In today’s rapidly digitizing financial ecosystem, account aggregators have emerged as vital enablers of secure data sharing, reshaping how financial information is accessed and utilized in India. For any regulated entity, partnering with the right account aggregator is not merely a technical choice — it is a strategic decision that can influence operational efficiency, customer experience, regulatory compliance, and long-term competitiveness. This is especially significant for institutions that serve small business owners, rural women, and other low-income segments traditionally viewed as costly and high-risk customers. Leveraging account aggregators can enhance an institution’s ability to assess credit risk and expand financial access for these customers, and offer tailored products and services.

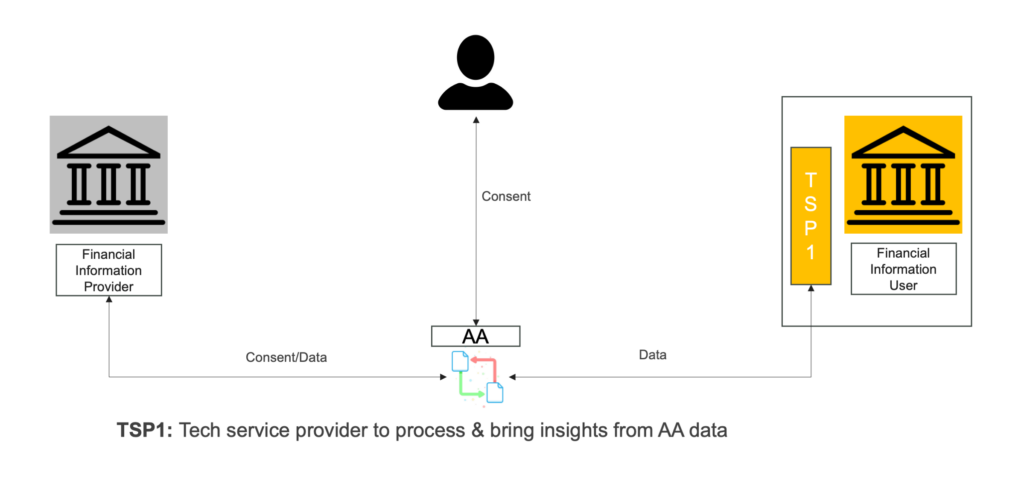

Accion Advisory is currently collaborating with local partners to develop demonstration models within the account aggregator ecosystem that advance financial inclusion. This involves connecting financial information users, typically formal financial institutions, with account aggregators and technical service providers that process and bring insights from account aggregator data. Given the criticality of these interrelationships, entities seeking to use financial information and partner with an account aggregator should carefully evaluate several key factors.

Coverage and connectivity

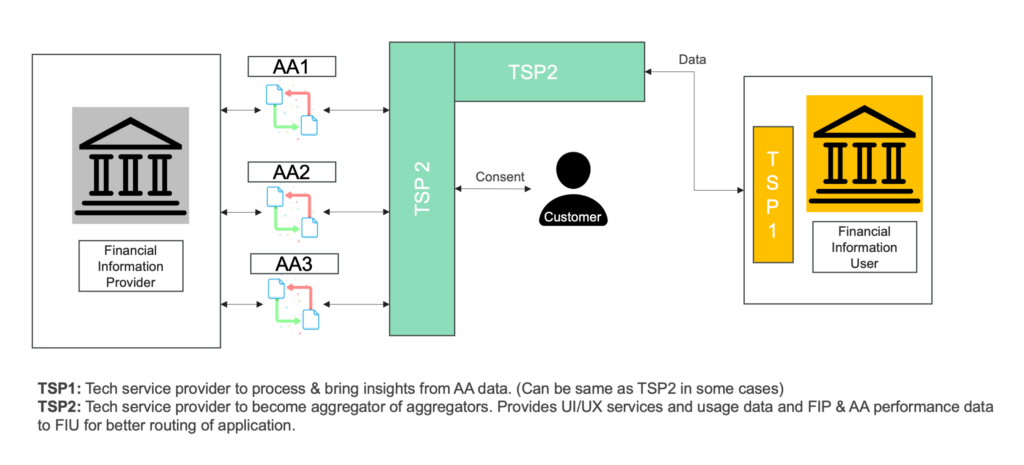

The value an account aggregator brings is directly related to its connectivity with financial information providers, including banks, mutual funds, and GST and insurance companies. A wider network aids better access to reliable, real-time customer data. Financial information users, or institutions, should seek account aggregators that already have existing connections with important financial information providers to ensure high serviceability. Relying on a single account aggregator for expanding coverage is not advisable, however, as that increases the risk of downtimes or data fetch failures. Onboarding an alternate (refer to Figure 1) can mitigate this risk and enhance coverage from key financial information providers that have data on the institution’s target segment.

Institutions can also partner with a technical service provider that functions as an aggregator of aggregators, handling connectivity and coverage (refer to Figure 2). The technical service provider enables ready API integration with multiple account aggregators, reducing the time for institutions to access data, and provides options when multiple attempts are being made to fetch customer data.

This resource from Accion partner and account aggregator industry alliance Sahamati provides a detailed look at the current coverage of financial information providers.

