As the recovery from COVID-19 begins, financial inclusion has never been more urgent. Low-income people around the world have lost their jobs or businesses, and the World Bank projects that the pandemic will push 100 million people into extreme poverty. Vulnerable populations direly need financial tools like savings, credit, and insurance to rebuild their livelihoods and build resilience to the challenges of today and those to come. Financial institutions have a critical role to play in supporting the most vulnerable and equipping them with the tools they need to enter the digital economy.

The pandemic and social distancing have dramatically increased the urgency for innovative and relevant digital solutions to meet the new and evolving needs of vulnerable populations. For many people visiting their local bank branch was unsafe or not feasible during lockdowns, and as economies begin to open, many people have begun to expect the convenience, speed, and affordability digital transactions can bring. To effectively support their clients and reach new populations in an increasingly digital environment, financial service providers (FSPs) need to digitally transform. Many microfinance institutions are built on low-tech, high-touch models designed decades ago to reach millions of low-income clients. Now, these FSPs must find digital ways to reach and interact with their customers efficiently and at scale, use their client data for more efficient credit management and product design, and build more flexible core systems that support adaptability. This requires FSPs to coordinate across every aspect of their business to achieve a fully digitally enabled business model.

FSPs must find digital ways to reach and interact with their customers efficiently and at scale, use their client data for more efficient credit management and product design, and build more flexible core systems that support adaptability.

Through our work with FSPs and their clients, we uncovered six key strategies that financial inclusion-focused institutions need to keep in mind as they progress down the path of digital transformation:

Six strategies to scale financial inclusion

Financially underserved individuals and businesses have varying levels of digital maturity, attitudes, and behaviors. Some segments may not have internet or smartphones, or simply do not trust digital financial services due to unfamiliarity or privacy concerns. Other segments may be early adopters of technology-enabled services and conduct their lives through their phones. FSPs can use their digital transformation efforts to reduce, rather than exacerbate, the existing digital divide by developing clear value propositions to help customers run their businesses better. FSPs can more effectively attract and retain clients by designing for both sides of the digital divide and balancing tech and touch strategies.

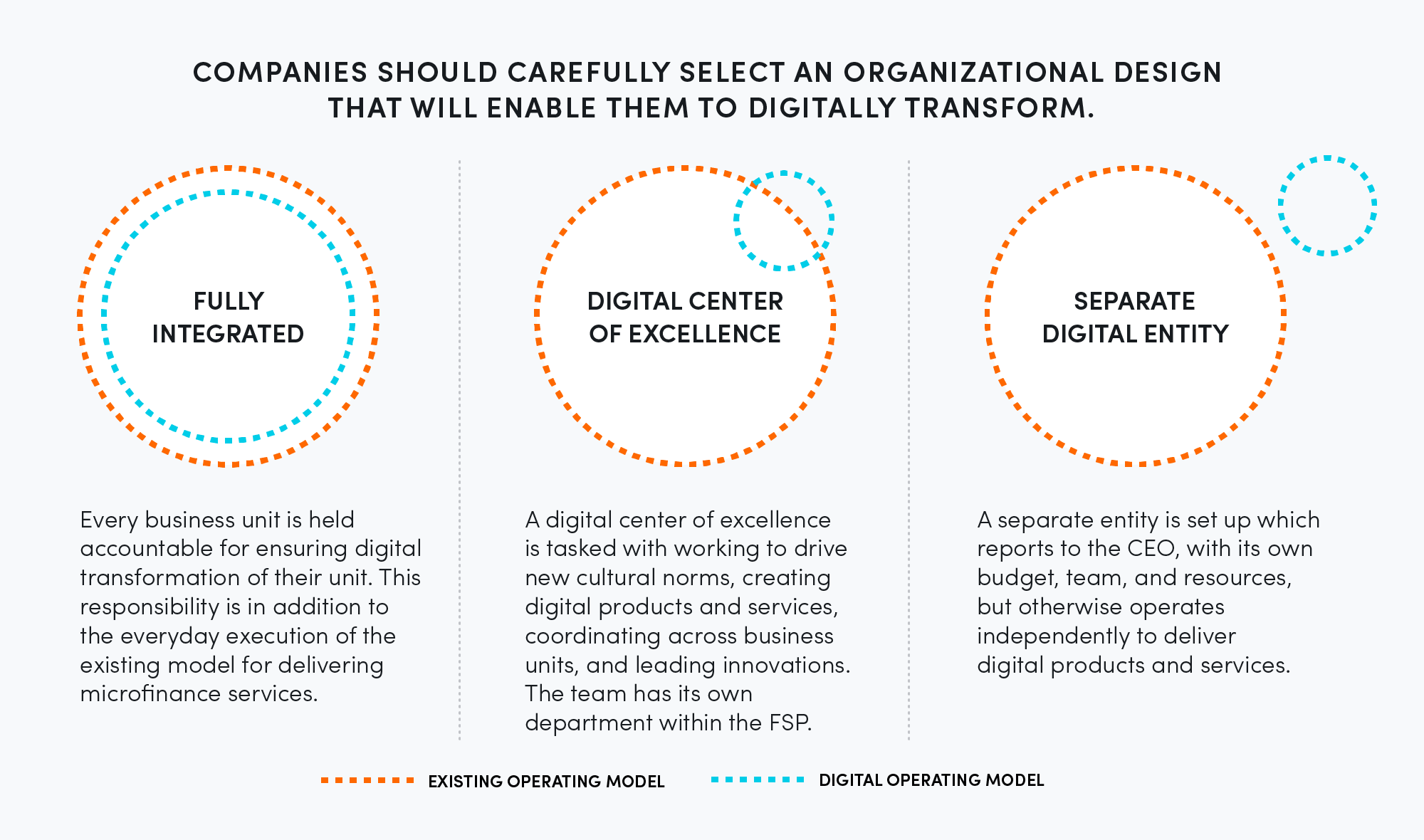

Traditional microfinance institutions are radically different than digitally native financial companies in their ethos, culture, and organizational design. The digital transformation of microfinance institutions requires developing a plan and implementing it simultaneously, and therefore also requires careful thought about how to integrate two very different operating models, one digital and one not, under one roof. There is no one right way to organize for digital transformation, and how an institution decides to organize depends on their starting point, their digital maturity, and their desired end state. Organizations can choose one of three paths: (1) a fully integrated holistic digital transformation where all departments have collective responsibility for transformation; (2) a digital center of excellence that sits within the organization and is responsible for driving digital solutions; and (3) setting up a stand-alone unit that builds, tests, learns and launches products outside the FSP’s existing business operations.

Many financial institutions tend to focus on short term goals and quarterly targets. Typically, key performance indicators (KPIs) are not designed to encourage risk and innovation. However, digital transformation requires a culture that is willing to experiment, learn what works, and innovate. This requires institutions to seek alignment and buy-in on organizational priorities across the organization: the board, C-suite, management, and field staff. The development of a safe space to fail encourages a test-and-learn approach that is essential to growth as an organization.

Data strategies are often implemented in isolation from the business and analysis is not articulated in a way that empowers and enables the core initiatives of the business — including creating greater customer value, creating process efficiencies, or making meaningful product updates. But when aligned with the core business, having a data plan and fleshed-out data capabilities are key to creating business value through greater understanding, alignment, and actioning of both digital and offline data. Institutions can harness the power of data in their digital transformation by deriving greater value from the data they already have, taking action based on insights, and prioritizing the management and governance of data to ensure it is used effectively and responsibly.

Microfinance organizations often struggle with legacy technological systems, which have monolithic designs and are written in dated programming languages. These systems are inflexible, unable to support innovation, and can introduce security concerns. Digital transformation must be built on solid technological foundations. The more digital an organization becomes, the more it needs to invest in building future-proof and resilient platforms that can easily connect to cloud and open APIs. This requires balancing their long-term vision and short-term agility and ensuring backup and disaster recovery on the cloud, where possible. Cybersecurity will increasingly be a key area for investment to prevent attacks on the digital channels and systems.

Potential partnerships that can support financial institutions’ business goals often fall through due to a lack of a clear business case that aligns the goals of all parties, as well as questions that arise regarding ownership of the customer relationship. But partnerships with institutions such as telecommunication providers, ecommerce players, digital payment providers, or fintechs can enable new ways to leverage data, evaluate risk, and reach new customers at scale. Partnerships expand financial inclusion by building a digital ecosystem and a deeper integration with the formal financial services industry. To realize these benefits, FSPs should seek win-win partnerships and expand their definition of a partner.

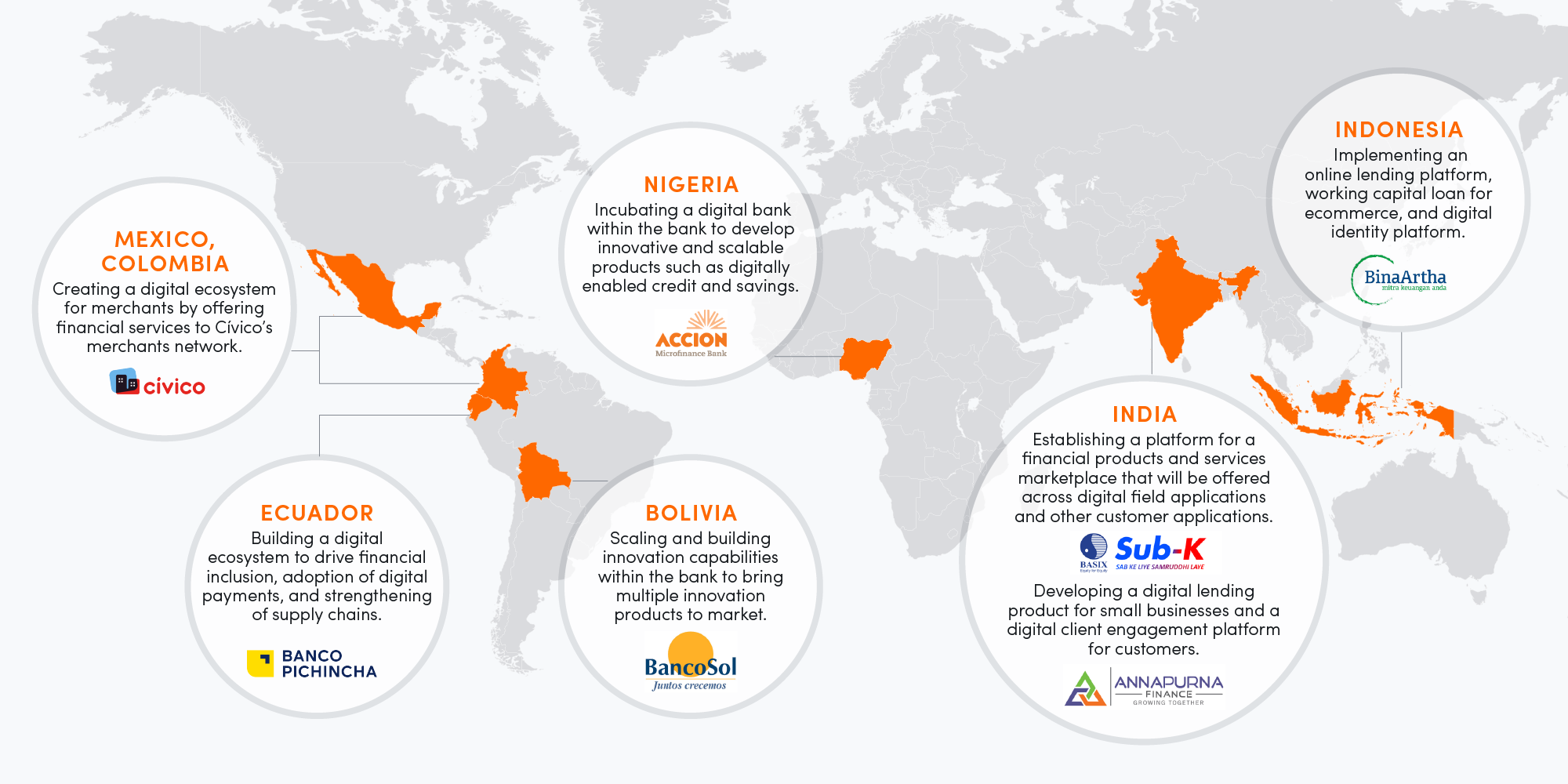

This paper unpacks each strategy through real examples of our implementation experiences across FSP partners.

Sub-K client Syed Saber in Hyderabad, India.

Introduction

Digitizing swiftly and effectively is vital for FSPs to successfully and responsibly serve their customers at scale and to remain competitive in the face of many digital challengers entering the market. But most FSPs face challenges that make transformation difficult, including a lack of resources, heavy reliance on manual processes, difficulty attracting technical expertise, and poorly organized customer data. This leaves many organizations asking: is our organization ready to undergo a digital transformation? What are the drawbacks or risks to consider before we dive in? Where do we start?

To help FSPs navigate these questions and enable millions of underserved micro, small, and medium enterprises (MSMEs) to enter the digital economy, Mastercard and Accion launched a first-of-its-kind partnership in 2018 that unites our worldwide networks and resources to support the digital transformation of FSPs around the world, as well as the millions of customers they serve. In our first two years of work, we have guided FSPs’ progress on digital transformation and helped them develop digital tools to reach more small businesses and individuals and serve them more effectively. In 2020, as COVID-19 first spread across the world, we helped our partners leverage digital tools to respond to the crisis. This included reimagining group and individual lending for a no-contact world, enhancing digital channels, and rapidly implementing remote customer service. As digital platforms become more pervasive, accessible, and affordable, MSMEs can leverage digital tools and products to rebuild and relaunch their businesses — and in some cases, digitally transform themselves.

