Arpit Singh contributed to this article.

Accion Ventures has invested in lending companies for more than a decade. We have watched the industry move through multiple waves of innovation, many of which have improved outcomes for customers. India has been at the forefront of this change, yet lenders continue to grapple with rising customer acquisition costs and regulatory risk. In response, lenders are adopting more SaaS (Software as a Service) tools for internal teams — unlocking value in some cases, but creating fragmented workflows in others.

We believe that the biggest SaaS winners will not replace core systems, but will reduce structural complexity by embedding controls, improving data quality, and helping lenders evolve from fragmented multi-vendor workflows to unified, end-to-end workflows.

Unpacking the lending process + support tools in India

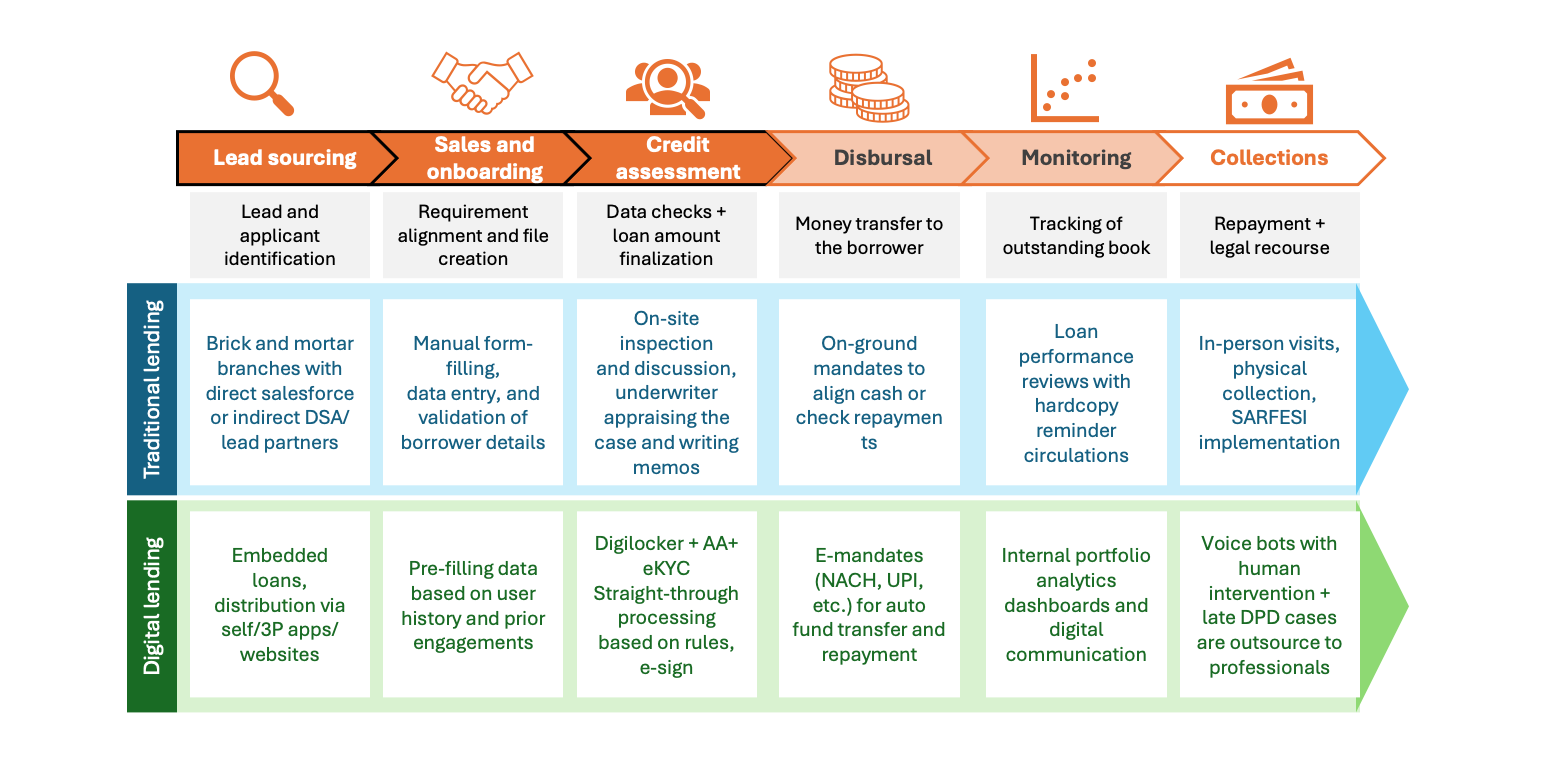

The loan journey

Lending is unique in India. The depth of lending markets, wide assortment of lending instruments, eagerness of regulated institutions to lend to emerging customer segments through frontier lending models, robust digital public infrastructure, innovative yet robust regulatory frameworks, and market size set India apart from other emerging markets. These factors lead to the industry having many unique products, complex value chains, an assortment of participants, and a robust tech stack that provides reliability at scale. At a high level, the lending journey can be broken into six stages, each varying in complexity dictated by the digital readiness of the lender.

