Over the past decade, human-centered design methodologies have made their way from Silicon Valley to the financial inclusion sector. These methodologies, which are based on deep customer understanding, blue sky ideation, and rapid prototyping, have been touted as the silver bullet to address ongoing access and usage problems at the base of the pyramid, particularly with regard to digital financial services. Initial results were promising: in collaboration with leading design firms, institutions were able to develop innovative product concepts and prototypes grounded in the realities of customers’ lives.

However, these products haven’t always been as successful as expected. Many products do not ultimately gain traction with customers, and others are discontinued as institutional priorities shift. Some institutions have focused on customer needs but overlooked real operational and business constraints. Others miss the complexities surrounding customer behavior and financial decision making and inadvertently solve the wrong problem.

The need for digital, customized and responsive financial products and services is greater than ever. The economic fallout from COVID-19 has disproportionately affected those without the access, resources, or network to weather the storm. Innovative financial products can help people to recover from the crisis and restart in the new normal.

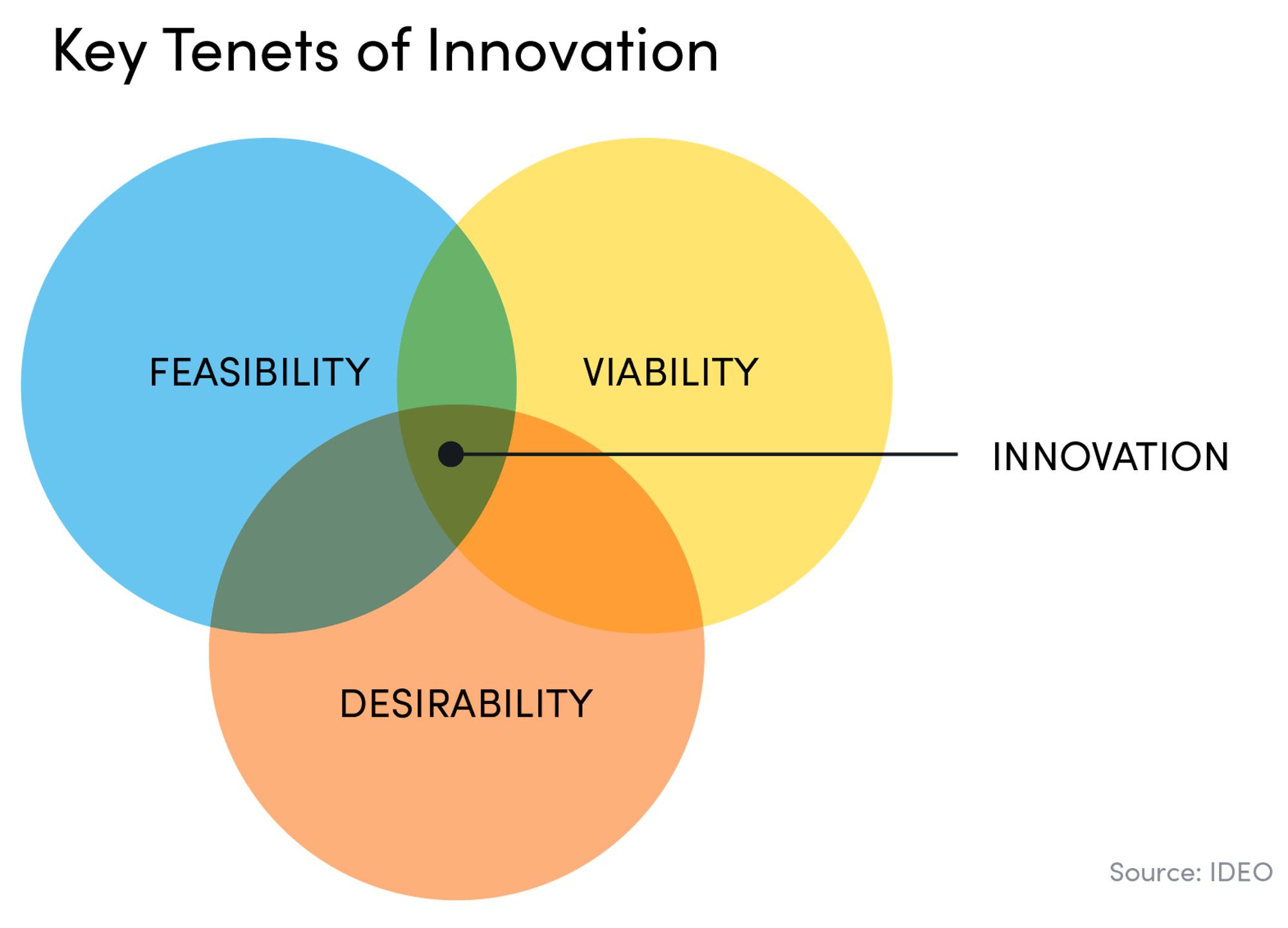

Innovative digital products must balance customers’ needs with organizational capacity and should be built upon a solid business case to ensure that the product is sustainable in the long term. This trifecta of desirability, feasibility, and viability seems intuitive but is not easy to implement — institutions must navigate competing priorities, limited resources, and tradeoffs between each area. Our latest white paper explores the interplay between desirability, feasibility, and viability, and shares lessons learned from our recent experiences working with five financial services providers and fintechs in Chile and Mexico. With the support of MetLife Foundation, we are working with these institutions to design and launch behaviorally informed products that build customers’ financial capabilities and ultimately improve their financial health.

A few key takeaways from the paper:

- There are many ways to learn from your customers: In-depth field interviews are an important channel for understanding people’ lives, but they can be time-consuming and aren’t always feasible — particularly during a pandemic. Customer data is a rich and often underutilized resource to identify trends and user pain points. We start our customer understanding with data analysis to build hypotheses that we can later test and refine through user research, in-person where possible, or remote.

