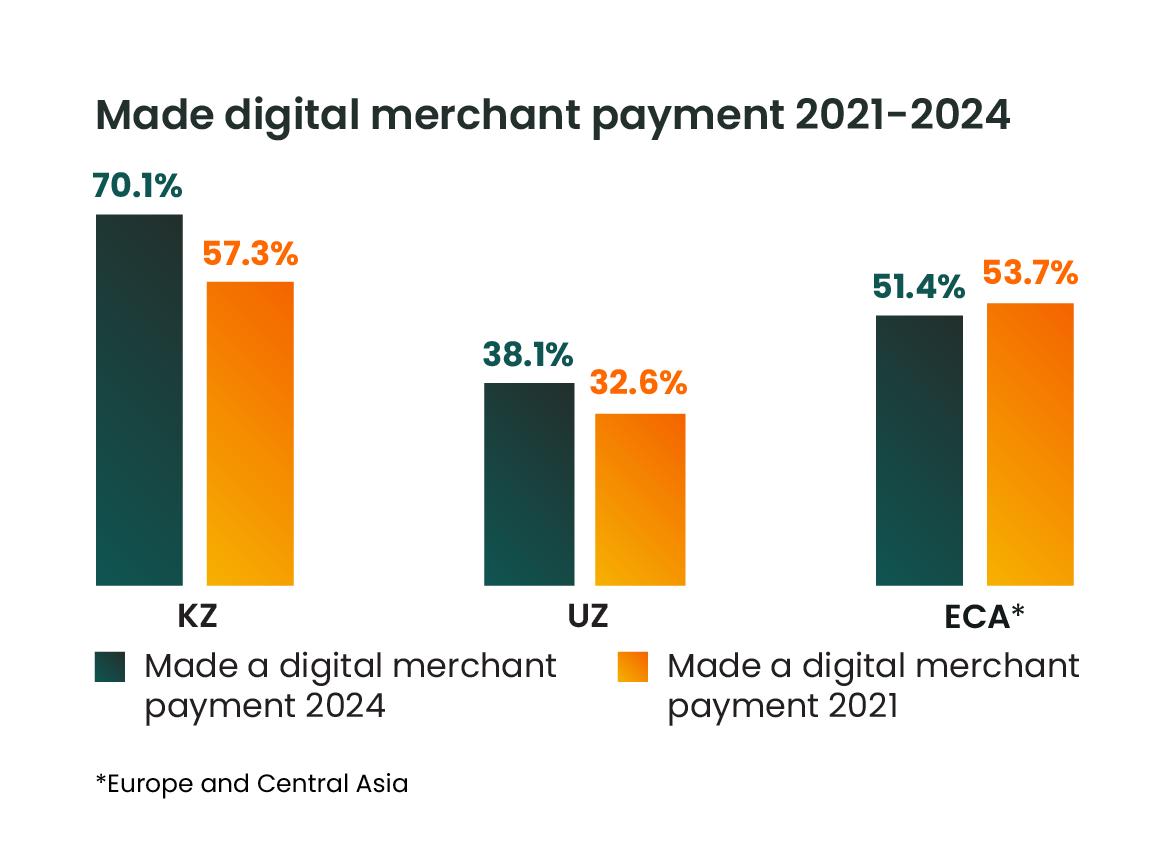

Digital payments to merchants have become commonplace in Kazakhstan, with more than 70 percent of adults making them. While digital payment usage is increasing, the two countries are moving at different speeds.

About one-third of the population in Kazakhstan and 12 percent of Uzbeks have accessed formal credit from banks and microfinance organizations.

KAZAKHSTAN MARKET FEATURES

High financial inclusion in terms of digital payments and accounts.

Presence of Kaspi.kz, a super app with significant scale.

Flourishing e-commerce ecosystem.

Microfinance industry plays a key role to ensure MSE lending.

Government provides wholesale financing to some private FSPs for MSE lending.

UZBEKISTAN MARKET FEATURES

MSE economy remains dominated by cash.

Peer-to-peer (P2P) wallets are the main digital payment players.

Emerging e-commerce ecosystem.

FSPs exhibit strong aversion to MSE lending through embedded finance in platforms.

Low level of access to commercial MSE credit.

Government intervention in MSE finance with subsidized loans through its own banks.

Registan Square, Samarkand, Uzbekistan. Courtesy of Mastercard Strive.