Most lenders tend to use a phygital (blend of physical and digital) model, alternating between human discretion and digital efficiency.

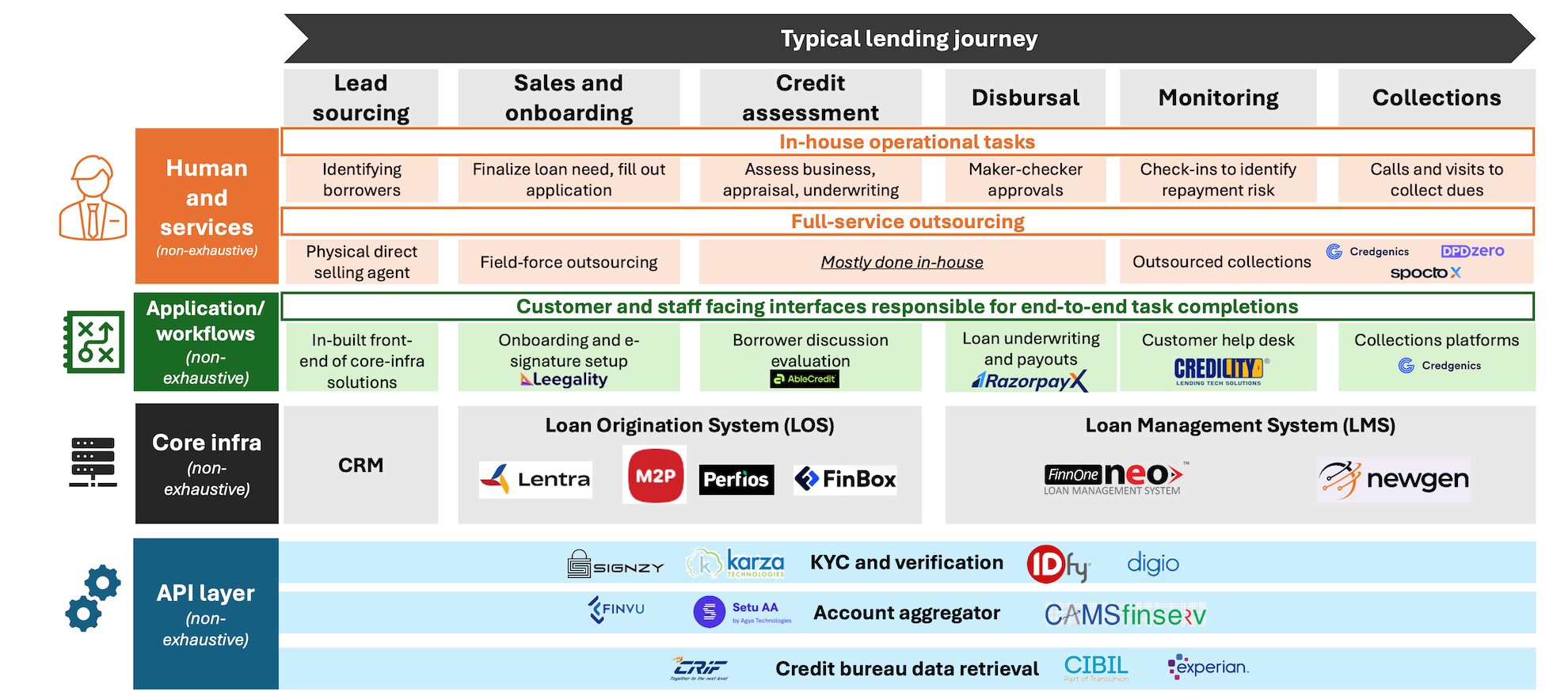

How tech caters to the journey

Because each stage in the lending journey is unique, lenders use different software to execute critical tasks. There is an interplay of three broad archetypes of solutions, which can be summarized as:

- Core infrastructure: The technical backbone of any lending system, such as Loan Origination Systems, Loan Management System, and Business Rule Engines.

- API solutions: Point solutions that cater to critical functions, such as identity verification, credit bureau checks, or bank statement analyzers.