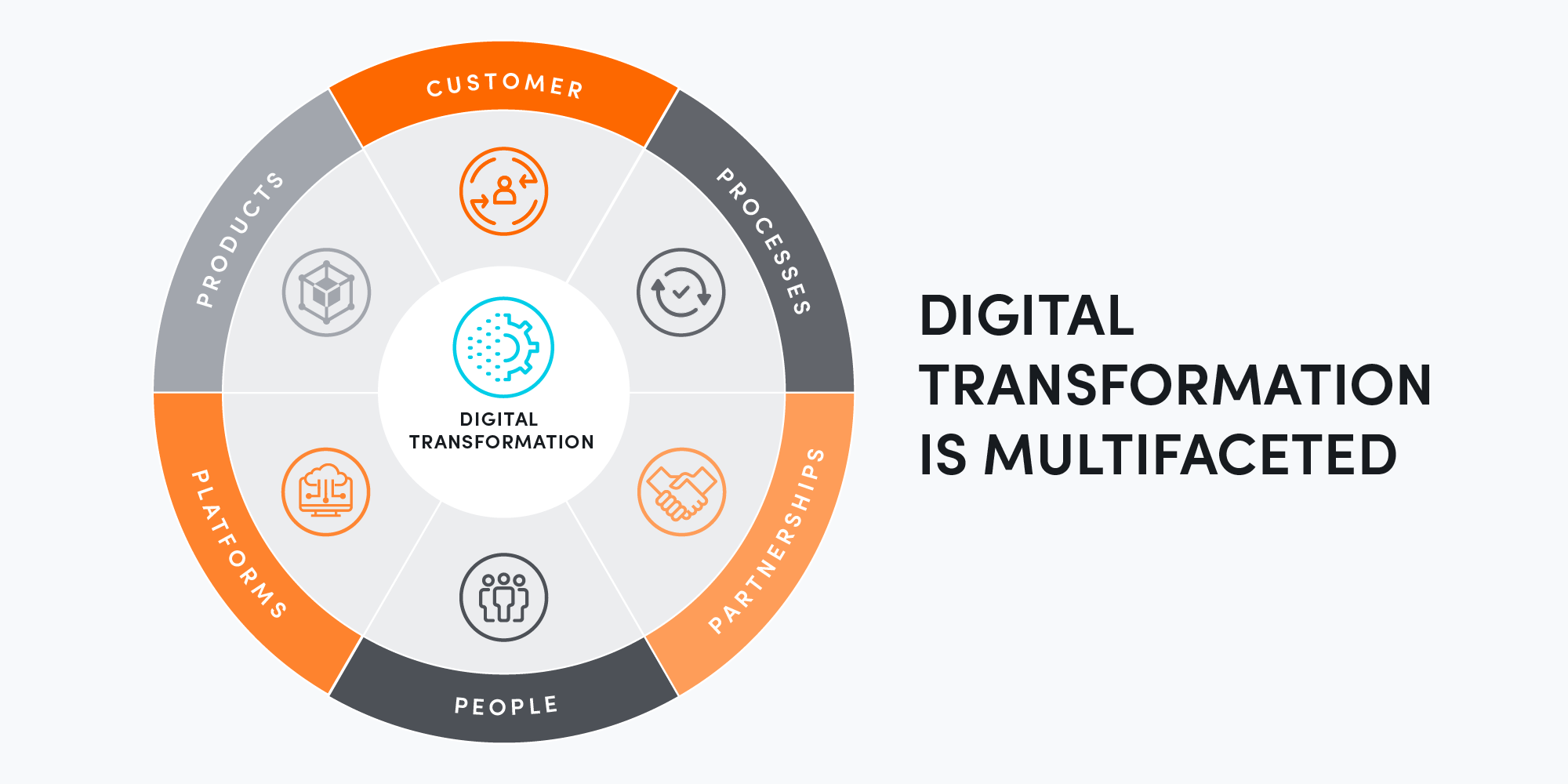

We recognize that digital transformation is a journey, not a destination. Our partners have travelled far, but their journeys are not complete — and will likely include some obstacles ahead. In this paper, we share learnings from the first two years of working with institutions to navigate their digital transformation efforts, across every aspect of their business: the customer, processes, partnerships, people, platforms, and products, to achieve a fully digitally enabled business model.

There is no single path to digital transformation, nor is it a one-off endavor.

This paper shares our challenges, frustrations, and successes, and also builds on lessons from other ongoing digital transformation efforts around the world. Going forward, we will continue to share lessons as our partners digitally transform and begin to realize the return on their investments.

We hope that the initial lessons shared here will help FSPs start their digital transformation journeys and maintain the momentum needed to succeed. We also hope this paper will demonstrate to the financial services industry at-large the impact that digital transformation can have in supporting the resilience of low-income people.

An oft-repeated point that bears repeating here: digital transformation is a massive exercise in culture change. It is complex and multi-faceted and requires solid commitment to evolve the core business model from the board all the way down to loan officers. There is no single path to digital transformation, nor is it a one-off endeavor. We believe the goal of digital transformation is not to achieve the same status as a digital-first company, but rather adaptability and an enduring culture of innovation and learning, so that institutions can respond rapidly to changes, challenges, and opportunities as they arise. As Charles Darwin argued, “survival of the fittest” refers not to being the strongest or fastest but being most adaptable to change.

Ibu Oom Rohmayato, a client of Bina Artha Ventura (BAV) in Majalaya, Bandung in West Java, Indonesia.

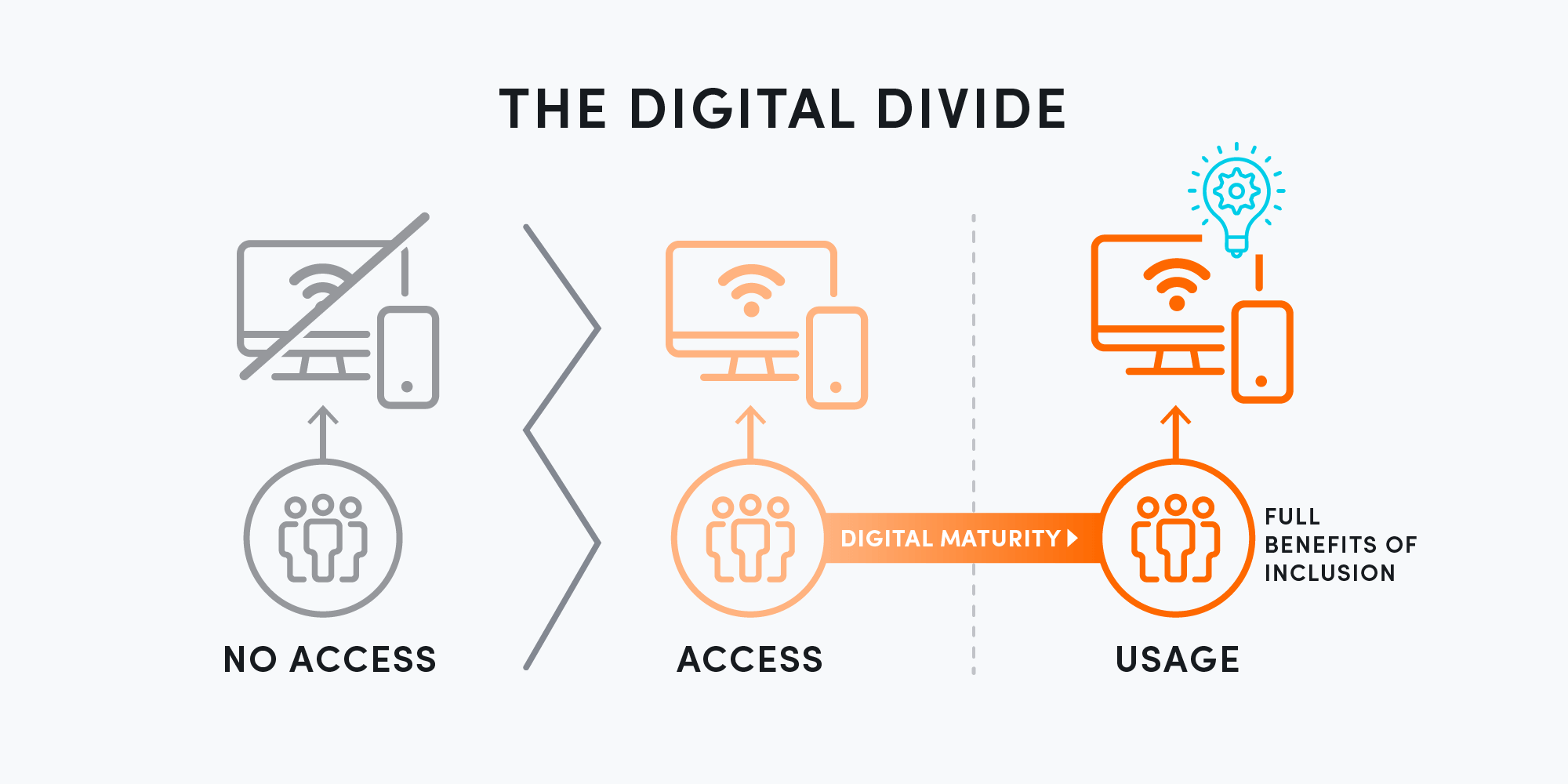

Combat the digital divide on multiple fronts

The COVID-19 pandemic has catalyzed the digital transformation of FSPs, especially those reliant on high degree of face-to-face interaction, like microfinance institutions — and expanded digital financial services holds the promise of greater financial inclusion. But with all the enthusiasm around digital transformation, there is little attention paid to the ways this can lead to financial exclusion. Financially underserved and excluded individuals and businesses represent a diverse set of digital maturities, attitudes, and behaviors. For example, some customers may not have access to the internet even if they own smartphones, others may not feel comfortable conducting financial transactions on a mobile device, and yet others may simply prefer to work directly with a person when conducting financial transactions. FSPs must be careful to ensure that digital transformation is not exacerbating an already pervasive digital divide. For example, the digitization of many government cash transfers during the pandemic has been particularly useful to reduce in-person contact while still providing critical economic relief. However, some reports have highlighted the exclusion of beneficiaries, especially women, who often lack access to the digital and financial tools needed to navigate the system of government to person (G2P) payments.

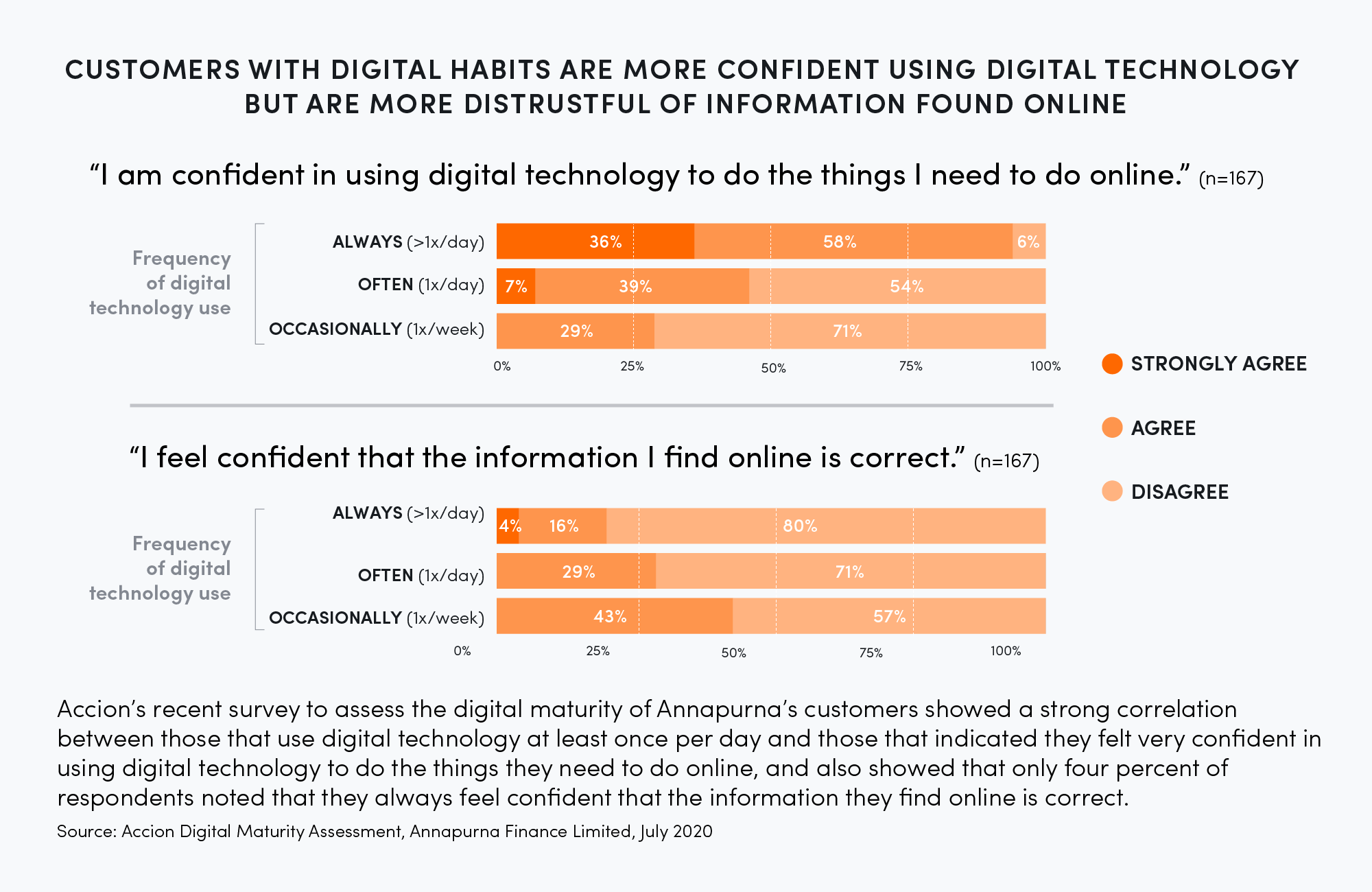

Therefore, we consider two aspects of the digital divide: first, the gulf between those without access to computers, smartphones, and the internet, and those with access, and second, the spectrum of varying digital maturities in terms of trust and comfort with, usage of, and capability to fully enjoy the benefits of digital inclusion. Based on recent analysis conducted by GSMA, in low-and-middle income countries, demographics play a key role in determining access to smartphones and usage of mobile internet. Individuals in rural areas, those with lower incomes, and those that have only completed primary education are less likely to own a smartphone or use mobile internet. On top of this, women are less likely than men to own a mobile phone or use mobile internet, even when other relevant socioeconomic and demographic factors are controlled for. For those that do have access to digital tools, results from an Accion survey of Annapurna clients demonstrated that there are several determinants of how comfortable a person feels using these tools. This includes both trust in digital channels and simply whether they are in the habit of using digital tools.

Digital channels offer some of the most effective ways to reach those that are financially excluded, especially while social distancing orders and lockdowns remain in force. We are already seeing that COVID-19 has accelerated digital adoption and has forced some previously reluctant consumers to overcome barriers around trust and tech-savviness because they have few other options. Among our partners, we’ve seen acceptance of digital payments increase 106 percent from December 2019 to September 2020 as microbusinesses move online. However, growth has been concentrated among partners who had digital infrastructure in place prior to the pandemic.