Innovating for inclusion with MayaSoft and Beksar

Most MSEs in Kazakhstan and Uzbekistan still rely on cash and have narrow digital footprints, underscoring the opportunity for digital business solutions.

From 2022 to 2025, Accion implemented the Mastercard Strive project to digitize MSEs in Kazakhstan and Uzbekistan. The program consisted of two phases: an initial research and concept design phase, followed by a second phase for partnership development and solution implementation.

During the initial phase, both markets offered a range of digital solutions and financial services for MSEs, particularly in Kazakhstan, where nearly 78 percent of adults had already used digital payments in 2021.

Accion also conducted digital maturity surveys with local financial institutions, which indicated relatively high levels of digital literacy and use by these banked MSEs. However, most MSEs remain unbanked or financially excluded. Many continue to operate primarily in cash or through peer-to-peer (P2P) wallet payments. They do not use digital accounting or point-of-sale (POS) systems. Their digital footprint remains narrow.

After extensive consultations with a wide range of stakeholders, FSPs, fintechs, and technology companies, we selected two DBS providers that each had a sizable reach, serving several thousand clients, and focused on MSE segments rather than medium-sized or larger enterprises.

MayaSoft

MayaSoft’s MARTA SoftPOS solution

MayaSoft, a licensed payment organization in Uzbekistan, is dedicated to developing, integrating, and implementing cutting-edge contactless payment technologies. With a clear mission to serve unbanked and underserved small merchants, its primary objective is to bolster the payment acceptance infrastructure for MSEs while actively promoting the adoption of fast, secure, and cashless payments among cardholders.

The Uzbekistan POS market lacks affordable, all-inclusive solutions that enable MSEs to manage retail sales efficiently. A POS terminal can cost up to US$300 and may require a monthly subscription payment. To address this gap, MayaSoft introduced the MARTA solution, which accepts all card types without hardware costs or subscription fees. It also offers near-instant merchant settlement, appealing to entrepreneurs seeking immediate access to transaction proceeds.

MayaSoft successfully launched its flagship SoftPOS product in Uzbekistan in 2021. The MARTA SoftPOS is a payment application that transforms an ordinary NFC-enabled Android smartphone into a full-fledged POS solution for accepting all major payment cards and their alternatives. Drawing on its experience and lessons learned, the company aimed to address the changing needs of MSEs with a new version of the MARTA SoftPOS solution released in November 2024.

During the 10-month project, MayaSoft grew its active MARTA user base from 4,000 to more than 14,000, the largest growth in active users since the solution’s launch in 2021, and demonstrating the strong performance of its latest version among MSEs.

Beksar

Beksar’s retail tech solution

Beksar, a DBS startup headquartered in Kazakhstan, specializes in retail automation solutions. With a 50 percent annual growth rate, the company serves over 4,000 active online and offline retailers, providing proprietary software that optimizes operations and enhances efficiency. Its franchising network includes over 35 partners, demonstrating its capacity to deliver scalable solutions tailored to market needs.

Beksar’s retail tech solution for MSEs includes sales, analytics, inventory management, loyalty systems, and other services. Users can obtain real-time data on business performance and conduct controls remotely at any time. They can also use the Beksar solution for digital marketing and sending promotions. With automation, they can optimize their processes, especially inventory control.

The project aimed to increase small business adoption of the Beksar solution by improving customer segmentation based on size, turnover, and specific needs. To enhance overall engagement, Beksar integrated business financing functions that gave MSEs easier access to funds, which in turn drove greater involvement in automating internal processes. A special focus was placed on women-led businesses, equipping them with tailored tools and financing options to foster their growth and participation in digital transformation.

Shared project objectives

Promote the digital transformation of MSEs by automating business processes and enabling them to shift from cash to digital payments faster and more conveniently while offering value-added services to incentivize their usage

Enhance data analytics capabilities at MayaSoft and Beksar to analyze business dynamics and leverage transaction data for predicting MSE behavior in using digital business solutions and remaining active customers

Introduce segmentation scoring of MSEs for better decision-making and customer service at MayaSoft and Beksar

Incorporate embedded finance into MayaSoft and Beksar’s business models through partnerships with MSE lenders

With both companies, Accion built and validated analytical models that aim to enhance decision-making across portfolio management, customer segmentation, and risk monitoring. Our technical assistance integrated advanced data analytics, machine learning techniques, and business intelligence tools to generate actionable insights that improve growth strategies, risk management, and client retention.