- Workflow layer: Interfaces that handle end-to-end tasks, such as user onboarding flows and collections management.

Identifying pain points and opportunities

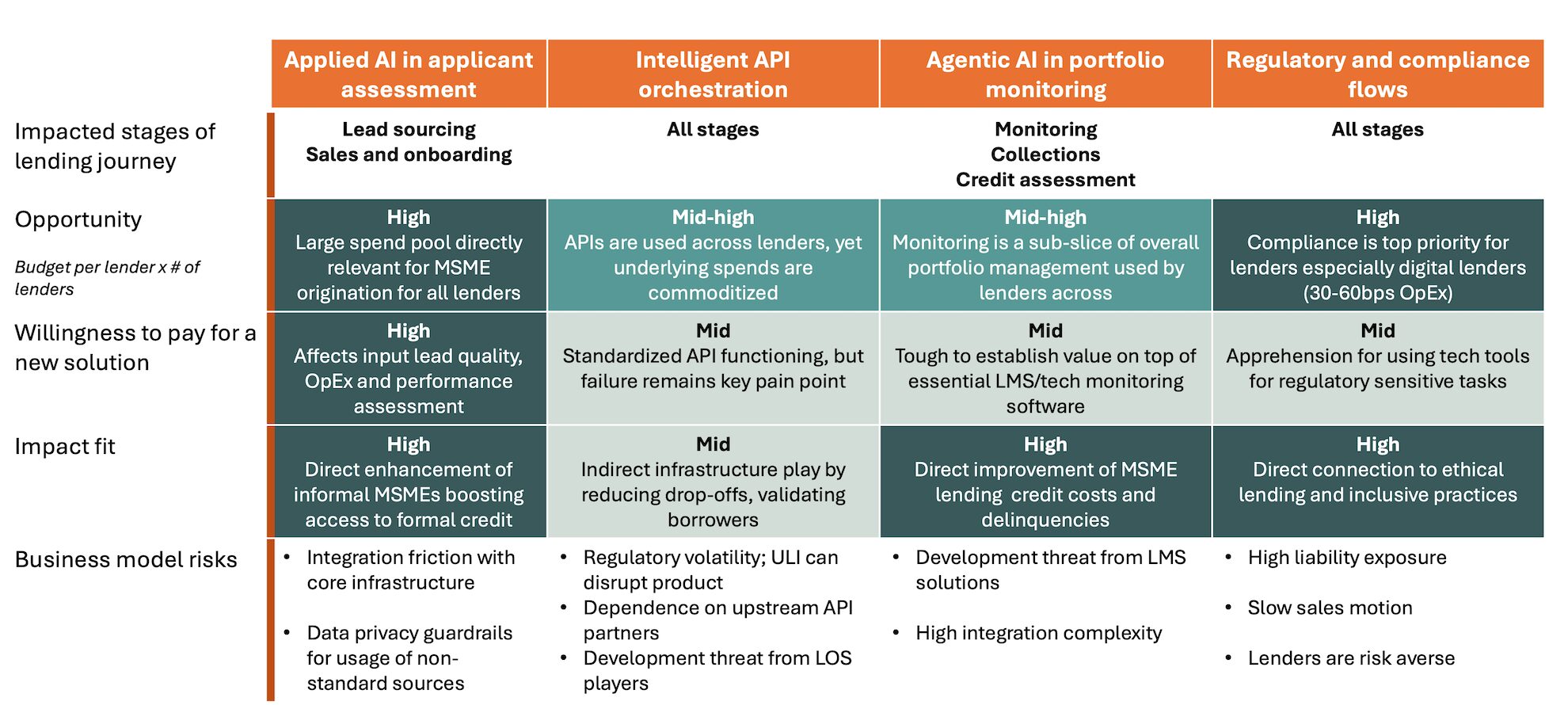

To uncover the opportunities, we identified the problems faced by lenders, the stages when these problems typically occur, and the likelihood that lenders will adopt solutions for these problems.

At a company-wide level, lenders measure any product by its impact on defined business outcomes. This focus shapes expectations — if the product does not drive material impact across a meaningful portion of the portfolio, it is unlikely to be evaluated seriously.

Problem 1: Compliance is critical and should not be an afterthought

Compliance often trails loan decisions: Requirements are treated as obligations rather than controls embedded in day-to-day operations, creating a “disburse first, fix later” pattern. Compliance teams then operate outside core lending workflows, relying on manual document preparation and inefficient filings.

This risk compounds as regulations, especially for digital lending, evolve rapidly. Knowledge remains concentrated in a small group of specialists, creating dependencies on their vigilance and institutional memory.