This underscores the pervasive digital divide among low-income people and businesses. Clearly, an undifferentiated focus on digital channels alone is not sufficient to bring useful financial tools to the underserved in a way that promotes trust and comfort. Accion Venture Lab’s 2018 report on the “Tech Touch Balance” demonstrates the importance of continued human interaction in delivering financial services to the poor to build trust, establish relationships, and engage customers. Especially now, in the wake of COVID-19, low-income and vulnerable segments need the support of FSPs to navigate the new normal, restart their businesses, and build financial health so that they can build resilience to future crises and ensure they are not left behind again.

FSPs should be deliberate and thoughtful about how they reach clients on both sides of the digital divide. While they should lean into digital channels when undergoing digital transformation, they should also continue to leverage physical networks (branches, loan officers, groups) to promote greater digital adoption. The percentage of women actively using the digital products and services supported through Accion’s partnership with Mastercard has increased over one percentage point between September 2020 and December 2020, which illustrates the effectiveness of the combined recommendations below in moving us in the right direction to address the persistent gender gaps in digital financial services.

When you try to digitalize the process for the clients — when you try to make clients adopt digital means — things become more complicated because we need to make sure that the client is at the center of the change… that it is benefitting and enriching the life of the client.

Christian Banno, Chief Business Officer of CASEA and board member of BAV

FSPS CAN ADDRESS THE DIGITAL DIVIDE IN MANY WAYS

Build a value proposition for digital products

Banco Pichincha is the largest financial institution in Ecuador, with a 115-year history and a deep commitment to its customers. The bank is undergoing a complete, large-scale digital transformation, not only to build their own technological capabilities, but to improve its relationship with its customers and to be better able to respond to their needs during tough times. The COVID-19 pandemic has accelerated their digital transformation and improved the uptake of digital channels among their entire client base. In 2020, Banco Pichincha’s mobile app went from having 650 thousand to 1.1 million customers and 50 thousand customers managed the disbursement of their loans entirely through digital channels. Their recently launched Billetera deUna! application, a mobile wallet that supports secure, real time payments for their customers, has been downloaded more than 118 thousand times. While they have seen significant adoption of digital channels, it has primarily been among high-income segments, while uptake has been much lower among merchants and consumers at the base of the pyramid.

For customers accustomed to using cash and that enjoy the tangibility it offers, the value proposition of digital is difficult to communicate – particularly when relying on cash is perceived as free and more secure.

Accion and Banco Pichincha are working together to promote financial and digital inclusion in Ecuador, and one of the first key actions of the project was to identify the key adoption barriers for the Billetera deUna! mobile wallet through an analysis of the payments ecosystem and conversations with clients and field staff. Nearly eight in 10 Ecuadorians have mobile phones, but only 32 percent of those with mobile phones are currently using their phones to make digital payments, and cash still accounts for about 40 percent of payments, particularly in rural communities. The use of digital payments can help small merchants gain more access to credit, formalize, grow their business, reduce time required for reconciliation and risk of theft, and save them multiple trips to the bank to deposit cash. However, for customers accustomed to using cash and that enjoy the tangibility it offers, the value proposition of digital is difficult to communicate – particularly when relying on cash is perceived as free and more secure.

Using this information, Banco Pichincha has reimagined the user experience for underserved microbusinesses by addressing the barriers to adoption with a clear and compelling value proposition. In parallel, the bank is using Accion’s EdTech platform, Ovante, to support their microfinance customers’ digital literacy.

A wallet that can be used for payments and that clearly meets the needs of a small merchant will enable them to build financial resilience, operate digitally where social distancing is still required, and participate in an increasingly digital ecosystem. Being clear about how digital will benefit small merchants specifically, in messages that resonate with them, can thus help overcome any initial barriers to adoption.Using this information, Banco Pichincha has reimagined the user experience for underserved microbusinesses by addressing the barriers to adoption with a clear and compelling value proposition. In parallel, the bank is using Accion’s EdTech platform, Ovante, to support their microfinance customers’ digital literacy.

Design for both sides of the digital divide

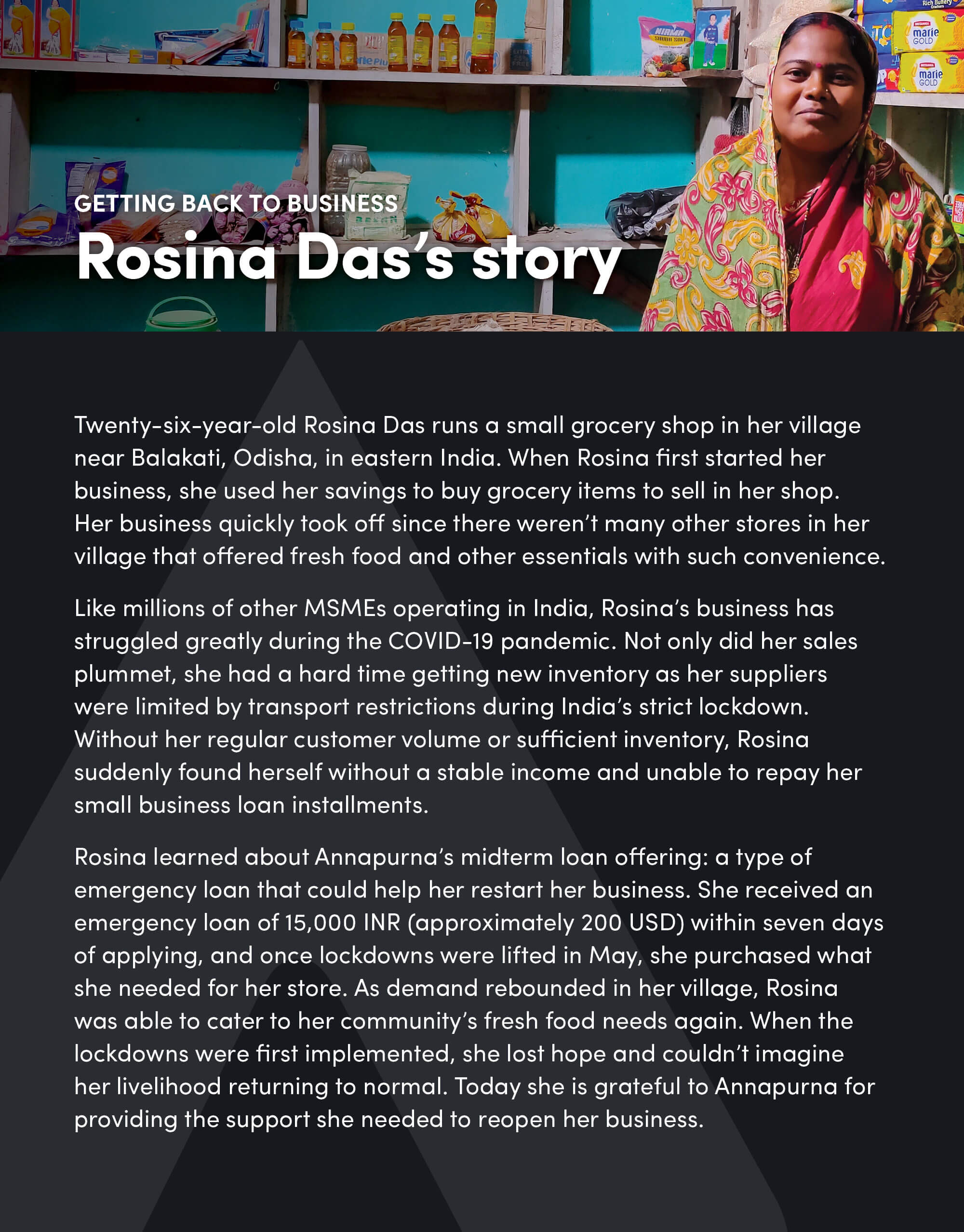

Annapurna Finance Limited, headquartered in Odisha, India, serves 1.9 million individuals in eastern India who would otherwise lack access to high-quality financial services. More than 99 percent of these individuals are group lending customers. When lockdowns due to the pandemic put an end to group meetings, this created a challenge for the members that depended on meetings to access much needed finance, especially during one of their most difficult times of need. Responding quickly to the crisis, Accion worked with Annapurna to reimagine their group lending process and supported the creation of a new digitally accessible emergency loan product for clients to help them manage liquidity constraints or any other financial emergency.

Though Annapurna is interested in developing more smartphone-based lending solutions, only 10 percent of their group lending customers currently own a smartphone. However, a greater percentage had access to less advanced feature phones. To address the digital divide, we created an SMS-based digital loan product that incorporated both tech and touch. Interested customers can provide a few details to their loan officer to ensure they meet the qualifications. If qualified, the loan officer can make an emergency loan limit available to them up to a pre-defined amount. Once this limit is created, a customer can access the funds at any time by simply sending an SMS to a dedicated phone number, which would result in the money being disbursed to the customer’s loan account.

We designed the solution to enable an easy upgrade to a smartphone version when relevant for their customers. Accion’s digital maturity assessment of Annapurna’s customers found that customers who use a digital device more than once per day are more than three times as likely to feel confident in using technology for different purposes and exhibit a greater willingness to try new products in the future. Therefore, Annapurna’s feature-to-smartphone product roadmap will allow customers to increase their digital maturity over time.

On the opposite side of the digital divide, Annapurna found that the more digitally mature segment of their MSME clients that have individual rather than group loans were interested in greater convenience and wanted to be able to move away from having to visit physical branches. Annapurna knows that they need to digitize even faster for this segment and we are supporting the bank to develop an end-to-end digital loan that clients can apply for without needing to speak directly to a loan officer and through which all repayments can be made remotely.

Balance tech and touch to bridge the digital divide

FSPs can do many things to ensure that customers get the human touchpoints they need to feel supported and engaged. For customers with low digital maturity, such as group lending clients who traditionally rely on high-touch models of interaction, institutions should think strategically about hybrid models that leverage digital to automate manual processes while still maintaining the human touch that customers value.

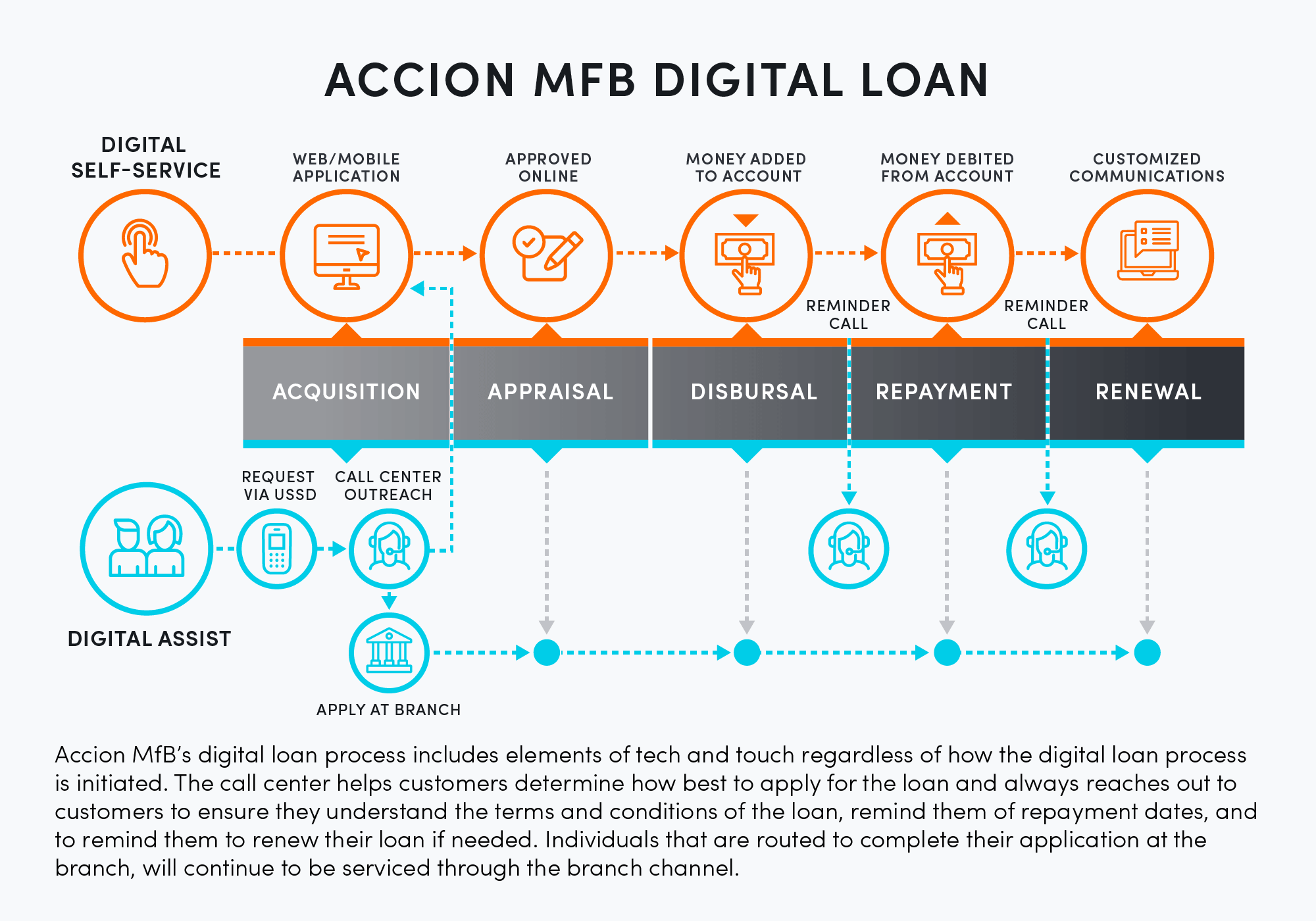

Accion Microfinance Bank (Accion MfB), one of Nigeria’s most successful microfinance institutions, is seeking to make digital the new norm and encourage digital behaviors in their client base. As part of this goal, they made the end-to-end application process for their new digital loan accessible only through mobile app or the web portal. But Accion MfB knew that not all their customers are ready for a fully digital process end-to-end, so the product was designed so that customers can initiate the digital loan application process with Accion MfB through several different channels. Customers can submit a request for a digital loan application via USSD mobile codes, which prompts the call center to reach out to better understand their characteristics: Do you have the documentation needed to apply digitally? What is your comfort in completing the application form online? Based on answers to these questions, the call center agent may direct applicants to one of the self-service channels to complete an application, or may refer applicants to a branch where a staff member can assist with a loan application.