The tool Accion developed for both companies combines transactional and behavioral data to design a scoring methodology and segmentation approach, ensuring robust statistical performance and alignment with business objectives. MSE clients are evaluated using at least six months of history, with the most recent three months used to calculate their Recency, Frequency, and Monetary (RFM) value. The model helps identify which clients will remain active users over the next 2-month period, supporting business actions related to retention, engagement, and portfolio optimization.

A central market hall in Almaty, Kazakhstan. Photo by Gwangjin Go on Unsplash.

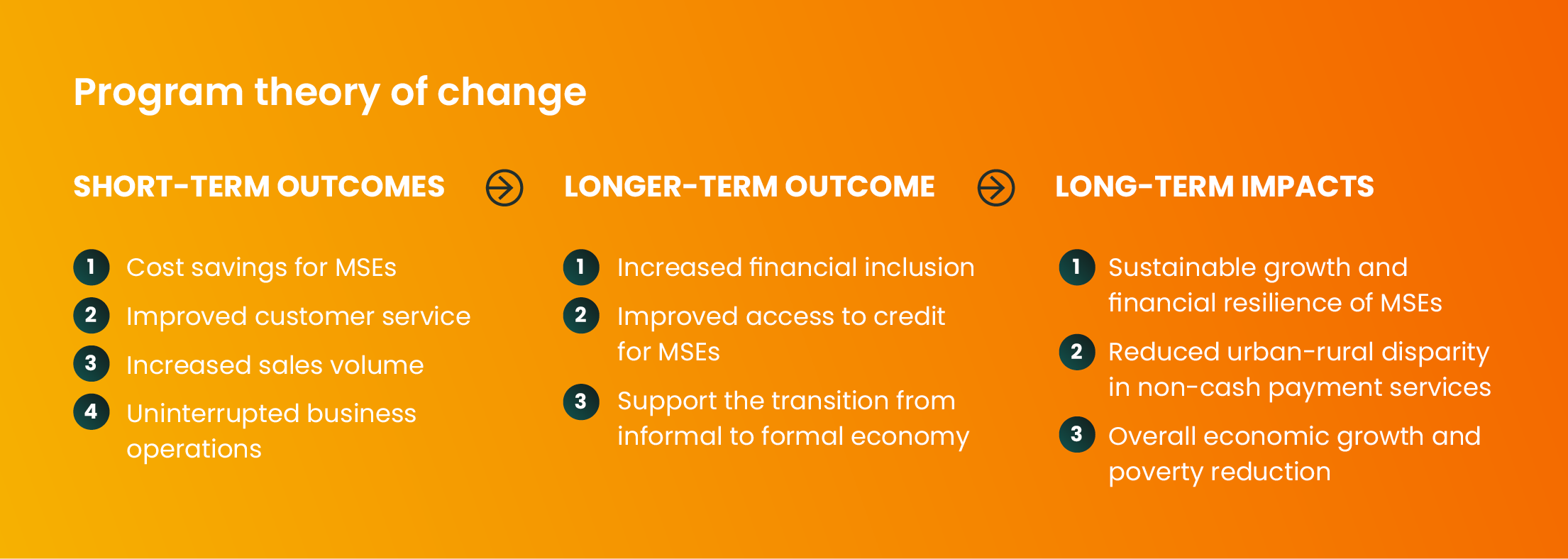

Key project insights

Within the framework of the shared project objectives, Accion, MayaSoft, and Beksar have compiled the following lessons learned from our collective experiences executing the projects, including data analysis, an endline survey of solution users in Uzbekistan, and qualitative interviews with MSE clients, industry experts, and other stakeholders.

For the MARTA Soft POS project, we surveyed 360 active solution users. The comparison group comprised 250 users who either did not use the solution regularly or became inactive. This impact study focused on outcomes aligned with the program theory of change. Qualitative interviews were also conducted with staff, clients, and industry experts. Due to time constraints, Beksar’s impact study relied strictly on qualitative interviews with a smaller group of new users and clients who received financing from MOST NeoBank, a new Beksar partner.

Expanding the outreach of digital business solutions to MSEs requires an enhanced and holistic value proposition and targeted marketing by segment.

