This article is the fourth of a six-part series on scaling financial inclusion to accompany our digital transformation guide.

Data capabilities are essential to an organization’s digital transformation: from informing strategies that increase efficiency and revenue to creating new business models where data assets become products. In today’s world, where financial service providers (FSPs) must make unprecedented and rapid decisions, adjust business strategies, segment customers to understand portfolio risks, rethink credit models, and reach customers and staff remotely, data capabilities go hand-in-hand with digital transformation.

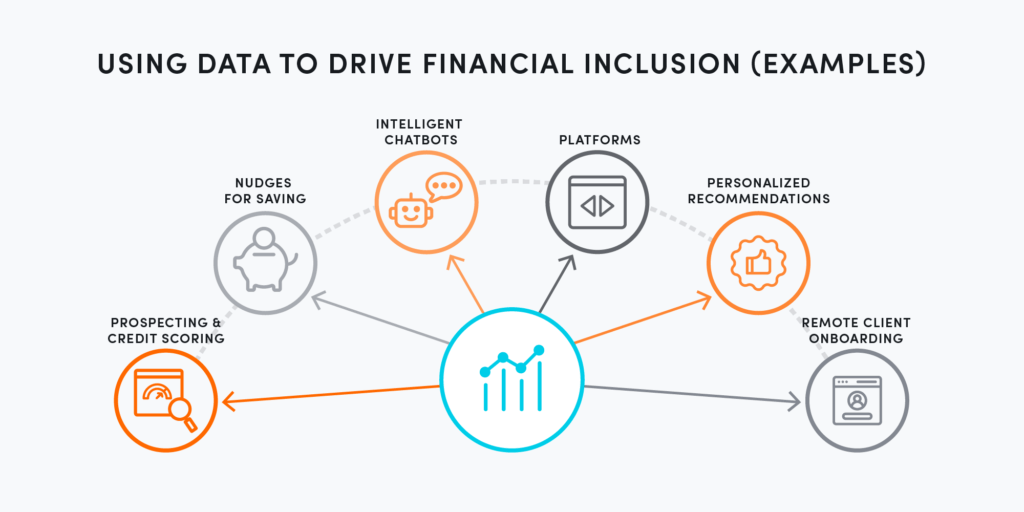

The explosion of available data, data-analytics services, and a growing digital ecosystem creates unprecedented opportunities for underserved communities and FSPs alike. The potential to unlock greater financial health for FSP customers is extraordinary, from prospecting and credit scoring for thin-file consumers to well-timed nudges for saving to intelligent chatbots, personalized recommendations, and remote client onboarding.

However, many organizations become overwhelmed by all the different ways they can use data and lose alignment when creating a focused data strategy. FSPs can take several steps to integrate data and analytics activities with their digital transformation goals:

Start with existing data

In the early stages of developing a digital loan product, Accion Microfinance Bank (Accion MfB) in Nigeria explored potential data-sharing partnerships to build a robust credit scoring model. But they struggled to find the right third-party data provider, so Accion MfB decided to look inwards at the lending data they had already amassed. For example, using what they knew about customers’ willingness and capacity to pay, they designed a pilot digital loan product and created a benchmark profile to compare incoming data against when onboarding new customers. Using their own internal data involved fewer operational and commercial complications, which helped Accion MfB quickly launch a viable pilot.

Be practical in moving from insights to action

Similarly, our longtime partner BancoSol, one of Bolivia’s largest banks, realized that leveraging their untapped data could uncover insights to help address four key challenges: driving digital adoption and improve usage, increasing cross-product usage, increasing savings balances, and maintaining customer relationships. A 36-hour datathon organized in partnership with Accion and Mastercard yielded three key recommendations to tackle these challenges:

1. Start by understanding your typical digital customer. Analyzing customer demographic data and banking patterns can help identify, prioritize, and nudge those customers who are most likely to go digital. BancoSol learned that their typical digital app customer is more likely to be female and younger than the average BancoSol client.

2. Equip loan officers with insights to match customers with products that meet their needs. The datathon revealed that app users made nearly twice as many deposits as other users, linking digital adoption with increased use. As research has shown, greater use of financial products makes small businesses more resilient to shocks.

With these insights, BancoSol developed clear messaging for loan officers about the benefits of going digital and respecting privacy and security measures and implemented continuous testing and streamlining to improve the app experience so it matched customer expectations.

3. Retain customers by being proactive, not reactive. The datathon also showed that when customers stop saving or communicating with the bank, their risk for a loan default rises, while those who used digital channels maintained consistent relationships with the bank. With that in mind, data analysts created a risk propensity score, which BancoSol can use to intervene before a customer begins to disengage.

Having dedicated resources skilled in data analytics embedded within the product innovation team is crucial to jumpstarting a virtuous cycle of data-driven design.

Prioritize data management and governance

To derive value from data and ensure customers’ privacy is protected, microfinance institutions need to invest in structuring their data appropriately and maintaining deliberate data governance (policies and procedures) and management (use of data in decision-making).

While many institutions know they possess valuable data, it’s often stored in various places and multiple formats, leaving the organization to only manage the limited data they are required to, or that is easily accessible. To get ahead of the curve before messy data accumulates, Annapurna Finance Limited in India invested heavily in data management solutions that improve data reporting, data migration, and data storage for new digital platforms and products.

Nearly every financial institution struggles to maintain accurate customer contact information, a simple yet critical example of data management. For microfinance institutions with high-touch models whose loan officers regularly visit their customers, having a current phone number on file seemed like a low priority. But when lockdowns brought on by the COVID-19 pandemic began, Annapurna’s loan officers found themselves unable to communicate critical loan information — like payment dates, updates on moratoriums, or even introduce new loan offers via SMS to their group lending customers — without up-to-date contact details.

To address this challenge, Annapurna introduced a standard process to ensure that at every customer touchpoint — from field visits from a loan officer to customer visits to a branch — bank staff would confirm the customers’ phone numbers to ensure a high-quality database. In parallel, they implemented a new communication system that integrates their SMS system with their loan origination system. These two initiatives standardize communications with customers, create greater engagement, and ensure a more transparent flow of information.

A clear data strategy can help inclusive FSPs accelerate their digital transformation, make organizational changes to better leverage their data and become more customer-centric, and ultimately set low-income households and microentrepreneurs on a path toward greater financial health.

To assess your organization’s current data capabilities and gain insights into priority areas, take our Data Maturity Diagnostic. Reach out to us to see how we can help plan a roadmap of strategic data initiatives to support your institution’s digital transformation journey and business goals.

Malavika Krishnan contributed to this article.