Even though Pallavi and her sister made high-quality products and had loyal customers, they found it difficult to grow their family’s textile business. Once they started working with Sub-K IMPACT Solutions, a digital finance company based in Hyderabad, India, and longtime Accion partner, they got the financial support needed to take their business to the next level. With access to digital financial services, they expanded the small shop started by their mother into three locations and began exporting materials to other countries. As their business thrived, Pallavi and her sister also turned to digital channels for other parts of their business, embracing social media to attract and engage with customers.

There has been a net increase in people, and especially microbusiness owners, using digital channels to conduct business and financial transactions. Evidence from China, Peru, Brazil, India, Mexico, Colombia, and the United States shows that demand for delivery services and e-commerce has increased rapidly to 27.6 percent globally. Despite the contraction in economic activity, GSMA reports that mobile money grew 12.7 percent — twice as fast as the forecast for 2020-2021 — reaching 1.2 billion accounts. Through our digital transformation work, part of Accion’s partnership with Mastercard Center for Inclusive Growth, we have seen a three-fold increase in digital services adoption by underserved microbusinesses in just the six months leading up to March 2022 alone.

This rapid shift to digital financial services creates a massive opportunity for financial services providers, with the lower costs afforded by digitization allowing them to reach more of the underserved. However, digital transformation requires providers to change how they think, operate, and deliver valuable services to their clients. By finding creative ways to deconstruct existing business models and reinventing themselves for the digital age, financial providers also signal to their employees an openness to more innovation in the future.

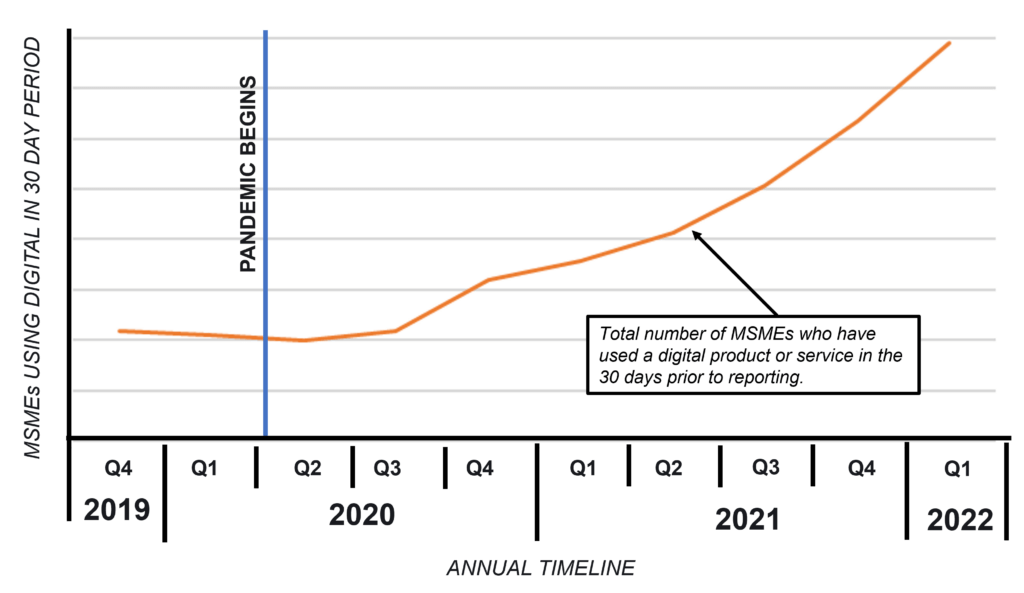

When Sub-K reinvented their digital product offerings, their clients’ digital usage increased slowly at first and then rose rapidly over the past year. Between August 2021 and May 2022, the number of clients using digital products grew by 150% and recently jumped from 52,000 unique customers in March 2022 to 72,000 in May 2022. This trend is beyond expectations and is not expected to change.

Sasidhar Thumuluri, Sub-K’s Managing Director and CEO, reflected on the initial days of this initiative, which has been a central part of the company’s digital transformation journey. When Sub-K first released their digital collections tool and other digital services for staff and clients, they were unsure about adoption. Some also worried that the front-line staff, their customer service representatives, may not see the benefits and ignore the new digital tools. With the help of Accion, Sub-K’s leadership drove this change from the top. Customer service representatives were suitably incentivized and digital KPIs were introduced for everybody, from the CEO and throughout the organization. Small successes were celebrated, and good performers were recognized and rewarded. Their initial concern proved wrong, so much so that the results took Sub-K by surprise. Not only did clients realize added flexibility and other benefits they did not expect, but the tool also saved time for the customer service representatives who supported them. Sub-K is now testing a new end-to-end digital product that will challenge the decades-old approach to group loans.

To introduce new digital solutions and experiment with agility as Sub-K did, financial providers must adapt their teams’ responsibilities and decision-making requirements. As processes and job responsibilities shift and new projects begin, teams must be clear on their new roles and deliverables and what is needed from each team to succeed.

One way to mitigate disruptions from internal changes is to formalize new, collaborative internal service level agreements between teams. These agreements, like RACI matrices, specify mutual goals and governance structures that can help align expectations, define roles and responsibilities, and foster lasting trust and collaboration between team members. These agreements should include SMART metrics to ensure transparent collaboration and enable monitoring for a successful outcome.

For employees to feel safe to be creative, take risks, and learn from their experiences, they also need psychological safety, which is essential whenever individuals face uncertainty. Any transformation leads to great uncertainty.

An example of creating psychological safety can be found in the postmortem philosophy, where a report is created after a failed test to identify objective reasons why an experiment failed rather than focus on the individual who led the test. This formal process requires the assumption of good intent, a widespread belief by leaders and their teams in the individual and their collective competency, and the expectation of high performance from everyone.

Psychological safety is the foundation of an environment that fosters creativity and learning, but diversity and inclusion bring innovation to life.

Instead of seeking consensus, organizations need to focus on bringing teams together that offer different perspectives and experiences so they can broaden possibilities, identify trends, and ultimately compete with other innovative organizations. To innovate, organizations need to think differently and be open to new ideas and ways of thinking. Meaningful innovation can only happen if there are different voices at the table.

Creating a culture of innovation is not an end game; it is a state of constant change and evolution. The digital products that are changing lives today are only the stepping stones to solutions that will shift the ways future generations experience the world. While formal, transactional changes will help employees establish new ways of working, organizations need to focus on their ability to sustain change while continuing to learn and grow.

This way, organizations can creatively destruct, reinvent, and expand the impact they have on their clients’ lives.

Where are you in your journey to create a culture of innovation? Please reach out if you are interested in learning more.

Explore More