Both MayaSoft and Beksar sought to expand outreach to their core target clients, MSEs, by leveraging their data and qualitative client feedback to better understand client behavior and needs, upgrade their solutions, and enhance their marketing strategies. While MSEs are becoming more aware of digital solutions and what they can offer, they are most aware of digital payment solutions, as demonstrated by the increases in digital payments to merchants. During its 10-month project, MayaSoft’s client base for its MARTA Soft POS increased by 250 percent, from 4,000 to over 14,000 MSEs. Beksar’s product enhancements have only recently launched, and results are forthcoming.

According to interviews conducted throughout the entire three-year project, MSEs in both countries tend to be skeptical of digital solutions. Their views are negatively affected by the prevalence of fraud and scams, as well as a desire to remain informal and outside the tax system. Micro-enterprises and self-employed individuals tend to be more informal. During the project, they expressed greater skepticism about digital solutions due to the risk of formalization arising from providers’ data collection. Among these segments, MayaSoft and Beksar observed significant merchant churn rates for their solutions before the project. This led them to reassess how their solutions’ value propositions met the expectations of a broader range of MSEs during the project to encourage regular use of the upgraded solutions after account opening or subscription.

High-touch approaches were key to driving digital adoption by MSEs in both countries, with third-party field agents, call center staff, and well-structured incentives playing central roles.

Each country has its own approach to digital marketing and communication. Accepted digital marketing channels among MSEs differ between Kazakhstan and Uzbekistan, ranging from Telegram to Instagram. However, high-touch channels emerged as key to driving adoption by MSEs in both countries. Both MayaSoft and Beksar used third-party field agents for marketing, training, and, where required, solution installation. With training and well-structured incentives, these agents explained to MSEs how to use the solution effectively, thereby increasing adoption rates and regular usage. Many MSEs preferred speaking with a person to answer their questions. In addition to field agents, call center staff at both companies played a key role in reducing friction in the onboarding process and scaling the solutions.

Although local industry experts often cited digital and financial literacy as an issue among MSEs, online capacity building for MSEs has not achieved important scale in either country. Several websites focused on such training reported low usage rates. Still, both MayaSoft and Beksar offer online video tutorials to build capacity and enhance solution usage. For those who can afford to view them on their smartphones, they provide valuable support, available at any time.

Enablers and barriers to digital business solution adoption among MSEs are driven primarily by solution design and existing infrastructure.

Enablers

Reliability of the solution builds trust among MSEs. According to the impact study, 91 percent of active MARTA users reported no issues with using the solution. The solution’s reliability is not just a technology outcome. It also drives behavior change. Merchants are building confidence in digital tools because MARTA consistently works.

Ease of use of a payment solution is an important component of the value proposition to MSE customers and another behavior change driver. Among active MARTA users surveyed, 47 percent indicated that the new version of the Soft POS was easy for their customers to utilize, compared to 12 percent of inactive users. This 35 percent difference indicates product-market fit in improving the customer experience.

Upfront cost savings reinforce MSE adoption. According to the impact study, 65 percent of active MARTA users estimated their monthly savings at $25 or more. For traditional POS, the MSE must purchase a device and pay a subscription fee. The MARTA Soft POS can be downloaded onto an NFC-enabled smartphone for free and only charges transaction fees. For the new version of its solution, Beksar has also opted to offer a basic version without charging a subscription fee.

Time saved and smoother checkout experiences foster emotional loyalty, even without large income gains. Among active MARTA users surveyed, 46 percent reported time savings, and 77 percent observed repeat customers due to the availability of card payment acceptance. In comparison, only 12 percent of inactive users reported time savings, and 27 percent observed returning customers. These differences demonstrate the loyalty effect and a positive impact on profitability beyond just cost savings.

Availability of field agents and call center staff to answer questions and provide guidance on how to use the solution. The integration of the Frequently Asked Questions feature in the solution and/or an AI-chatbot for customer support can decrease the workload of these agents and the call center and extend support to any time, even outside normal working hours.

Improvements in digital connectivity infrastructure. Many Beksar clients preferred to use the initial version of the solution offline on a local device due to its initial design and market positioning. Improvements in digital connectivity infrastructure and the cost of access would increase MSEs’ online use of the solution and improve Beksar’s data collection.

Increased support from commercial banks and other established ecosystem players, especially for the shift from POS devices to Soft POS and the addition of unsecured MSE loans to their digital offering.

Barriers

Digital maturity of most micro-enterprises and the need for a high-touch approach to onboard them. Due to limited digital and financial literacy, many new account holders rarely use their accounts for purposes beyond basic transfers.

