Cover photo: With support from Annapurna Finance Ltd. through the pandemic, Papina Das reopened her small dairy business in Odisha, India.

This article is the first of a six-part series on scaling financial inclusion to accompany our digital transformation guide.

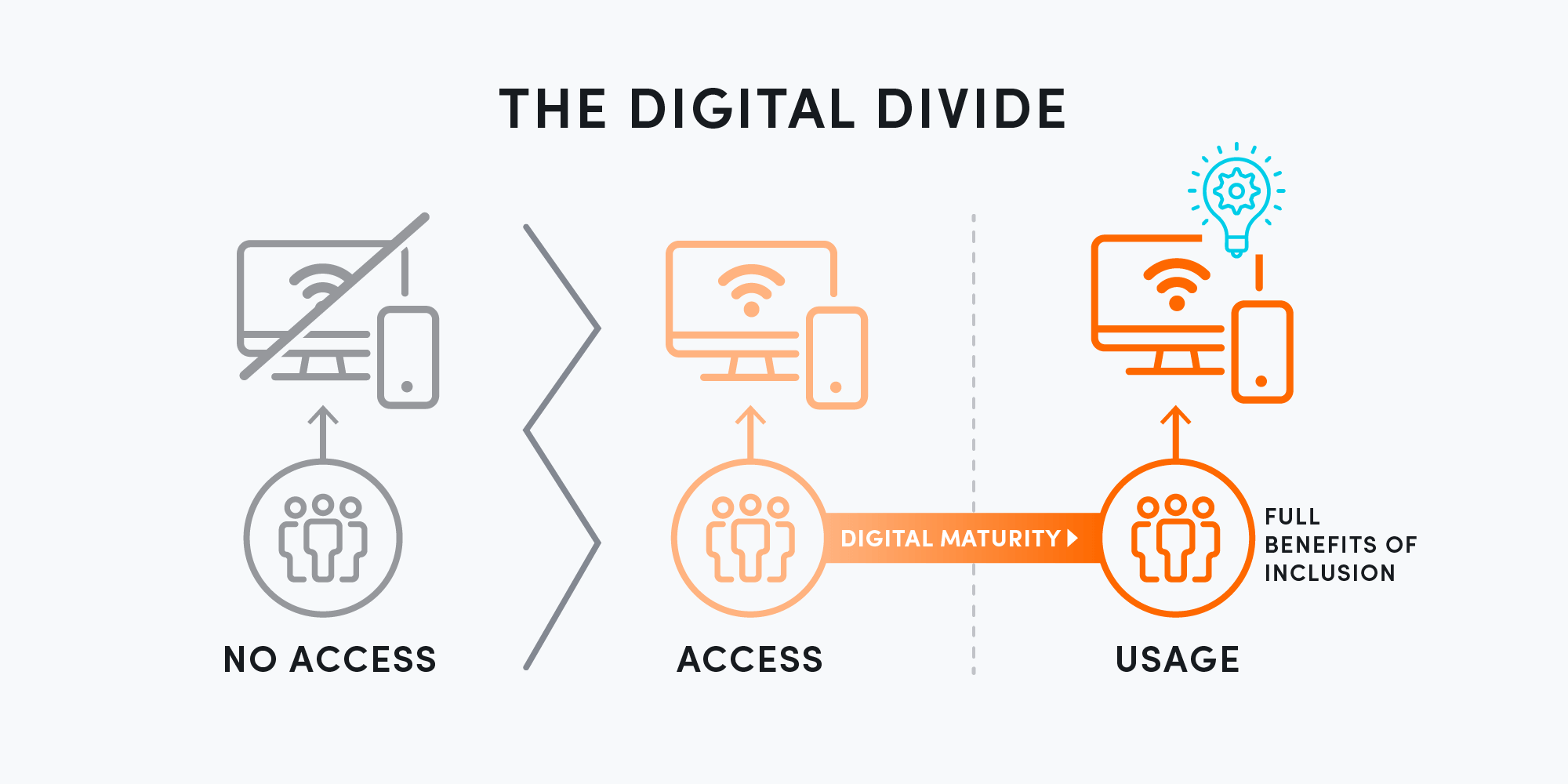

During India’s first strict COVID-19 lockdown, Papina Das, a dairy business owner in Odisha, faced plummeting sales and an unstable income when people in her village avoided visiting the local market and stopped buying her cows’ milk. In the face of unpredictable challenges, digital financial tools can help micro, small, and medium enterprises (MSMEs) owners like Papina build resilience by giving them access to credit, payments, insurance, and business management advice. However, low-income individuals and small business owners don’t always have the digital skills, attitudes, and behaviors they need to use such tools. While some people are comfortable using technology in their daily lives, many lack access to smartphones or stable internet connections, and others simply do not trust or feel comfortable using unfamiliar digital financial services. With customers spanning many different levels of digital awareness, how do financial service providers effectively bridge the digital divide to support their clients and reach the most vulnerable?