Customers who completed the digital loan application but were denied were redirected to a branch so that they could reapply using the traditional application process. Interestingly, the Accion MfB team found that some of the customers who were denied a loan using the digital process were approved using the in-person process for the same loan amount. After digging into the data, they found that customers were responding to questions on the digital loan application differently than they did in the in-person loan application process. It seemed that some customers were misinterpreting the questions on the digital loan application. When they were face to face with someone who could ask the same questions in several different ways, offer clarifications, or suggestions, the number of errors greatly reduced. For example, when asked about their revenues, they may have entered revenue for the day rather than the month. Given this finding, Accion MfB made several changes to the digital loan application to incorporate this human element. They changed how many questions were phrased to more closely resemble how an account officer would ask them, and made more help, examples, and tips available.

As a street vendor, Tamar Kumar Prahan struggled to provide for his family during India’s lockdown. A loan from Accion partner Annapurna Finance helped him restart his business.

Optimize organizational design

Most microfinance institutions were built to be high-touch businesses, focused on meeting the needs of their customers through replicable processes conducted face-to-face and mostly in cash. Technology has helped automate some processes, such as field staff tools and credit risk decisioning. While this model worked well in ensuring that some underserved populations get access to the responsible finance they need, the heavy reliance on loan officers and physical branches results in higher costs and limits scalability.

The digital transformation of financial service providers requires careful thought about how two very different operating models, one current and one future state, should be integrated, under the same roof.

A purely digital financial services model — with remote application, application processing, approval, and digital transactions — is very different than the high-touch model of traditional microfinance institutions. When a microfinance institution is restricted only by a customer’s access to the right type of device and access to a mobile network, the potential for scale is massive. However, this newer model is diametrically opposite to the historical one in terms of ethos, culture, and style.

The reality for FSPs serving the underserved is that some of their customers do not yet have access to digital devices or a mobile network and will continue to require the high-touch service offered through the traditional microfinance model. Other customers, becoming more accustomed to transacting digitally in other areas of their life, are demanding the accessibility, convenience, and speed of service that digital financial services can provide. Therefore, the digital transformation of financial service providers requires careful thought about how two very different operating models, one current and one future state, should be integrated, under the same roof.

There’s no one right way to organize for digital transformation, and what it looks like can be very different from one organization to the next. A lot depends on the starting point — the as-is digital maturity of the institution — as well as the desired end state.

Some companies may want to integrate digital processes across all departments from the start.

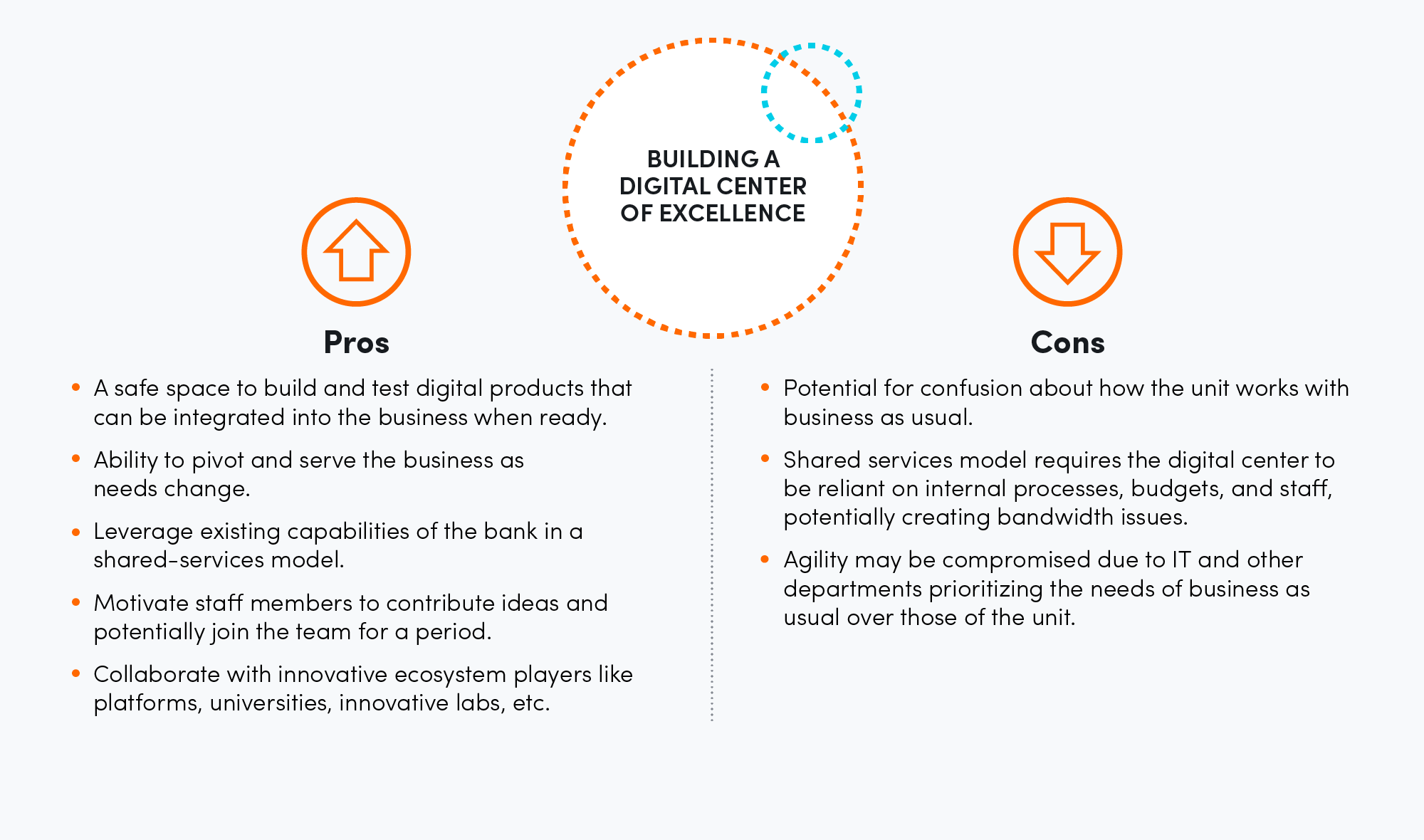

Others may create a digital center of excellence, like an innovation lab, within the organization that is tasked with creating products that serve the institution’s client base.

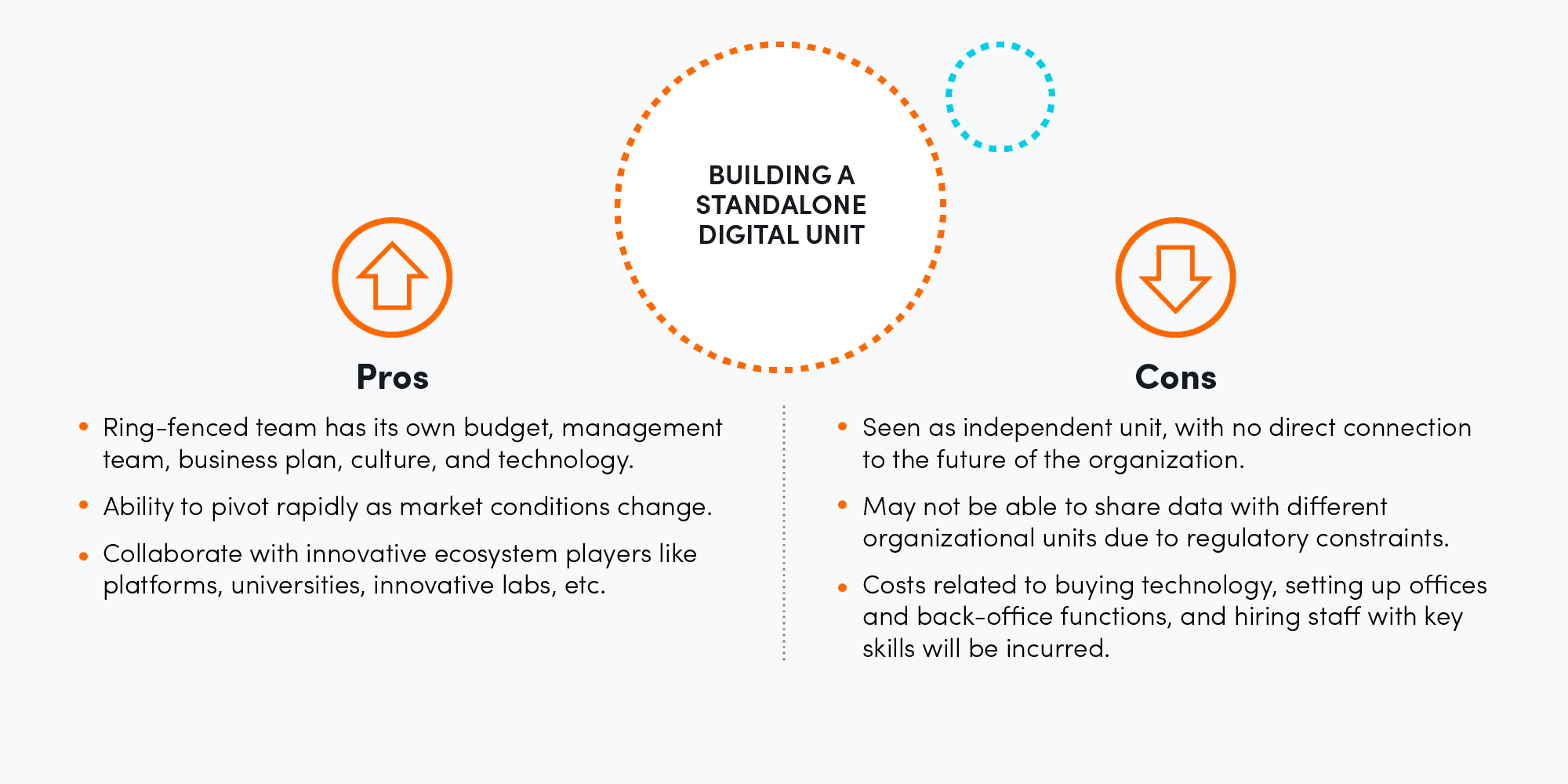

And finally, others may decide to create a separate unit or even a wholly owned subsidiary to experiment in a controlled environment and ensure little or no impact on business as usual.

For an organization to determine the best model to start with, they should consider the following dimensions:

Target customer segment: An institution should determine whether they are primarily focused on creating new products for new market segments to expand their reach, or on transforming existing products for existing market segments in order to serve them more efficiently. Those looking to serve new customer segments should look to create some separation between their existing and digital operating model.

Macro-level factors: Factors such as access to talent, potential for partnerships, level of digital readiness in the country, level of investment in digital transformation, and competitive landscape play a role in determining organizational design.

The level of disruption faced by the business: Often, a fully integrated digital transformation model takes more time and can create major distractions for business as usual. The higher the potential for disruption, the better to keep the digital unit separate until a point of maturity.

The level of digital maturity: The earlier a company is in its digital evolution — including digitally enabled processes, skills, and infrastructure — the more likely it is to need a bit of separation from standard operations to concentrate digital skills and move quickly.

Openness to change: Companies that have a more resistant or traditional culture usually fare better with a separate unit that is solely focused on digital evolution.

It is important to remember that organizational design can and should change over time. For most companies, having the dedicated focus of a separate or semi-integrated digital unit may make sense when starting on the journey — but over the longer term, they may want to ensure that digital capabilities become embedded across business lines. We took variations of the fully integrated digital transformation and digital center of excellence approaches with each of the FSPs we worked with as demonstrated by the examples below.

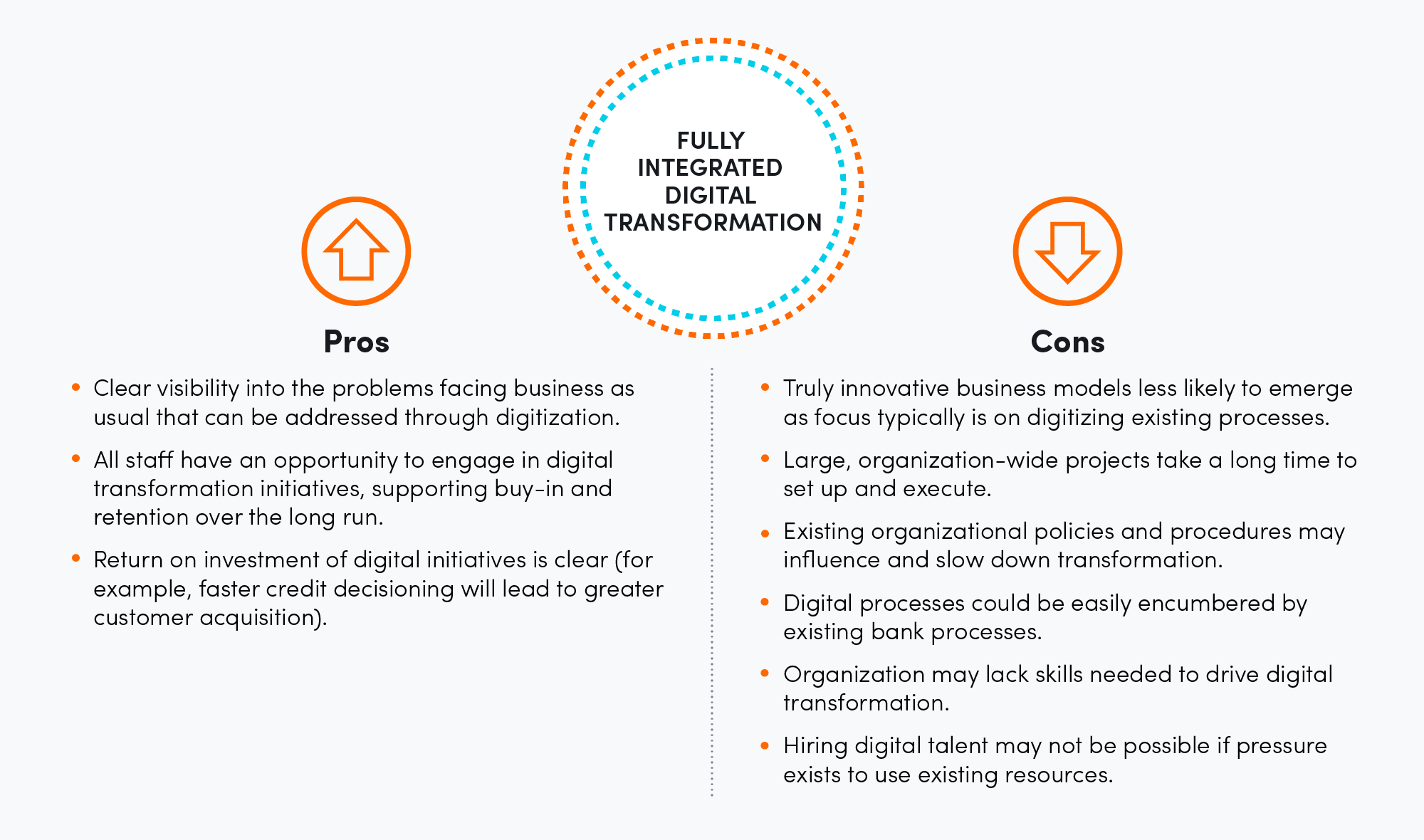

In a fully integrated digital transformation model, digital capabilities and processes are integrated across business lines and all business lines have a responsibility to drive business agility, growth, and innovation.