Smartphone quality and capacity among MSEs may not be adequate, especially outside core urban areas. To address this barrier, MayaSoft gave smartphones to clients in one market in Samarkand.

Internet connectivity outside core urban areas is unstable and expensive in relative terms. While urban areas in both countries have seen rapid adoption of digital financial services, especially for payments, rural communities, where many merchants, smallholder farmers, and artisans are based, still rely heavily on cash. The MARTA Soft POS can conduct transactions via USSD. According to the impact study, advocacy levels among active MARTA users for the solution were higher in rural and peri-urban areas where connectivity is unstable. In part, this USSD feature may explain this advocacy trend.

Affordability of the solution. Small transaction fees tend to be more acceptable to MSEs than subscription fees. While Maysoft’s Soft POS transaction fees are higher than those of traditional POS provided by banks, merchants still prefer the Soft POS due to the absence of hardware purchase costs and subscription fees.

Partnerships and collaboration to offer embedded finance to MSEs can be challenging in emerging contexts, but opportunities are taking shape.

The project’s original concept was designed to foster partnerships between financial service providers (FSPs) and digital business solution (DBS) providers, with the goal of offering embedded finance solutions that combine the lending expertise of FSPs with the innovative platforms managed by DBS providers.

During the project period, market conditions presented some hurdles to building these partnerships. Still, these experiences highlighted valuable opportunities for the ecosystem to grow. For instance, FSPs were increasingly acquiring DBS to create their own corporate ecosystems, and competition in the digital financial services space intensified. While these were signs of dynamic and evolving markets in both countries, the establishment or consolidation of these corporate ecosystems was not conducive to collaboration more broadly. In addition, many lenders, especially commercial banks, prefer to engage with MSEs with more traditional business models. Microfinance organizations that do serve MSEs have room to strengthen their technical capacity, particularly in core banking systems and other IT infrastructure, to implement partnerships with DBS providers.

These developments suggest the MSE finance ecosystem in the region is at an important inflection point. Encouraging greater innovation through partnerships, coupled with support mechanisms such as risk-sharing guarantees, can enable FSPs to explore and test new MSE loan products delivered through DBS platforms. The alternative, DBS offering credit directly to MSEs, can be even more challenging. In most cases, DBS providers in the region are not set up to offer credit on their own. They often lack the financial resources, key technical skills, and risk management systems required. Strategically, they are better positioned to collaborate with a licensed lender to offer embedded finance through their platforms.

The most suitable partners are neobanks interested in lending through existing platforms. During the project, MayaSoft collaborated with Anor Bank, a branchless commercial bank, to bring its upgraded Soft POS to market, and Beksar proposed its clients to MOST NeoBank for financing. This collaboration between Beksar and MOST indicates that optimism is warranted. Licensed as a microfinance organization, MOST is a B2B financial technology platform that offers digital financial solutions designed to provide credit to MSEs in the technology sector across Central Asia. During the project, MOST financed 40 Beksar clients with unsecured working capital loans totaling more than US$300,000 and has maintained strong portfolio quality among them.

Transactional and sales data analysis generates predictive segmentation scoring models to enhance MSE lending and reduce churn.

Accion used sales transaction data from both MayaSoft and Beksar to design segmentation scores that predict how active MSEs would be in using the digital business solution. These scores are not meant to assess credit behavior, but to identify which active clients should be recommended for further credit assessment by lenders and can be used to better segment customers, price products, create channel strategies, and develop loyalty rewards schemes. Both companies plan to use the segmentation scoring to better understand their MSE clients’ behavior and to design loyalty schemes and other services that reduce churn. They will also invest more in building internal capacity for data analysis and score management.

Digital business solution providers can use segmentation scoring to better understand their MSE clients’ behavior and to design loyalty schemes and other services that reduce churn.

The segmentation scores were more predictive than expected. Using data from MayaSoft and Beksar, Accion developed a set of 6-11 new variables that could be combined to generate their respective scoring models. Based on initial tests, the discrimination levels of these two statistical models are strong.

To develop more robust segmentation scores or even credit scores in the future, MayaSoft and Beksar must continue to improve their data collection. Many DBS providers tend to minimize data collection on applicants to reduce friction at onboarding. However, they need to collect sufficient data and obtain client consent to access third-party data to conduct a full assessment of MSE clients, especially if they want to offer credit directly. Both companies revised their data collection practices as part of the project.