In partnership with the Mastercard Center for Inclusive Growth, Accion recently published a guide to help financial providers (FSPs) navigate the complexities of digital transformation. We uncovered three key strategies to combat the digital divide that prevents FSPs from reaching clients in need of financial services.

1. Communicate how digital products help customers improve their businesses

“Our digital transformation goes hand-in-hand with our clients’ digital transformation.”

– Verónica Gavilanes, General Manager, Microfinance, Banco Pichincha in Ecuador

For small business customers accustomed to using cash, the value proposition of switching to digital payments can be difficult to understand — particularly when customers perceive cash to be free and more secure. Communicating the benefits of digital products by using clear messages that resonate with small merchants can help them overcome their initial hesitation.

Banco Pichincha is the largest financial institution in Ecuador. As the bank undergoes a complete, large-scale digital transformation, they recently launched Billetera deUna!, a mobile wallet that supports secure, real-time payments for their customers. While the application has been downloaded more than 118,000 times, this is concentrated among high-income segments, with much lower uptake at the base of the pyramid.

Nearly eight in 10 Ecuadorians have mobile phones, but only 32 percent of those with phones are currently using them to make digital payments. Cash still accounts for about 40 percent of payments, with cash being particularly prevalent in rural communities. Using insights into their customers’ adoption barriers, Banco Pichincha has redesigned the user experience for underserved microbusinesses with a clear and compelling value proposition. In parallel, the bank is using Accion’s edtech platform, Ovante, to help their microfinance customers gain the digital literacy and skills they need to use the platform.

2. Design for both sides of the digital divide

FSPs that serve low-income people and businesses face the challenging reality that some of their customers do not yet have access to digital devices and will continue to depend on high-touch services offered through the traditional microfinance model. At the same time, they have client segments that prefer the accessibility, convenience, and speed that digital financial services can provide.

India’s Annapurna Finance Limited serves 1.9 million group lending customers who would otherwise lack access to high-quality, affordable financial services. When pandemic-induced lockdowns effectively ended group meetings, members found themselves without much-needed finance at a time when economic vulnerability skyrocketed.

While only 10 percent of Annapurna’s group lending customers currently own a smartphone, a greater percentage has access to less advanced feature phones. To address the digital divide, Accion worked with Annapurna to create an SMS-based, digitally accessible emergency loan product that incorporates both tech and touch. For example, interested customers can provide details directly to their loan officer for their application and receive an emergency loan limit if qualified. Once deployed, a customer can access the funds at any time without interacting with a person by sending a simple SMS to a dedicated phone number, which then disburses the money to the customer’s loan account.

We designed the solution to easily upgrade to a smartphone version so that customers can grow with the platform as they gain digital skills. For the more digitally savvy segment of Annapurna’s MSME clients, we are supporting the bank in developing an end-to-end digital loan that allows clients to apply without needing to speak directly to a loan officer and make all repayments remotely.

3. Balance tech and touch strategies

Human interaction continues to be critical in delivering financial services to the poor as personal interactions build trust, establish relationships, and engage customers. For customers with low digital maturity, FSPs should think strategically about hybrid models that leverage digital to automate manual processes while still maintaining the human touch that customers value.

“Our approach is to first understand our customers, understand the segment that we want to serve, understand how digitally mature they are, and then reach out to them [in a way that is uniquely suited to the circumstances].”

– Taiwo Joda, Managing Director and CEO, Accion Microfinance Bank in Nigeria

Accion Microfinance Bank (Accion MfB), one of Nigeria’s most successful microfinance institutions, aims to make digital their new norm and encourages digital behaviors in their client base. As part of this goal, they made the end-to-end application process for their new digital loan accessible only through a mobile app or web portal. But Accion MfB knew that not all their customers are ready for a fully digital process, so they designed the product to allow customers to initiate the digital loan application process through several different channels. Using USSD mobile codes, customers can submit a request for digital assistance, which prompts the call center to reach out to the client and understand their characteristics and comfort level with digital applications. The call center agent may then direct applicants to one of the self-service channels to complete an application online or may refer applicants to a branch where a staff member can assist with a loan application.

Finally, after noticing discrepancies between customers who were initially denied online but later approved after visiting a physical branch, Accion MfB also made several changes to the digital loan application to more closely resemble how an account officer would ask questions. They also integrated more customer support, examples, and tips.

To bring useful financial tools to underserved MSMEs in a way that promotes trust and comfort, financial providers need to tailor their digital approach to their customers’ varying levels of digital skill and access. FSPs should be deliberate and thoughtful about how they reach clients on both sides of the digital divide: leaning into digital channels, while continuing to leverage physical networks like branches, loan officers, and groups. Meeting clients where they are will promote greater digital adoption and ultimately fuels the digital transformation of low-income individuals and small businesses.

Malavika Krishnan contributed to this article.

Explore More