Sub-K IMPACT Solutions Ltd., a banking correspondent company focused on reaching underserved populations in India, started their digital transformation journey from a relatively high level of digital maturity, and with a clear understanding of where they wanted to go with a digitally enabled model.

The team socialized digital transformation across the entire organization, utilizing town hall meetings with those at headquarters and in the field to discuss the importance of digital. They trained nearly all staff to adopt a digital-first approach to customer acquisition, application processing, account servicing and collections and put in place KPIs to drive forward a digital operating model. They also created several working groups with members from product, data strategy, training, compliance, marketing, call center, and agent networks to ensure that the existing assets and infrastructure of the institution could be completely leveraged to offer a distribution model for digital products. These cross-functional teams work together to develop and implement digitally enabled, customer-centric products and services, and to ensure a successful digital transformation at Sub-K.

Early on, we realized that for our new digital platform SARTHI to be successful, Sub-K needed to pursue a fully integrated digital transformation model. It required an organizational redesign to reinforce a digital-first approach amongst the leadership and to align the vision with execution.

Sasidhar Thumuluri, Managing Director and CEO, Sub-K IMPACT Solutions Ltd.

Aligning around this model enabled Sub-K to launch the SARTHI fintech platform in August 2020. This platform currently offers their customers products such as MSME credit, digital micro-loans, gold loans, health insurance and micro-investments. The platform is integrated with multiple banks and third-party partners. Customers can access the marketplace on their own mobile devices or with the assistance from Sub-K’s staff and agents.

A center of excellence within FSPs can take a variety of forms. The center could have their own profit and loss (P&L) responsibility for products that they develop and take to market, or they could emerge as an internal service that is responsible for working with existing P&L owners to drive new and innovative solutions. As FSPs decide what model is right for them, it is important to consider which existing assets within the business will be leveraged in new digital initiatives. Usually, this model requires a significant shift in how departments such as IT, marketing, audit, and compliance, will operate, plan, and resource themselves to support the new venture, making clear agreements about how to share resources to achieve the organization’s priorities critical.

BancoSol is a financial institution serving more than one million low-income clients in Bolivia. As BancoSol embarked on their digital transformation journey, the bank opted to develop a digital center of excellence – an innovation hub – that would be responsible for leading the digital transformation of the bank. This group would enable BancoSol to better serve current customers and to explore what the future of the bank looks like. To encourage experimentation, the innovation hub was not configured to have P&L responsibility immediately. It was given the freedom to develop a digitally native identity and culture, and the responsibility to work closely with the other business lines to deliver new products and services. This structure enables the innovation hub to leverage the existing capabilities of the bank, including the tech stack,marketing, and operational staff.

The innovation hub also serves as an incubator for new skills for the bank. Currently the hub is focused on building capabilities in three areas: human-centered design, data analytics, and open innovation. As these mature, they will be embedded within the business units — moving the organization closer and closer to a fully integrated digital transformation model. As the digital maturity of the organization grows through this process, the innovation hub will continue to foster cutting edge capabilities.

In the long run, as the capabilities of the innovation hub grow, the vision is to transition to a standalone digital unit that has its own P&L responsibility, and that acts as a service provider for the bank, charging for its services. This bank-led innovation hub model has shown to be successful with DBS Asia X (DAX) and the BRAC Social Innovation Lab. Both these innovation hubs were developed by banks to create a space where ideas could be generated, developed, and implemented. The innovation hubs continue to bring internal innovation capability to the bank.

A standalone digital unit is a powerful idea for many innovators in the industry. The allure of being able to build, test, learn, and launch products without having to worry about the FSP’s existing business operations is strong. One notable example is ALAT, Nigeria’s first fully digital bank, which is a child of the country’s oldest bank, Wema Bank. ALAT was built from the ground up to provide a branchless customer experience. Today, ALAT has over 200,000 active clients, is Wema Bank’s primary banking platform, and is bringing significant transformation to the Nigerian banking industry. In order to set up a stand-alone unit, the strategy, focus, investment requirement, and management structure of the new unit need to be absolutely clear.

Under the Mastercard and Accion partnership, we have opted not to work with any institutions to create a stand-alone digital unit. Rather, we remain focused on the transformation of the microfinance operating model in order to help existing and new clients access credit faster, make payments digitally, save remotely, purchase insurance, and access other benefits.

Accion Microfinance Bank employees in Lagos, Nigeria help drive digital transformation.

Build (and rebuild) a culture of experimentation

Culture is a key determinant of a successful digital transformation. An institution can upgrade technologies, infrastructure, and processes, but without addressing the human element, lasting change will not happen. Many microfinance organizations struggle to build digital capabilities internally, as employees prize their deep relationships with customers, and fear that digital tools such as mobile apps or chatbots may diminish their value and have a negative impact on the customer experience. In some cases, effective digital transformation will require bringing in new talent that has different experiences and exposure outside of the organization.

Likewise, the norm in many financial service providers, is that management tends to be focused on the short term and in reaching quarterly targets, and key performance indicators (KPIs) are not designed to encourage risk and innovation for incumbents in such a heavily regulated industry. But digital transformation requires innovation — or reimagining how to respond quickly to market challenges and opportunities. And this requires KPIs, protocols, and a collective learning mindset that supports a culture of experimentation.

Institutions that adopt a culture of experimentation are invested in learning, rather than expecting a product to turn a profit from day one. DBS Bank for example, runs over 1,000 experiments every year —they strive to understand the needs of their customer, rapidly come up with ideas to solve their most pressing problems, and then take them back to the customer to test those ideas. While many of these experiments fail, it is the iterated version of those failures that leads to success. We find that many institutions will try something once, and it will fail, and the organization will never take the opportunity to learn from the failure and get past the initial iteration. Realizing the transformative power of experimentation is a commitment and over time, experiments yield thousands of small and not-so-small changes that can collectively result in huge benefits.

Don’t digitize your bank — digitize your staff, and they will digitize your bank.

Neal Cross, Chief Innovation Officer, DBS Bank

TO BUILD THIS CULTURE OF EXPERIMENTATION, THERE ARE SEVERAL STEPS FSPS SHOULD TAKE

Focus on alignment before getting started

Many FSPs have a perceived need to get new products out the door quickly to demonstrate progress on digital transformation initiatives. However, it can be counterproductive to shortchange the time and effort required to build alignment and a shared understanding of the roles and responsibilities expected of each team member in a new way of working together. Setting norms, from the Board down to each level of the organization, is the first step in defining the rules of engagement when creating and implementing digital transformation initiatives. In practice, key activities for digital transformation initiatives often fall on already over-burdened shoulders, which underscores how essential it is to ensure the incentives are right and that everyone has a shared understanding of the organizational priorities and their role in the strategy execution.

Sub-K’s CEO, Sasidhar Thumuluri, approached the challenge by first aligning with all teams on organizational goals and priorities. He held several strategy-setting workshops with relevant teams to identify gaps within the organizational design and process flows and to identify where concrete adjustments needed to be made. One opportunity area identified was a need to streamline hand-offs between the product and technology teams, which would be increasingly important to support the technological developments in the pipeline. Based on the workshop outcomes, the product and technology teams are working together to ensure hand-offs and configurations between the two teams are seamless.

Sasidhar also appointed subcommittees composed of senior-level staff to determine which activities best supported the organization’s priorities. Over time, this has made the organization much more amenable to running experiments. Their attitude has changed from “we can’t” to “we have challenges, let’s address them.” They have recently started evaluating use cases to implement conversational artificial intelligence and are running surveys to better understand the features and functionalities that their customers would find useful for their new customer-facing mobile application.

A culture of experimentation requires a test-and-learn approach — and a safe space to fail

With Accion MfB in Lagos, Nigeria, we began the digital transformation process with the awareness that the organization was in very early stages of thinking about digitization. Leadership was excited and motivated to digitize, and they assumed that the organization could just hire a few staff members with key digital capabilities to develop a new digital unit, and that would be enough to move the organization forward. However, we quickly learned that we did not have the buy-in or support from other departments that would be required for the digital team to be effective. The HR, IT, marketing, and risk teams simply hadn’t bought in to the mission of the digital unit, and the KPIs they were asked to meet remained aligned with business as usual rather than the bank’s new digital ambitions. This created a disincentive to take any risks aligned with the digital teams’ ambitions.

Even though the organization’s board and CEO were pushing digital transformation, this trickle-down approach was not sufficient to drive a culture where the shared services of the bank were able to support the needs of a team using a test-and-learn approach. For example, the operational teams had certain risk and compliance measures they had to adhere to and were skeptical of large-scale digital changes where the outcomes had not yet been proven.

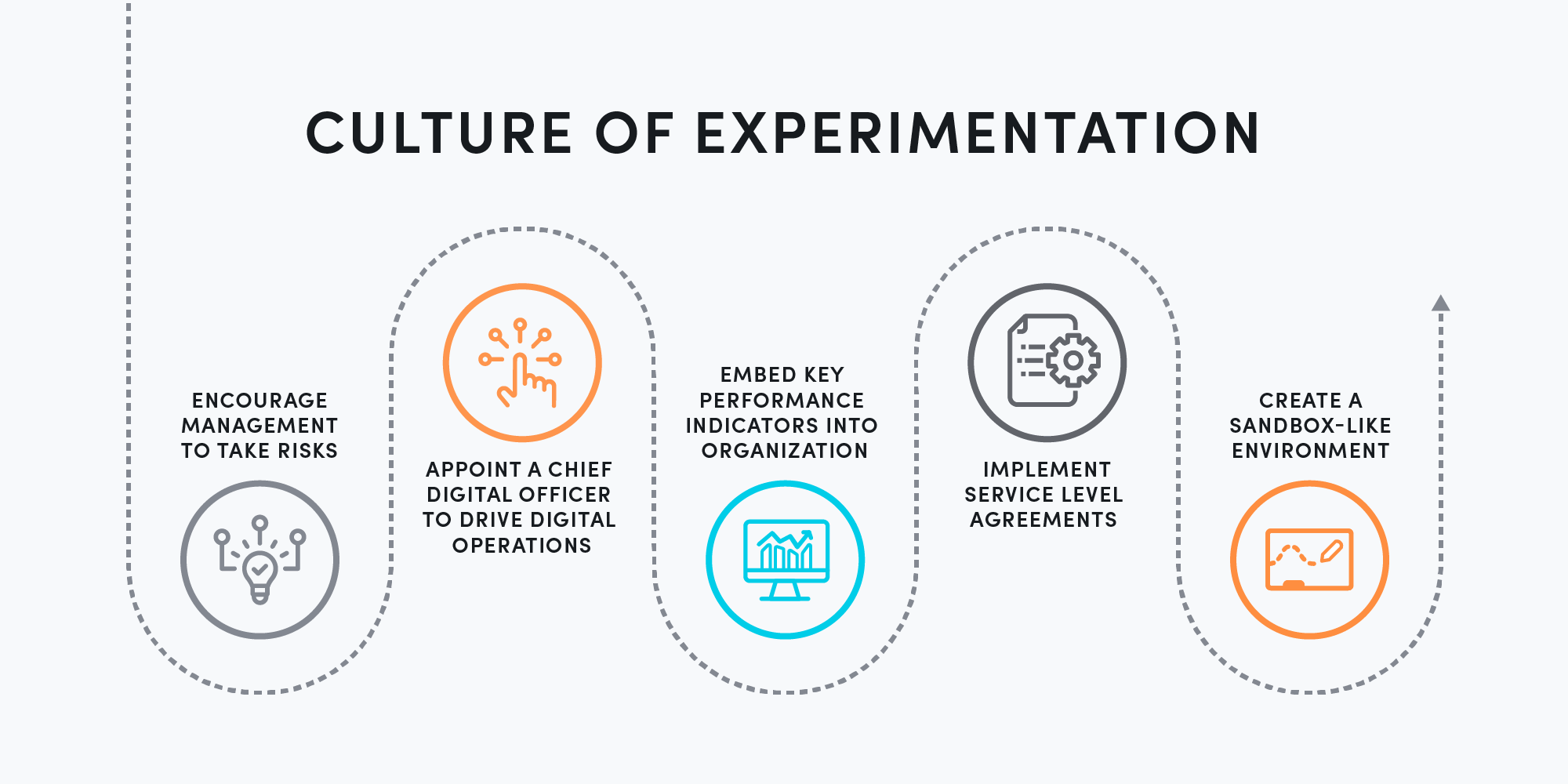

To address these challenges, the organization embedded the desired changes within the day-to-day operations of staff at every level by taking the following actions:

Encouraging management to take risks. One of the key challenges was to get the management to feel comfortable with learning by doing. They were worried about the impact of failed projects on the profitability numbers of the bank. The board approved an innovation budget and noted that any losses would not be counted against the bank’s profitability or performance-related pay. At the same time, the board held the management team accountable to demonstrate progress against their goals within an agreed timeframe.

Prioritizing a Chief Digital Officer (CDO) with the necessary people skills to drive digital adoption within the bank. The bank’s new CDO encouraged his team to take risks and learn from failure. It was more important to have someone who could set a vision and evangelize digital transformation than someone with deep technical and digital skills.

Developing digital KPIs and embedding them into the entire organization’s DNA. For example, the Human Resources team took on KPIs such as speed of recruitment of talent with digital skills, which were aligned around the needed competencies of recruits. The commercial team and branch managers were also given the mandate to contribute 15 to 20 percent of their time to digital support. This helped all teams understand their role in supporting initiatives sponsored by the digital unit.

Implementing several interdepartmental service level agreements (SLAs). For example, they ensured that audit and compliance will conduct timely assessments of digitally enabled products, marketing would respond to the needs of the new products being produced, risk team would support the needs of digital product innovation. This has been particularly important to ensure that departments develop budgets and plans that support experimentation requirements.