One-size-fits-all digital business solutions fail to engage diverse MSE segments and increase churn.

Based on the project’s segmentation analysis, it is important to note that MSEs are not a monolithic market segment; they exhibit diverse characteristics that are often overlooked in DBS design. Segmentation scoring models can inform DBS design and improve the MSE user’s experience. While microenterprises and self-employed individuals often prioritize simplicity and affordability, more established small merchants value analytics, reports, and financing features. For example, Beksar proposed loans to hundreds of its clients, but only 40 opted to pursue a loan from MOST. Many others appreciated the opportunity but did not want or need financing at that moment.

The segment of self-employed individuals is MayaSoft’s main inclusion objective: digitizing merchants previously excluded from card ecosystems. More active self-employed respondents to the survey (85 percent) recommend the MARTA SoftPOS than active legal entities or individual entrepreneurs (65 percent). This segment values MARTA’s no-hardware, low-cost model to a greater degree, as it allows them to accept digital payments without a fixed location or formal infrastructure.

Moreover, women-led and rural MSEs add further layers of differentiation that require inclusive solution design, tailored communications, and simple user interfaces. The segmentation scores will be used by Beksar and MayaSoft to optimize and personalize their solutions to the needs and aspirations of the diverse segments with the aim of reducing churn.

Women-led MSEs represent the strongest untapped potential for digital solution uptake and growth in the region.

The representation of formalized women owned MSEs is likely to be understated compared to the real market opportunity. According to recent studies, Uzbek women own only 16 percent of MSEs. In Kazakhstan, women own 30 percent of MSEs. The World Bank conducted enterprise surveys in 2024 that indicated similar ownership figures. However, according to several local market experts, women in both countries play key roles in the ownership and leadership of the majority of MSEs although they may not be represented as the registered owner. This is important for FSPs and DBS to consider as they design new solutions or optimize current solutions in order to improve their value proposition for women entrepreneurs.

Women entrepreneurs often manage both business and household responsibilities, leaving little time for solution training and onboarding. Among MARTA users, many also expressed less confidence in using new digital tools, especially in rural areas, and prefer advice from trusted peers to online sources. As a result, they were less likely to engage with long, technical tutorials and more responsive to short, relationship-based support. Women entrepreneurs were also concerned about data privacy and the formalization of their businesses, which can add another layer of hesitation to digitization. Despite these challenges, the role of women in owning, managing and developing MSEs is important in the region but tends to be understated and not accounted for sufficiently in DBS design.

More targeted solutions and trust-based support will improve their inclusion. According to the impact study, women-led MSEs perceive MARTA as simpler, safer, and more reliable. These factors are key drivers of adoption in low-literacy contexts. More female users (53 percent) would recommend MARTA than male users (48 percent). Female merchants also reported slightly higher perceptions of reliability and ease of use, thereby suggesting that inclusive design and low onboarding barriers particularly benefit women-led MSEs.

Rural MSEs face more constraints in using digital business solutions regularly.

MSEs in rural areas are significantly constrained in using digital financial services and digital business solutions due to poor internet connectivity, high costs, and low smartphone quality. These barriers remain pronounced in rural Uzbekistan and Kazakhstan.

Although many rural MSEs are aware of digital business solutions, transaction failures, slow loading times, and high data costs discourage consistent use. MayaSoft has aimed to address this by enabling the MARTA SoftPOS to function without internet connectivity via USSD. The higher rates of advocacy for MARTA among active users in the more rural regions indicate that this feature and other inclusive design features have successfully addressed some of these constraints.

Digital access does not guarantee financial empowerment.

Although both Kazakhstan and Uzbekistan report sharp increases in account ownership and digital payments usage in the past 10 years, as outlined above, many MSEs use accounts passively or withdraw cash immediately after transfers. MayaSoft observed similar usage behavior with artisans and self-employed individuals. This behavior indicates that access to digital business solutions and financial services is not sufficient on its own to improve business performance among MSEs. As highlighted by the impact study of the MARTA Soft POS project, satisfaction with and advocacy for the solution are notably higher among active users than among inactive users. Sixty-six percent of active users recommend MARTA, whereas only 26 percent of inactive users do. Based on its simple, safe, and reliable design, this inclusive solution has reduced costs and time spent on transactions for many MSEs, which have become active users. However, other MSEs that registered and opened accounts but stopped using the solution for various reasons have not realized the same financial gains.