The result is non-compliance that is often discovered only during inspections, triggering expensive remediation and operational disruption. Over time, this reduces competitiveness through longer turnaround times, regulatory constraints, and reputational damage.

The fix: Solutions that embed compliance into origination-to-collections workflows can reduce audit findings and remediation costs while improving turnaround time for compliance fixes.

Problem 2: Borrower data has improved, but capturing complete data is still difficult and leads to customer drop-offs and delinquencies

Borrower assessment today depends on in-field evaluation and backend data pulls. Credit officers conduct field visits to capture context (business activity, borrower behavior), while APIs fetch bureau scores and bank statements that feed scorecards and the underwriting process.

While this looks seamless on paper, execution depends heavily on officer skill and one-time snapshots of borrower information. Field officers vary in experience and training, leading to errors in capture and interpretation, creating inconsistency in borrower profiles. API failures also create real field cost — distances are large, time is scarce, and revisiting a customer can be prohibitive. Finally, commoditization and overcrowding among API vendors can disincentivize meaningful innovation, reinforcing a vicious cycle.

Together, these issues make origination fragile. Despite spending over 50 percent of operational expense on sales, according to internal research and benchmarking, lenders still face declining lead quality and a high-churn sales force. The result is drop-offs during underwriting — or worse, higher delinquencies — while weak documentation makes it difficult to retrace credit decisions and identify root causes.

The fix: Data capture workflows that leverage real-time nudges to improve completeness and consistency at the point of origination can reduce underwriting drop-offs and downstream delinquency.

Problem 3: Technology pricing appears transparent, but true cost-of-ownership is high.

Many tech vendors promote transparent pricing, such as pay-as-you-go or fixed subscriptions. In practice, these tools wrap core infrastructure that remains deeply embedded and is commonly priced via annual contracts or assets-under-management–linked fees.

Because switching core infrastructure is costly, most changes happen at the periphery. But peripheral tools still need to integrate with the core via APIs, and even small changes can require expensive change requests (CRs). Over time, these CRs accumulate across the lender lifecycle and turn incremental improvements into uncontrolled costs.

In practice, we see lenders spend up to 60 percent of their technology spend on core systems. As complexity rises, operations get pushed to field teams as manual workarounds. In a market that rewards speed, this setup punishes experimentation: each new integration intended to unlock efficiency can trigger prohibitive CR cost.

The fix: Integration and orchestration layers that cut CR cycles and lower integration effort can shorten time-to-launch for new products while reducing total vendor and engineering cost.

Problem 4: Passive portfolio monitoring is no longer sufficient to manage ever-rising fraud

Most lenders rely on risk-containment teams to track portfolio quality by polling loan-management systems for flags and early warning signals. Field collections teams relay on-ground borrower developments to capture qualitative signals that do not show up in documents, bureau pulls, or bank data.

This workflow breaks with the rising pace of disbursals. Recurring manual reviews lead to reactive corrective actions for changing collections strategies and loan documents. This results in limited real-time feedback loops between collections and originations, leading to delayed refresh in sourcing criteria or pricing decisions. Persistent asset quality weakens the credibility of lenders, leading to tighter funding and, therefore, a higher cost of capital that hampers growth.

The fix: Continuous monitoring and early-warning SaaS that connects servicing signals back into underwriting can reduce fraud loss and improve portfolio performance at scale.

Our perspectives on opportunities ahead

We continue to be driven by our thesis as we look for opportunities to build within these identified problems. Firstly, we care deeply about solutions that deliver lasting impact to the underserved people. Secondly, we believe that gauging willingness to pay is an excellent proxy for identifying the cross-section of product-market fit and price, and thus the likelihood of a product’s success. Lastly, we continue to keep a keen eye on risks that affect the models that interest us.

We’ve identified these opportunities to solve challenges along the lending journey:

Complexity in India’s lending SaaS is a structural problem – it won’t simply go away with time. Siloed data, regulatory flux, and manual inefficiencies will continue to evolve, presenting openings for improvement. As India and other markets start to adopt a wider variety of tools and AI solutions, we see an opportunity to identify whitespaces ahead of the curve. We believe our learnings from India on building vertical fintech SaaS, such as identity, onboarding, data enrichment, and collections solutions, can be adapted to other emerging markets where we are seeing the mushrooming of such SaaS solutions.

The next generation of fintech SaaS will not win by replacing core systems or replicating APIs, but by navigating complexity: enhancing human judgment and stitching disjointed steps into measurable workflows. The best teams building in this space will speak the lender’s language, understand the lender’s cost structure, and translate deep operational insight into durable products with real impact.