Creating a safe space to fail and encourage experimentation in a sandbox-like environment. They ringfenced potential risks by creating limits in terms of the maximum number of customers and the total amount to lend during the pilot to quantify the upfront costs needed for the experiment to achieve its learning objectives. The key was to provide a digital unit with autonomy and decision-making power and to frame the new digital loan as a low-risk experiment, rather than a fully fledged product launch. By doing this, the team was able to take a more flexible approach within the bank’s risk management framework for new product launches, to build up enough lending history for the digital loan pilot to validate the alternative scoring model.

Ultimately, digital transformation requires comfort with radical experimentation

A vital ingredient of any digital transformation strategy is experimentation. To be able to develop new offerings in a digital world, FSPs need the flexibility to experiment safely and effectively. This means that teams need the freedom to fail, all while ensuring that any inevitable failures occur in a secure environment. Leadership teams can create a safe environment for promoting innovation by mastering six skills: be approachable, compassionate, composed, manage conflict, direct others, and listen. Leadership teams that embody these characteristics open surprising doors that create differentiated offerings and innovative solutions to better serve financially excluded populations.

CÍVICO’s digital loan application provides MSMEs with just in time credit and flexible conditions so MSME’s can continue growing their businesses.

CÍVICO is a digital ecosystem that has geolocated hundreds of thousands of small merchants and corner stores across Latin America to make it easier for citizens to find what they need in their local environment. CÍVICO is not a traditional financial service provider, but many of the merchants in their network expressed a need for financial services to help them to grow their businesses. Seeing the opportunity to better serve their customers and grow their business, CÍVICO set out to develop an end-to-end digital loan product for underserved businesses to help communities thrive. Because CÍVICO did not have the financial services infrastructure in place, they were initially solely considering partnering with external vendors to develop a digital lending platform. However, due to uncertainty caused by the COVID-19 pandemic, many of the partnerships they had been considering failed to materialize due to perceived elevated risks in lending.

Rather than continue to wait for the perfect partner to come along, especially when they knew that their users needed capital immediately to sustain their businesses, CÍVICO made the bold decision to start lending directly. They launched a low-fidelity product, lending very small amounts and limiting their total investment to just $15,000 USD so that they could conduct tests and learn quickly. This low-fidelity product has enabled CÍVICO to make several adjustments to their processes and product. For example, the team found that they needed to develop a filtering process to determine the specific needs of the MSMEs in their network. They deployed a survey that evolved into a merchant assessment tool. When they cross-referenced these profiles with CÍVICO’s existing data, it helped them to better understand the entrepreneur’s behaviors, their biggest pain points in recovering from the pandemic, and the state of their financial health. With this data, CÍVICO was more easily able to target the merchants most in need of credit and recommend specific educational modules, available on the CÍVICO platform, that would be most useful for the business. This is also helping them identify how to better use alternative data for credit scoring. After six months of running the pilot, they have been able to reach 1000 customers, and they are constantly incorporating learnings into their processes. CÍVICO has also identified several partners with which to scale the digital loan offering and is working toward building a multi-partner flexible product. By launching the pilot early with a small group of customers, they were able to finetune which customers to target and reduce risks for themselves and their partner lending institutions.

Employees like Sharda embrace digitalization at Sub-K in India.

Have a clear data strategy

Any digital customer experience requires quality and curated data that is readily consumable as close to real-time as possible.

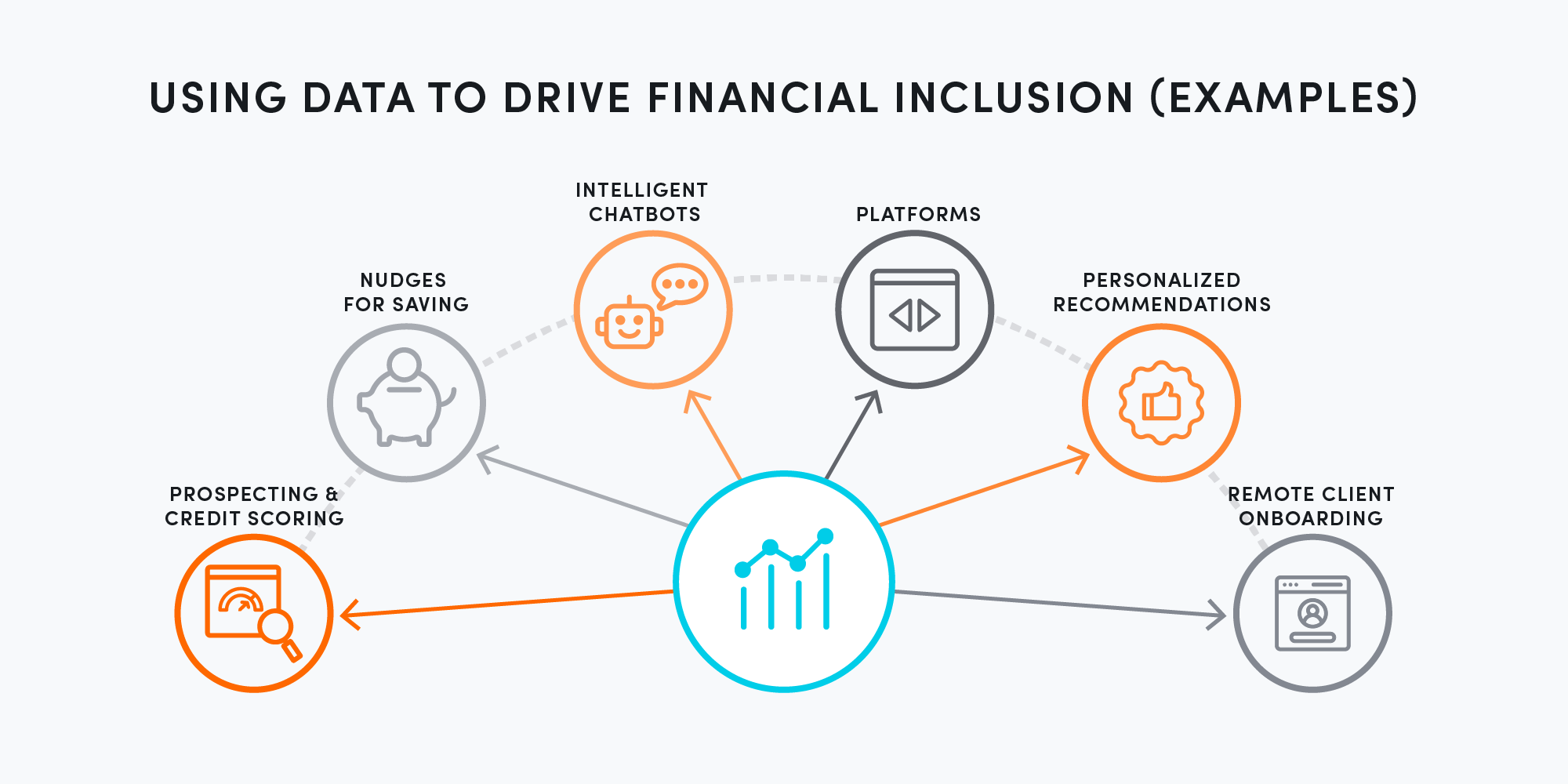

Data capabilities play an essential role in an organization’s digital transformation. Data can inform optimization strategies that increase efficiency and revenue. Data itself can also be monetized creating entirely new business models where data assets become products. Especially today, when FSPs must make unprecedented and rapid decisions, adjust business strategies, segment customers to understand portfolio risks, rethink credit models, and enable remote engagement with customers and staff, data capabilities go hand-in-hand with digital.

For the unbanked and underbanked and the financial providers that serve them, the explosion of available data, data-analytics services, and a growing digital ecosystem creates unprecedented potential. The possibilities to unlock inclusion, greater financial health, and opportunity for the underserved are extraordinary, from prospecting and credit scoring for thin-file consumers to well-timed nudges for saving, to intelligent chatbots, to personalized recommendations, to remote client onboarding, to access to online platforms. Any digital customer experience requires quality and curated data that is readily consumable as close to real-time as possible.

Despite the proliferation of data, the challenges of obtaining and converting raw information into actionable insights are immense. Many organizations become overwhelmed with the possible use cases for data and lose alignment and focus when it comes to creating a data strategy. Some institutions end up creating a parallel siloed data strategy rather than an integrated strategy which acts as a key enabler to their core strategic initiatives. However, microfinance organizations can take several key steps to harness the power of data in their digital transformation. These steps amount to a plan for how to align and prioritize data and analytics activities with key digital transformation priorities, goals, and objectives.

Derive value first from the data you have

In the early stages of developing a digital loan product, Accion MfB explored potential data-sharing partnerships with several entities, which would enable them to build a robust scoring model that would leverage alternative data. However, it was challenging to assess the value-add from potential third-party data providers and agree on how best to structure a commercial partnership. This challenge prompted the bank to take a long hard look at their own data. The organization has an arsenal of over 10 years of lending data that has been under-utilized, and the team realized that they could do a lot more with their own data if they got creative and looked at it in a different way. For example, they were able to use what they already know about customers’ willingness to pay and capacity to pay to design the pilot digital loan product. They leveraged historical data collected from existing bank customers and used this to create a benchmark profile against which to compare incoming data from new customers. As the use of their own internal data involved fewer operational and commercial complications, it helped the bank launch a viable pilot quickly even as it continues to explore other collaborations.

Be practical with how to get from insights to action

Similarly, BancoSol in Bolivia has been in operation for over 30 years and today serves 1 million clients, making it one of the nation’s largest banks. Mindful that they have a lot of untapped data under their noses, BancoSol wanted to leverage this data to uncover insights that could help to address four key challenges for the bank: drive digital adoption and improve usage, increase cross-product usage, increase savings balances, and maintain customer relationships. Accion and Mastercard supported BancoSol by convening a 36-hour “datathon” during which 40 Mastercard volunteer data scientists collaborated to tackle these key challenges.

Three key recommendations came from this exercise:

Start by understanding your typical digital customer. Analyzing customer demographic data and banking patterns can help identify and nudge those customers who are most likely to go digital. In BancoSol’s case, the datathon revealed that its typical digital app customer was more likely to be female and more likely to be younger compared to the average BancoSol client. By understanding the typical digital customer, BancoSol can prioritize those who may be most-inclined toward digital adoption.

Equip loan officers with insights to match customers with products that meet their needs. The datathon analysis revealed that app users made nearly twice as many deposits as other users — linking digital adoption with increased use. As research has shown, greater use of financial products, whether that’s insurance, savings, or credit, makes small businesses more resilient to shocks like COVID-19 and also ensures the bank’s own sustainability. Equipped with these kinds of insights, loan officers can better communicate key benefits of going digital and identify when unexpected hurdles might be steering potential users away, like privacy or information security concerns or bad online experiences elsewhere. With insights from users, BancoSol was able to develop clear messaging for loan officers about privacy and security, and continually test and streamline the app experience for customers so it matched expectations.

Retain customers by being proactive, not reactive. The datathon offered insights on customer retention. When a customer stopped saving or communicating with the bank, for example, his or her risk for a loan default rose. Based on those factors, the data analysts created a risk propensity score, which the bank can use to intervene before a customer begins to disengage. The datathon also revealed that a digital connection can improve retention in the absence of an in-person connection, critical in an era of social distancing. Customers who use digital channels maintain consistent relationships with the bank and have more consistent differentiators between high and low retention risk.

Based on the experience of the datathon and seeing the value that could come from the data already in their arsenal, BancoSol has hired a full-time data analyst to join the team and plans to add on additional data experts over time. They know that having dedicated resources skilled in data analytics embedded within the product innovation team will help jumpstart a virtuous cycle of data-driven design.

After conducting the datathon [a hackathon style event supported by Mastercard data scientists], we have been able to see other perspectives of the data we have stored that we had not discovered before. The data was there, now we see it in a different way, with more value.

Carlos Otalora Martinez, National Manager of Information Technology, BancoSol

Prioritize data management and governance

To derive value from existing data, microfinance institutions need to invest in structuring their data appropriately and be deliberate in the governance and management of their datasets to ensure their usefulness and adherence to data responsibility principles. Data governance establishes policies and procedures around data and must involve key business stakeholders. Data management comprises the set of activities and logistics involved to enact those policies and procedures with regards to how data is compiled and used for decision-making. FSPs should be proactive in adhering to global best-in-class customer data protection and privacy regulations, even if they are not (yet) required in their country.

Many institutions know they possess valuable data, but it is stored in various places and in multiple formats. They often ignore complicated archives and only manage the limited data that they are required to — or that is easily accessible. Many are preoccupied by fulfilling regulatory reporting requirements or consumed by responding to urgent ad hoc data requests, leaving little time and bandwidth to step back and organize their data. They acknowledge the importance of, but defer investing in, proper data management solutions to a later date, yet as data accumulates, this becomes harder. Annapurna Finance Limited wanted to address this challenge and has recently invested heavily in data management solutions that will improve data reporting, data migration, and data storage for new digital platforms and products from day one, such as the loan origination system, which will expedite credit scoring and origination of new digital lending and other products.

Nearly every financial institution struggles with maintaining accurate customer contact information, a simple yet critical example of data management. For microfinance institutions with high-touch models, having a current phone number on file can seem low priority, since the loan officer regularly visits customers in person. However, when lockdowns were first implemented due to the COVID-19 pandemic, the ability for loan officers to communicate directly with their group lending customers became almost impossible without up-to-date contact information. Annapurna needed to communicate critical loan information, including payment dates, updates on moratoriums, and even introduce new loan offers via SMS, as many of their clients only have access to feature phones.

Many institutions know they possess valuable data, but it is stored in various places and in multiple formats.

However, they found that their database of phone numbers was outdated, with many numbers no longer working or belonging to a new individual. Annapurna introduced a standard process to ensure that at every customer touch point — whether during a field visit from a loan officer or a customer visit to a branch — bank staff would confirm the customer’s phone number to ensure a high-quality database. In parallel, they implemented a new communication system, which required them to integrate their SMS messaging system with their loan origination system. These two initiatives helped to standardize communications with customers, create greater engagement, and ensure a more transparent flow of information

BancoSol employee Celia Copa Choque assists small business clients in Bolivia.

Future-proof your transformation with the right technology platform

While an institution’s technology infrastructure can be a springboard to leap forward, it can also be an obstacle. Today’s social distancing measures have made technology maturity even more crucial, as technology determines whether the institution can quickly deliver the critical digital functionality its staff and customers need. Underlying all of this is a need to build more flexible core IT and data management systems, which have traditionally been a weakness for MFIs. The ability to evolve and adapt business models, dependent on agile and adaptable IT systems, is increasingly a defining factor in the digital age.