Mobile transactions bring traditional small retailers into the digital economy. Courtesy of Mastercard Strive.

Key stakeholder recommendations

Embedded finance is an important opportunity that is currently limited in Central Asia to e-commerce platforms developed or owned by banks. Other platforms focused on serving MSEs could be leveraged more effectively to provide affordable, unsecured loans, based on available data. Partnerships between banks, microfinance organizations, and DBS providers can test data-driven lending models rather than relying on traditional collateral-based models.

FSPs can also build internal capacity to analyze alternative data to better assess MSEs, especially those with limited or no formal credit history. Emerging neobanks with this skillset can develop and de-risk embedded finance for MSEs in collaboration with fintechs and digital business solution providers.

FSPs can develop digital financial services tailored to the realities women entrepreneurs face. Mobile microloans, microinsurance, and digital layaway (buy now, pay later) options could enhance their business stability. These products should incorporate smaller loan sizes and account for irregular income patterns and the lack of collateral. Their design should explicitly consider women’s needs, risk profiles, and time constraints.

Data collection and analytics are a key part of scalable, sustainable business models, and it is important to build this internal capacity at an early stage. To achieve this, fintechs and DBS providers can partner with local universities and accelerators or join specialized programs. Stronger data capabilities enable these companies to better segment the market, understand client behavior, design relevant products, and attract partnerships with lenders and investors.

Digital solutions for MSEs must have clear links to real business outcomes. Most solutions are focused on facilitating transactions and reducing costs. Features that promote business growth, such as digital marketing, inventory management, and customer engagement, should be enhanced and deepened to add greater value to MSEs. They should be accompanied by training programs for entrepreneurs on analyzing sales and expense data, accessing e-commerce platforms, and using financing strategically.

Fintechs and DBS providers seeking to reach MSEs can design their apps to function in low-connectivity environments. For example, they could promote blended access (online and offline) for rural MSEs by combining mobile apps with local agents and creating simplified user interfaces in local languages.

Fintechs and DBS providers should be encouraged to bring tried and tested offerings to other markets in the region where MSEs have fewer resources and capacity to invest in digital business solutions.

More space is needed within the digital financial services ecosystem to encourage innovation and collaboration. More agile startups are constrained in the current ecosystem by their reliance on public funding and the high cost of capital. Modernizing licensing and supervision procedures could allow innovative fintechs to operate under lighter regulatory tiers, while maintaining oversight, to drive innovation. More public-private funds should be made available to support these initiatives.

Rules and regulations governing loan-loss provisioning for FSPs should be reviewed to allow such models to be tested and reduce the cost of serving MSEs.

Measures to improve consumer protection and public trust in digital financial services are advantageous. Throughout this project, MSE owners expressed concerns about hidden fees, fraud, and data misuse, which deterred them from using digital financial services. Transparent fee disclosure, fair lending practices, and strong digital security standards can build public trust and are essential to increasing MSE participation in emerging digital financial ecosystems.

Internet connectivity in rural areas limits access to digital business solutions. Increased investment in telecommunications and broadband infrastructure is needed in these areas. Governments and telecom operators should invest in extending internet coverage to rural areas, especially where MSEs are concentrated.

The region’s universities can enhance education in statistics, new data analytical methods and tools, and related skills.

A bolder approach to funding regional innovation is encouraged. Funding from donors and impact investors should prioritize local fintechs and DBS providers that demonstrate inclusive impact potential, particularly those that enable access for MSEs in rural areas.

Longer-term financing would allow innovative companies to strengthen their products and attain sustainability beyond the pilot phase.

Capital should be complemented by mentoring and investor-readiness training for scaling FSP and DBS products.

A local vendor displays his wares at a market in Samarkand, Uzbekistan. Courtesy of Mastercard Strive.

Conclusion

Digitization and embedded finance can significantly transform MSEs in Central Asia and further fuel economic growth. Stakeholders in the region have demonstrated that concerted efforts at public and private sector collaboration can expand access to important business and consumer tools, such as smartphones and digital payments.

However, success depends on more than technology and capital. Accion’s experience working with MayaSoft and Beksar demonstrates that tailored, inclusive design, strategic partnerships, and targeted initiatives to address persistent barriers are critical to driving adoption and sustained use of digital financial services and business solutions among MSEs in the region. By encouraging ongoing collaboration and coordinated efforts from all stakeholders to action these recommendations, we aim to accelerate progress and achieve lasting impact.