- The most valuable feedback will come post-product launch: No research or data analysis is as valuable as customer engagement with an actual product. Even prototyping has its limits: customers may sit and look at an application for an hour with an interviewer, but in reality, they may only have five minutes to use the product during their daily lives and experience constant interruptions, connectivity challenges, and competing demands for their time. Financial institutions should seek to go to market quickly with a minimum viable product, build in robust feedback loops, and plan for ongoing improvements.

- Consider innovation you can sustain: In the quest for innovation, institutions often feel they must ‘go big’ and develop completely new, groundbreaking solutions. But these products often don’t make it past pilot because the gaps required for long term success are too large. Innovative products often require new skills, updated technology, or new partnerships. A more feasible product can still be innovative without requiring a full-blown overhaul of the institution. It is critical to assess operational and technological capabilities from the start, understand the implications of proposed product design, and actively plan to address gaps. Incremental innovation can be just as powerful to drive customer usage and growth.

- Build a business case from the beginning: In the product design process, some design efforts prefer to focus on the idea before considering business case implications. While helpful to think out the box, we’ve found this can be dangerous. Without a business case, product ideas may never get the buy-in to move to pilot; or worse, they may lead the institution to invest time and money in products that don’t make business sense. It is not enough to create a product that customers love — it must drive growth, reduce costs, or generate revenue. We always start with a preliminary business case at the concept stage and then flesh out a detailed projection of user growth, revenue, break-even analysis, and assumptions.

Innovative ideas will not help customers reach their goals or recover from the pandemic if they cannot be implemented and scaled. In the long run, products that truly drive financial inclusion are those that balance desirability, feasibility, and viability. For customers, this approach translates to more intuitive financial products and services that are aligned with their behaviors and help build their financial health. For financial service providers, this approach leads to innovative products that are sustainable, use internal resources efficiently, and achieve business goals. Learn more about how we created sustainable and innovative products in Mexico and Chile by reading our paper, To succeed, innovative financial products must be desirable, feasible, and viable.

Explore More