A key to digital transformation, and what makes it so difficult, is balancing both the necessary planning required to transform the organization and the agility needed to innovate quickly. In a Harvard Business Review article titled “Make your strategy more agile,” Tim Leberecht highlights the union of vision and improvisation:

“Vision incorporates the long-term, if not permanent, purpose and principles of an organization, which serves as the north star for all its actions. Improvisation suggests a fundamental openness and flexibility at the tactical level — the willingness to explore, experiment, and iterate.”

Perhaps nowhere do the conflicts inherent in these two opposing concepts come more starkly into contrast than in the technology stack and IT functions of an organization undertaking digital transformation. The fact is, technology decisions made today will impact what’s possible tomorrow, so organizations need to design for the future while understanding the constraints they face today due to legacy systems. Following these key design principles can help your organization balance conflicting priorities and opposing forces to build its future state architecture.

We started our digital journey in 2017…the first thing we did was to look at our IT architecture and IT backbone, to see whether they were sufficient to carry [our] digital aspirations…

Taiwo Joda, CEO, AMfB Nigeria

Balance vision and improvisation

Balancing infrastructure planning (or vision) with agility (improvisation) often requires a phased approach, with work around solutions enabling products to get to market quickly, while parallel tracking more long-term strategic investments in future-proofing your technology infrastructure. BancoSol was able to effectively take such a parallel approach. At the onset of their digital transformation journey, senior leadership articulated a vision and an implementation plan for the technology stack and analytics platform capabilities which would be required to execute the bank’s digital strategy for the next five years and beyond. The organization committed to ambitious digital adoption targets to set a north star toward which the team should set its sights. Yet, the team also recognized that it was equally important to start somewhere, to commit to improvising an agile approach to innovation rather than wait for the entire technology infrastructure to be deployed before beginning development of their first digital minimum viable product (MVP). Instead, the MVP was designed to function within the existing technology systems with the minimum modifications necessary in terms of API connections, etc., while planning to rollout additional functionality in line with the broader technology roadmap.

Balancing vision and improvisation also requires careful consideration of what to build in house versus what to outsource. As technology evolves, that question becomes increasingly complex. It may be easier to outsource key functions, but institutions need to be careful about protecting their core value-add to the market and not concentrating risk by relying too heavily on one vendor. Sub-K’s digital marketplace, SARTHI, was initially planned for in-house development, as they felt their IT team had the needed capabilities. However, after some deliberation, they realized that it would not be worth the time or effort to develop all of the capabilities needed internally, especially solutions that have already been commoditized in India. The organization decided to partner with several vendors to get access to their existing solutions, with necessary customizations. Sub-K knew that their core value-add was their unique methodology and agility to add new products and partners to the platform, so they needed to work with a technology partner to build a platform that enabled this flexibility.

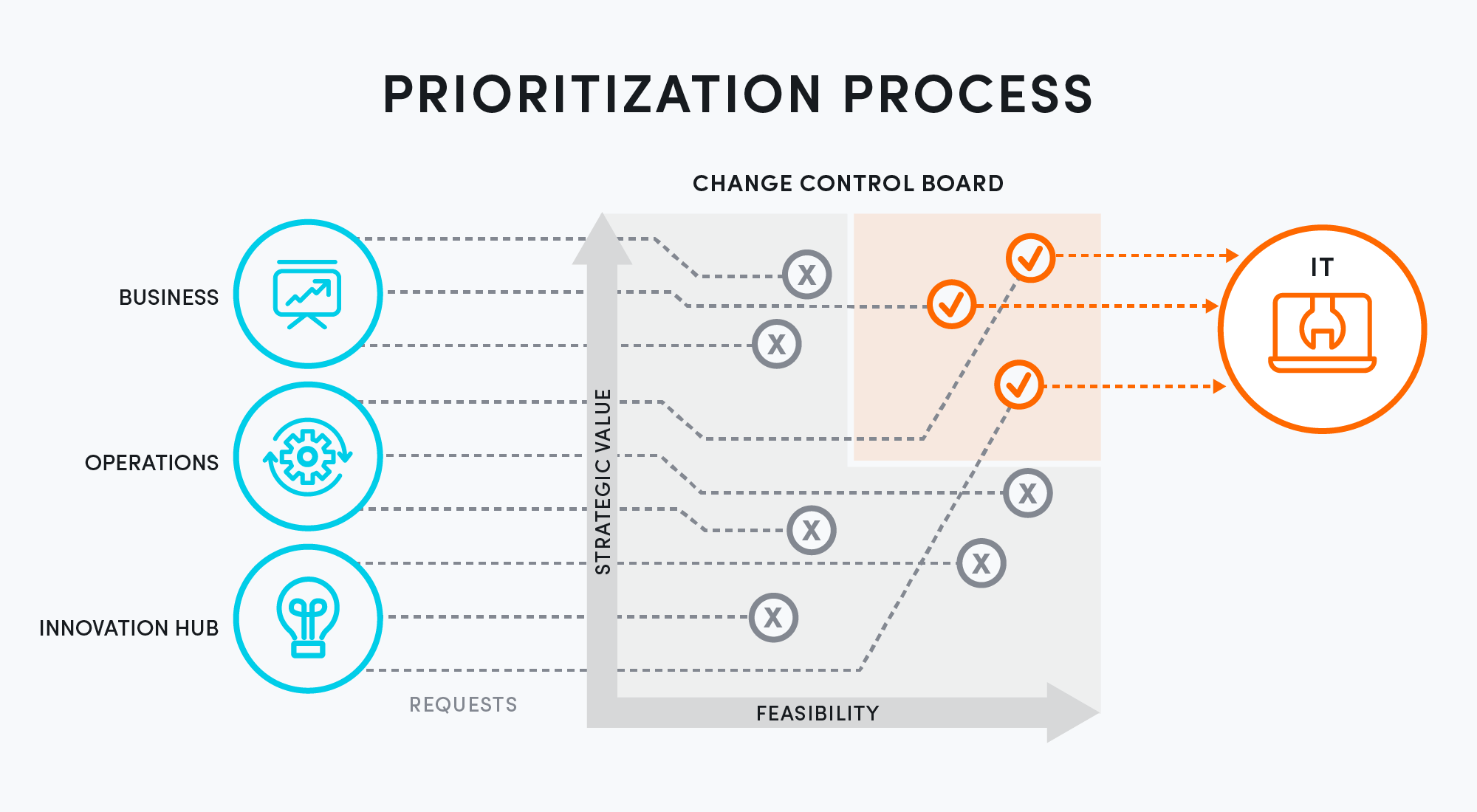

Finally, a strong and coherent technology team is critical to delivering on the vision. The challenge confronting this team during a digital transformation is: how do we balance new digital initiatives with the tasks of business as usual? And how should we determine what to focus on? Digital transformation requires that IT departments are clear on the organization’s transformation priorities and can effectively prioritize incoming projects. Sub-K, for example, has established a “change control board” tasked with assessing the business value of each request to prioritize the change requests. This board governs the process for required sign-offs and cross-checks with all affected product owners when a change is requested to the IT work stack. This helps IT manage delivery by prioritizing feasibility and strategic importance of various initiatives and continually reevaluating the current backlog.

Likewise, our partner Bina Artha Ventura in Indonesia had three standalone initiatives they wanted to pursue at the outset of their digital transformation journey: ecommerce, digital identity, and digital lending. In an effort to combine all three into a logical technical architecture, they made the strategic decision to prioritize development of an overarching customer engagement platform, which would support and ultimately be able to deliver their other key initiatives.

Think strategically about APIs to modernize legacy systems

The movement toward open-banking, or the system of allowing access and control of consumer banking and financial accounts through third-party applications, has generated a need for FSPs to be able to consume and produce data for third parties to reap the benefits that partnerships can provide. APIs play an important role in ensuring that a company can access, interact, and engage with a third party’s data and functions. They can also be an effective tool to modernize legacy systems in a way that is low-cost, efficient, and does not require a complete (and expensive) upheaval of the existing core system.

At Accion Microfinance Bank, for example, the team needed to find the right partner to support their ambitions to create a digital loan product. After finding the right partner, the organization quickly realized that to deliver the digital loan capability, it would need to build APIs to connect with the partner’s systems. To evaluate the feasibility of this, the team conducted an API inventory — or an evaluation of how various systems should connect and where vulnerabilities may lie.

Though this process, they examined:

the various integration points required for the organization’s systems to be able to communicate with various partners or vendors to meet the requirements of the digital lending product,

whether these integration points already existed,

whether they had the capabilities needed to manage the data, and

handoffs that may be required between the technology and operations teams.

This inventory helped them to understand the steps they would need to take to develop the capabilities required to manage the data exchanged through the new APIs.

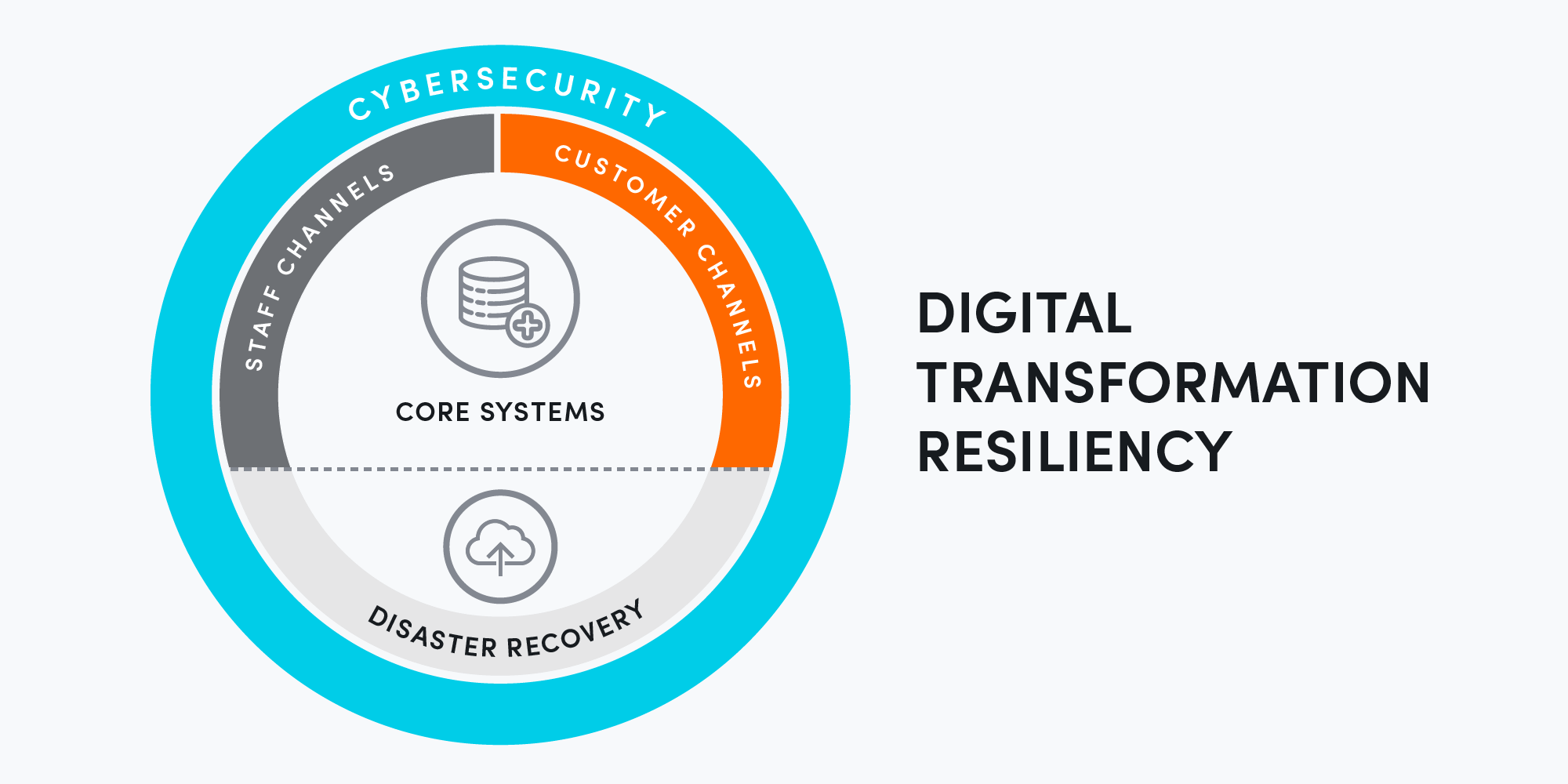

As you go digital, ensure you are resilient

Digital transformation requires great reliance on the external and internal technological environment. The external environment includes the availability of mobile connectivity in the region, the ability to connect with others over the internet, and the technological readiness of potential partners. The internal environment includes the systems such as the core banking system, data warehouses, document management systems, and office automation systems. As an FSP begins to digitize, through greater process automation or through new business models, the more vulnerable their systems may be to system failures or cyber-attacks, and the more resilient its internal environment needs to be to avoid these challenges.

Ezeh, a client of Accion Microfinance Bank in Lagos, Nigeria

To build resiliency, it is important to have well thought out and structured disaster recovery plans with remote disaster recovery sites set up with the appropriate failover and switch back parameters in place. These can include both on-premises (in physical server rooms) and on-cloud architecture. Cloud technologies, particularly, can improve technology resilience through greater regional autonomy (not dependent on other regions to run), data backups, and automated insights for decision-making.

However, regulators often perceive cloud infrastructure for financial services to be risky in terms of its suitability to safeguard customer’s personal and financial information. Financial regulators have a more comfortable view of carefully designed cloud-based architecture held within the country’s borders. Given the low cost of using cloud architecture and the benefits they offer, institutions can and should explore their use.

Finally, as FSPs digitize, cybersecurity is critical to ensure that the organization can reach its digital vision and the technology stack continues to be future proof. Cyber threats and attacks have increased since the start of the pandemic, particularly ransomware and COVID-themed phishing attacks, and organizations in the midst of digital transformation are very vulnerable. Effective mitigation against cyber risks requires developing layers of governance, accountability, policies, and procedures, all while creating and adhering to new norms of data protection and guidelines.

We worked with Accion AMfB, Sub-K, BancoSol, and Annapurna to recommend the necessary systems for greater resilience. This included suggestions for finetuning their disaster recovery plans, assessing cyber-risk solutions, regular testing, and the cultural changes needed for staff and partners to proactively address cyber risks and ensure business resilience and continuity planning.