Performance

Key metrics for assessing an account aggregator’s performance include total consents handled and successfully shared across a finite period, total customer drops throughout the journey, consistent uptime and downtime, and distribution of consents across existing financial information users. Institutions should also assess failed attempts to fetch data or register consent, the reasons they failed, how these failures may affect service, and the mechanisms to overcome them.

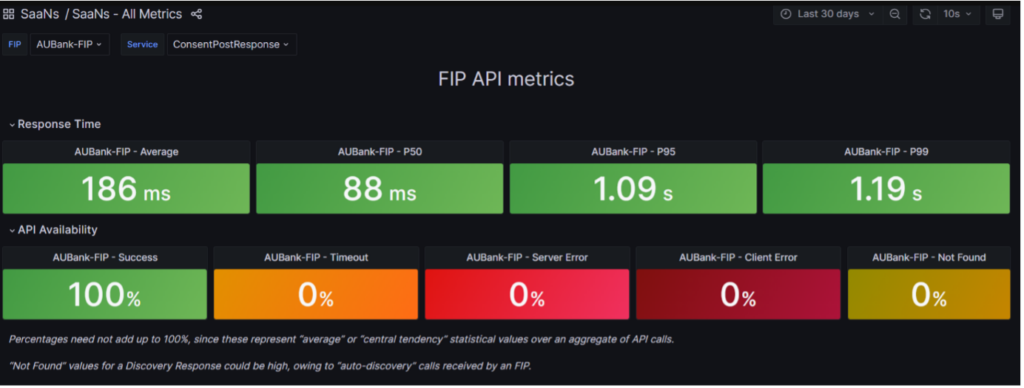

Sahamati’s Swasthya of AA Network as a Service (SAANS) service tracks the performance of financial information providers’ API. “Swasthya” means “health” and “Saans” means “breath” in Hindi, signifying the liveliness of the APIs. Figure 3 is a sample SAANS output that illustrates that the performance indicator is not limited to showing uptime, but also highlights the reasons for failure in successfully fetching data.

Target segments and service distribution

Account aggregators provide data fetch services for various financial products, including investments, loans, and stocks. Institutions should clearly define the distribution model for their primary product, then check for an account aggregator that can add value. The product may require an embedded account aggregator service, a web-based portal, or a redirection journey. For instance, a do-it-yourself journey-focused account aggregator may add little value for a product that requires assisted distribution through channel partners, as the customer and channel partner interfaces may be very different.

Ease of integration and technical support

Factors like lightweight APIs, clear documentation, plug-and-play capabilities, and robust onboarding support can substantially reduce integration timelines and costs. Institutions may also have unique requirements that account aggregators must accommodate based on target customer segments, such as micro and small business owners, first-time borrowers, or rural populations. A one-size-fits-all account aggregator may not suffice.

Additionally, account aggregators should provide technical support for successful data fetch, retry mechanisms, and UI/UX glitches, and ensure quick troubleshooting.

User experience

For account aggregators, user experience extends beyond the end customer. The primary user of the service is the financial institution, with the customer’s consent. The users of account aggregator data can be external — the institution’s customers, who may be new to the process of giving consent to use their data — or internal — the institution’s staff. Internal decision-makers using the data require it in a certain format, either through a business rule engine output or an expert scorecard, while external customers require a user-friendly interface and experience to provide account details and consent.

The account aggregator’s ability to customize output data formats, consent journeys, and user interfaces (especially for non-English speaking customers) and provide device compatibility, language translations, and interoperability can be significant advantages in ensuring adoption and operational success.

Cost structure and pricing transparency

Pricing models depend on factors like transaction volumes, number of user accounts, number of active financial information providers, time to go-live, and customizations. Pricing is proportional to components like data types to fetch (higher for more data), account volumes being onboarded or fetched (per-pull-based or tiered), service level agreements, and one-time integration costs. Institutions should consider transparency, scalability, and predictability while defining terms and negotiating a fair, flexible, and tiered pricing structure with the account aggregator to accommodate future expansion needs and service quality.

Technical service provider layering

Although the account aggregator provides secured, reliable, and consented data, it is still raw data. To make meaning out of the data, the financial information user, the institution, needs intelligence. That’s where the technical service provider comes into play, particularly for institutions without the systems to generate actionable insights internally.

The institution can receive these insights from the technical service provider to meet their requirements instead of the financial statement dump from the account aggregator. This reduces the lead time for delivering the product or service to the customer and saves the institution from developing an analytics layer on top of the account aggregator data themselves. Other benefits of integrating a technical service provider during setup include audit-ready reports, customizable analytics models, and faster go-live times.

In conclusion, selecting an account aggregator is no longer just a decision that enables faster access to customer data — it’s a strategic investment that directly influences an institution’s ability to better serve its customers. Choosing an appropriate account aggregator partner, especially when bundled with a capable technical service provider, offers actionable intelligence, operational efficiency, and enhanced user experience, which are crucial in today’s digital-first environment and for serving rural or low-income customers who may be less digitally savvy. Institutions should approach this decision with a clear understanding of their product distribution models, customer segments, technical capabilities, and long-term growth aspirations. By onboarding the right partners, institutions can ensure they are not just adopting a digital utility, but also enabling better and faster access to formal financial services for those who need them.

Get in touch

Contact Accion Advisory

We work to transform the lives of underserved people and small businesses around the world through digitally enabled products and services that improve financial health and resilience. If you share this vision, let us know how we can work together.