BancoSol client Felix Marcelo Quisbert in La Paz, Bolivia.

Form partnerships to achieve scale

Partnerships are key to success in digital transformation. They can enable new ways to leverage data, evaluate risk, reach new customers, develop new products and services, and strengthen customer touch points. FSPs need to carefully consider when, how, and with whom to partner. The right partners will help accelerate your transformation agenda, bringing in agility and expertise that are beyond the core competencies of the FSP. As FSPs grow and evolve digitally, they are better able to integrate with formal players in the financial services ecosystem, such as payment providers and credit bureaus.

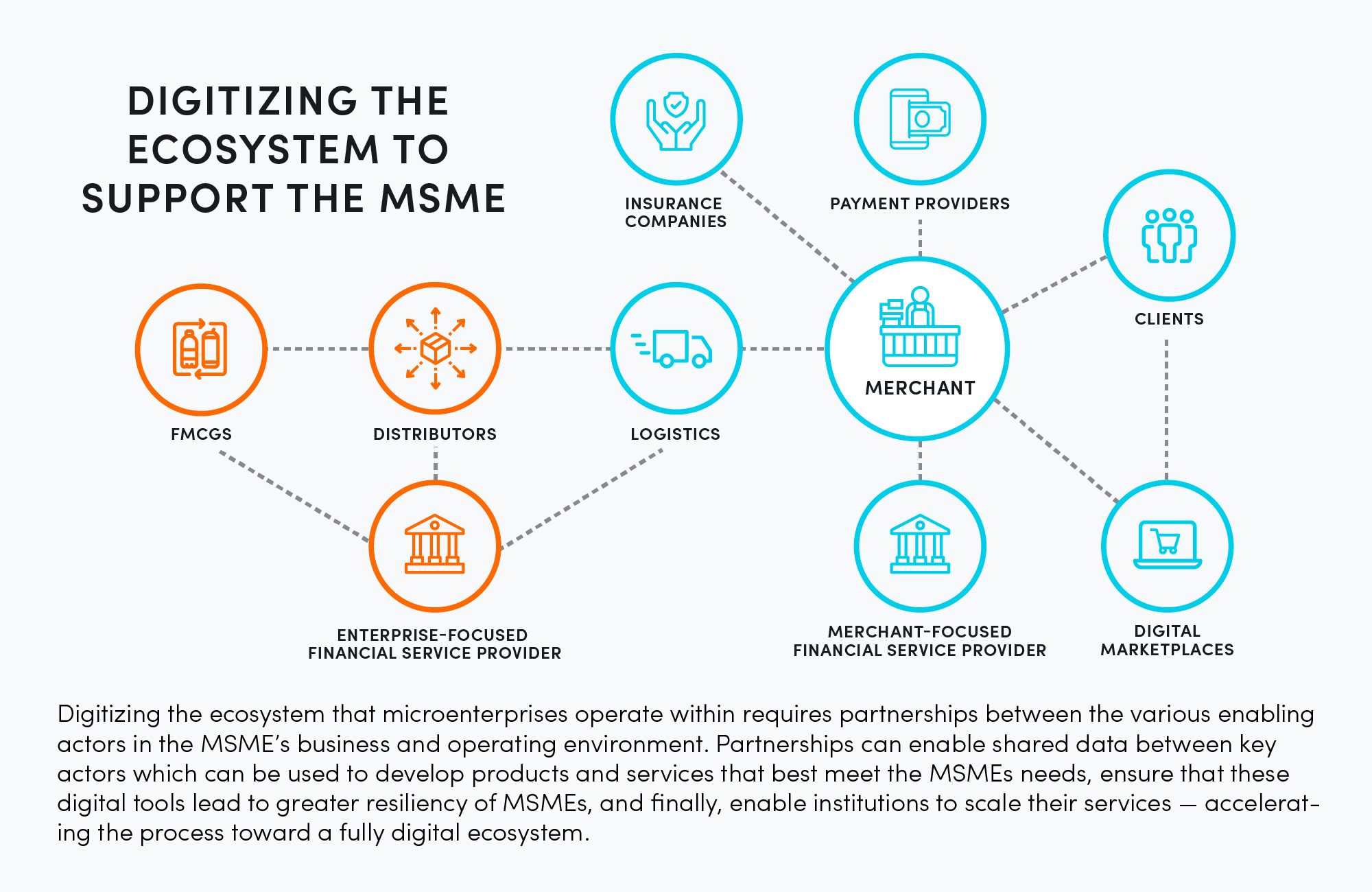

Partnerships are critical to expanding the reach and uptake of financial products among underserved people by supporting the development of a 360-degree digital financial ecosystem. We know that providing customers with digital financial products is only useful in so far that the financial ecosystem in which the customer operates has digital capabilities across the value chain, including merchants being able to accept digital payments, customers willing to pay digitally, and suppliers to small merchants accepting digital payments for inventory. Lacking any of these crucial elements can generate a bottleneck within digital financial transactions that will slow the adoption of digital financial services. To address this, many partnerships are emerging between FSPs and other enabling actors to drive this ecosystem. For example, FSP partnerships with mobile network operators (MNOs) are focused on enhancing mobile payments and increasing the usability of payment-related technologies — and have transformed how people complete financial transactions in many markets. As the density of digital services available within an ecosystem grows, so too will the digital comfort of end-customers.

Some FSPs, however, tend to view partnerships through the narrow lens of a vendor relationship, rather than seeking to create something that is greater than the sum of its parts. The sticking point for many partnerships is a question of who owns the customer relationship and their data and a lack of a clear business case that aligns the goals of all parties. However, there are many ways to address these issues and build partnerships that work.

We are creating a digital ecosystem that reduces the use of cash, promotes responsible financial inclusion, improves living conditions, and facilities access to financial products and services to all segments of the Ecuadorian population — especially the most vulnerable.

Verónica Gavilanes, General Manager, Microfinance, Banco Pichincha in Ecuador

Establish win-win partnerships

Our partners, including the team at BancoSol, are developing innovative products to help small businesses to succeed.

BancoSol, as one of the leading financial institutions in Bolivia, has a first-class IT team. They were able to develop their latest customer mobile banking app completely in house, and high uptake of the product established them as a pioneer in the market. However, when they planned to upgrade to a 3.0 version, they wanted to find a partner that could help them get to market within 100 days. Partnering with fintech startup Flourish allowed them to layer the gamification functionality enabled by Flourish’s platform on top of the bank’s digital assets, as a tactic to drive engagement — in this case, increased savings deposits — within the revamped customer app. The partnership was successful because it went beyond a mere vendor-bank relationship, with both entities collaborating on how to reach shared goals. Flourish was able to bring its knowledge of behavioral science together with BancoSol’s strong understanding of their customer to develop a captivating customer engagement strategy. The partnership was win-win for both entities: Flourish was able to enter the Bolivian market and BancoSol was able to get to market faster.

Partnerships can serve as a mutually beneficial go-to-market accelerator. For example, a good partnership can benefit both an FSP looking to scale their digital offerings and an ecommerce platform looking to grow their customer base. That’s why Accion MfB teamed up with African ecommerce giant Jumia to help onboard their MSME customers onto the Jumia platform to boost sales through ecommerce and increase MSMEs’ comfort and trust in using digitally enabled tools to run their businesses. Jumia customers benefit through access to Accion MfB’s credit offering. Through this partnership, Jumia will be able to grow its customer base, and Accion MfB will be able to leverage ecommerce sales data to underwrite digital working capital loans.

Expand your definition of partner

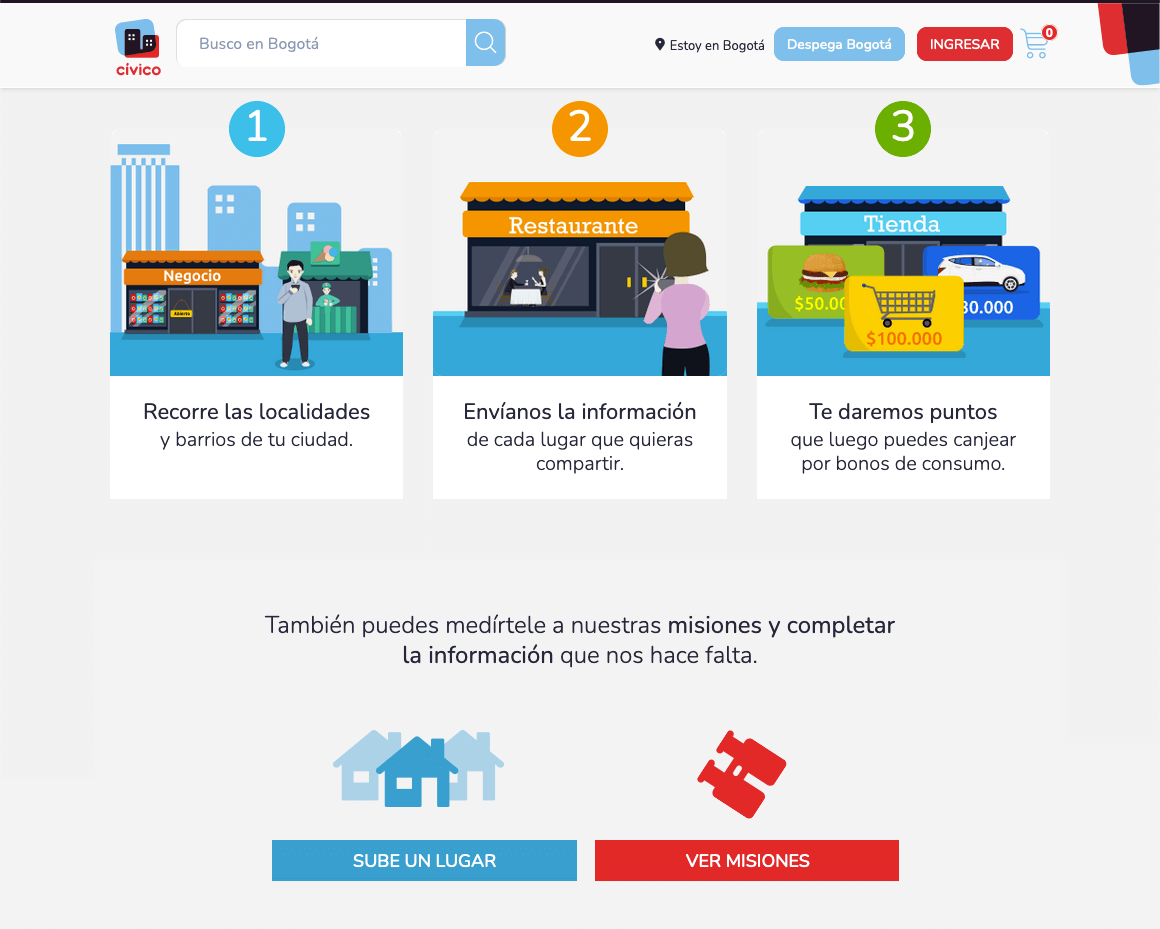

When most people think of partnerships, the first thought that comes to mind is an alliance between two independent entities. However, CÍVICO’s founders are not ones to let traditional concepts define the realm of what’s possible, having invented a crowdsourcing model for citizens to map their own cities by posting missions and offering points and rewards to those who complete tasks, such as confirming the products or services offered at a specific location. In this way, they were able to build out the most comprehensive picture of local small businesses and other civic services available in cities like Bogotá, Colombia, and gain a better understanding of what financial services those small businesses might need.

The screen shot above is from CÍVICO’s website and describes how everyday citizens can collaborate with CÍVICO to map small businesses in their city, by taking the following steps: Step 1: “Tour the neighborhoods in your city,” Step 2: “Send us information from each place you are able to share,” Step 3: “We will provide you with points that you can later exchange for customer vouchers.” On this page, citizens can upload information about a business or look for other missions to complete.

But for CÍVICO’s new digital lending product to be viable, the company needed to find a cost-effective way to mitigate risk by verifying the business location of their online applicants. Rather than deploying CÍVICO staff to visit every potential customer — as a loan officer would do in the traditional microfinance model, and which would be expensive and time consuming for the start-up — CÍVICO turned again to their crowd-sourcing platform. They created new missions where individual citizens were asked to verify the location of the business by taking a picture of it and collect information related to perceived sales activity.

In the few cases where the business could not be verified in this way, CÍVICO would then deploy other more resource-intensive channels to verify the customer, either by phone or by conducting the visit themselves. This crowdsourcing-by-default design enabled an OPEX light business model by leaning on the existing relationships the company had created through their gamified crowdsourcing platform.

Conclusion and next steps

The global pandemic has taken an especially devastating toll on low-income people and small businesses. These vulnerable populations need access to financial tools that can help them rebuild their livelihoods and gain access to the increasingly digital economy, and they need financial services that are convenient, easy to use, and affordable. Digitizing swiftly and effectively is vital for FSPs to meet their customer’s evolving needs responsibly and at scale.

Much remains to be done, both by our partners and the industry at large.

Our global partnership with Mastercard has laid a solid foundation toward our goal of helping millions of people and small businesses fully participate in and benefit from the digital economy. While digital transformation is a continual and never-ending process, our partners have already accomplished so much. Beyond the digital products and services our partners are launching, what we hope sticks is the transformation process itself: the willingness and ability of everyone — through the culture of innovation and learning they create — to continue on the journey so that they can be responsive to the needs of their customers and meet challenges and opportunities as they arise.

The digital transformation of FSPs can also encourage more people to embrace the use of digital tools and spur the digital transformation of MSMEs. Individuals that are able and comfortable transacting digitally can connect more easily online and participate more fully in an inclusive digital economy. To date, 1.3 million microbusinesses are actively using digital products on a monthly basis as a result of this program. One notable example is 26-year-old Rosina Das, who with the help of Annapurna’s digital emergency loan, was able to reopen her small grocery shop in her village of Odisha, India. Similarly, millions of other MSMEs around the world can benefit from digital financial services to build resilience and seize opportunities.

Yet much remains to be done, both by our partners and the industry at large. Donors should play the important role of catalyzing the digital transformation of microbusinesses through strategic investments in microfinance organizations. Governments and regulators can take steps to reduce the demand for cash through carefully crafted regulations that incentivize digital transactions. Finally, development finance institutions and multilateral institutions should further embrace digital transformation through technical support that is backed with investment funding.

We hope the learnings, insights, and strategies we share here inspire others to collectively contribute to the building of an inclusive digital economy. We are also hopeful that these examples of how our partners are addressing key challenges, while celebrating milestones achieved along the way, can inform the approaches of other institutions as they evolve and grow in our increasingly digital world.